The Japanese government's $20 trillion carry trade finally exploded

The carry trade has broken down, and in any case, the game is over for Japan.

JinseFinance

JinseFinance

Source: DODO Research

The footsteps of spring always step on the muddy path, and 2023 is a year where challenges and opportunities coexist. We have witnessed the release of Uniswap V4 and UniswapX, the underlying code of Curve was attacked, and the emergence of DEX newcomers such as Maverick.

In this volatile market environment, DEXs have not only experienced technical challenges, but also faced increasing competitive pressure. Despite this, many DEXs continue to make breakthroughs in innovation, launching safer and more efficient trading mechanisms, attracting a large number of new users.

In the past year, the DEX Weekly Brief column has closely monitored and reported the latest trends and key data in the decentralized exchange (DEX) market. TheDEX Annual Report condenses the DODO Research team’s detailed observation and analysis of the market throughout the year, and provides an in-depth discussion of the significant trends and important findings in the DEX field in 2023 for reference.

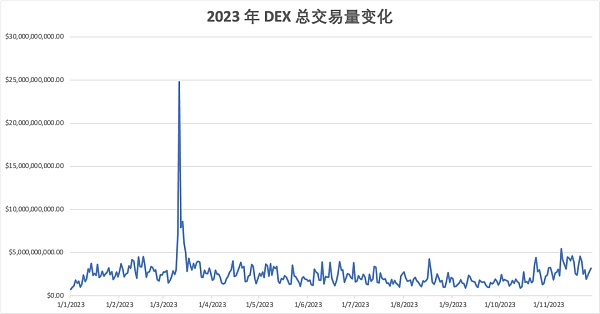

“The total DEX trading volume in 2023 at the beginning and end of the year It is at a high level, and fluctuates at a low level during the rest of the time, showing a certain positive correlation with the trend of the market."

Since October, affected by the expected adoption of ETFs, the total trading volume of DEX has shown a relatively high Significant climb and growth. Market volume is showing clear signs of recovery and is expected to maintain growth in 2024.

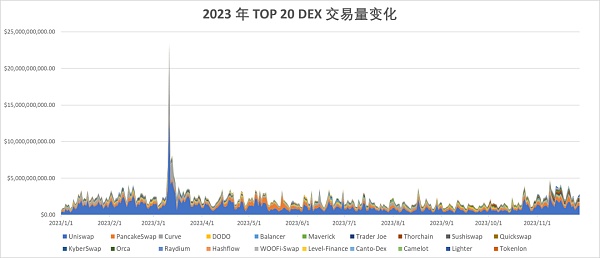

From a single trend perspective, Uniswap The performance was stable throughout the year, occupying a major share of the market. Other DEXs have performed well in event-driven events. For example, Pancakeswap launched V3 on the BNB chain and Ethereum chain in April, which improved fund utilization and reconstructed the fee results, resulting in significant short-term growth in the platform's monthly trading volume and market share. .

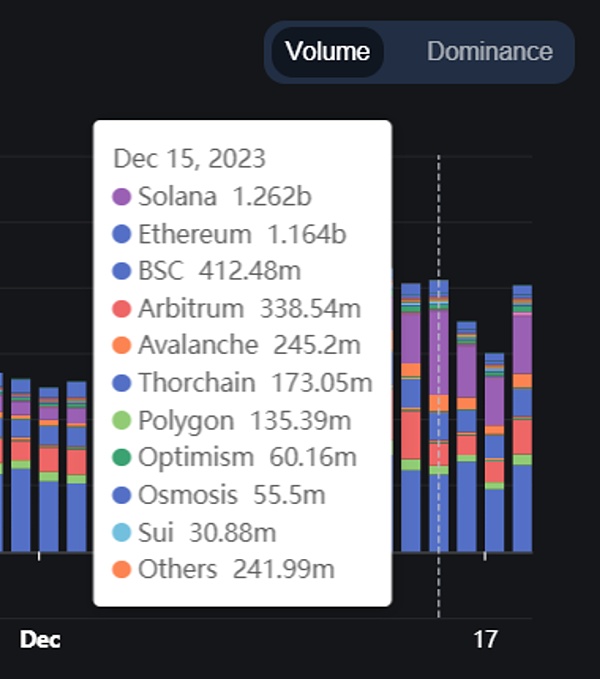

Starting from the end of October , the market style has gradually changed: from Uniswap's "one big one" to the pattern of "one super, many strong". Affected by the active ecology of major public chains such as SOL and AVAX, the DEXs at the head of these chains have contributed a lot of transaction volume, even surpassing the traditional mainstream DEXs on the Ethereum chain (see Weekly Brief for details). According to data from Defillama, on December 15, the DEX trading volume on the Solana chain exceeded US$1.2 billion, surpassing the Ethereum chain that dominated the list for the first time.

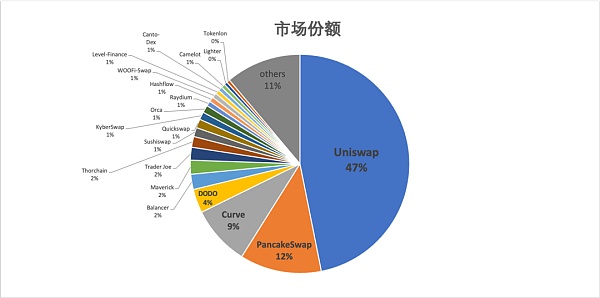

TOP 20 DEX market share ranking As shown in the pie chart, these DEXs account for approximately 89% of the total DEX market share. Uniswap has maintained its dominant position as the top player this year with 47%, and the overall DEX maintains the "echelon stratification" pattern.

Uniswap is located in the first echelon. It has rich products, wide reputation, and its market share accounts for half of the market. The second tier is Pancake, Curve, and DODO. These three DEXs account for 25% of the market share. The third tier includes Balancer, Maverick, TraderJoe, Thorchain, etc., and the remaining DEXs are divided into the fourth tier.

The second tier are all established exchanges with long operation times and mature and stable products. There are many newcomers in the third tier. Maverick has often reached the TOP5 in market share since its launch at the beginning of the year with its automatic balancing liquidity mechanism; Thorchain's unique casting mechanism has also gained new life with the support of the market recovery.

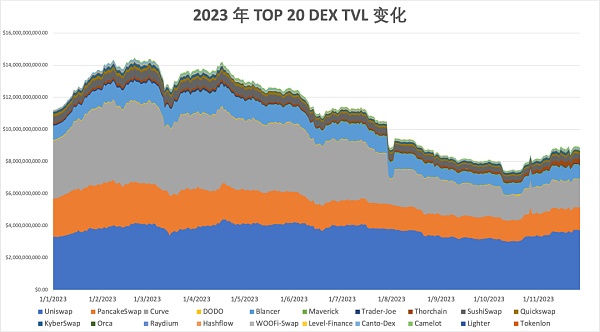

Represented by the TOP 20 TVL , the overall TVL of DEX has not experienced a cliff-like decline similar to that in 2022. After showing a certain recovery at the beginning of the year, the decline of TVL has gradually slowed down, and an inflection point has appeared in October, with the possibility of reversal. The overall TVL scale is around $9B.

The vast majority of TVL is locked in the leading exchanges: Curve, Pancaksswap and Uniswap. Uniswap’s TVL performance is stable, while Curve’s TVL has shrunk significantly after the hacking incident, and is not much different from Pancakeswap’s TVL. Thorchain’s TVL performs better.

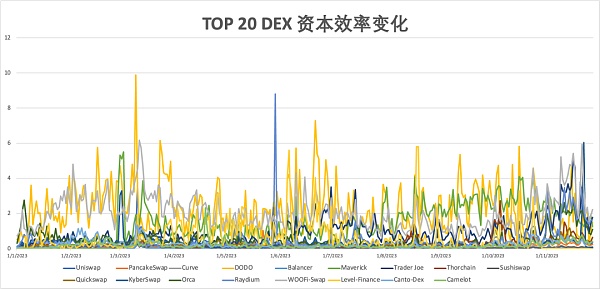

“Looking at the overall capital efficiency of DEX, the overall capital efficiency performance of the DEX track has recovered. Capital efficiency has gradually transitioned from local activity to global activity. Capital efficiency has improved and the market has tended to pick up. ”

From the perspective of the capital efficiency of a single DEX, the yellow line DODO led the market throughout the year, and only the gray line Curve remained active at the beginning of the year. The second half of the year started in August, and the green line Maverick suddenly emerged and performed well during the market shock.

“On the whole, major DEXs are actively expanding into EVM-compatible public chains and L2.”

This not only helps to diversify the product user base , also reflects that DEX is leveraging L2 solutions to reduce fees and congestion related to the Ethereum chain (processing 4.5 times transactions per second, saving 10 times fees). Due to the different underlying architecture, the Solana chain has higher deployment costs and currently has less DEX support. Raydium and Orca are the main DEX platforms that undertake exchanges on the SOL chain.

However, the Solana chain has high throughput and low transaction costs, so we are seeing more cross-chain solutions emerging, allowing assets to be transferred more seamlessly between different blockchains. The cross-chain platform ThorChain provides the exchange of native assets and performed well in Q4. Cosmos' IBC architecture enables interoperability between different blockchains and is also a potential solution for DEX multi-chain deployment.

We listed the multi-chain development of common exchanges on Ethereum among the top 20 market shares:

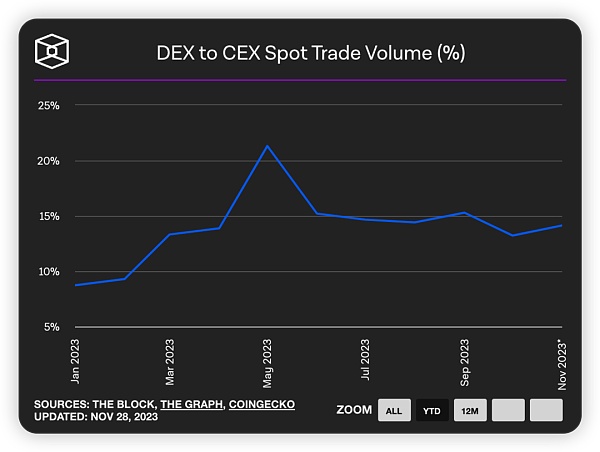

“The market share of DEX spot trading increased in the first two quarters, with the highest It hit 21.31%, setting a record high."

Then it fell back and stabilized around 15%. This continues the trend of the previous year, when the crisis of trust caused by the FTX thunder forced users to transfer their assets to DEX. At the same time, the user experience of DEX is also further optimized, such as Uniswap, Paraswap, etc., have successively launched their own wallet apps.

The most important thing is that DEX (especially AMM) allows users to add liquidity to long-tail tokens (such as meme tokens, etc.) without permission, which bypasses regulatory issues or other factors, leaving Remove the shackles of listing on centralized exchanges. With DEX, projects can channel liquidity immediately, allowing for greater market participation. According to data from CoinGecko, Uniswap has almost 20 times more coins listed than Coinbase and 3.4 times more coins than Binance.

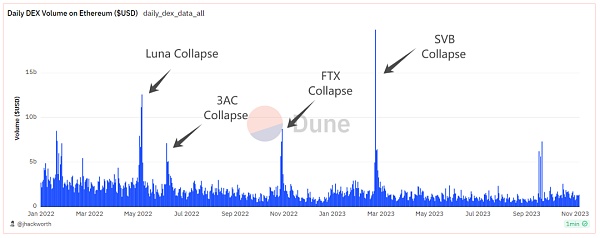

The most essential difference from CEX is , DEXs repeat what they are programmed to do: provide permissionless trading. During the days when centralized entities such as FTX, BlockFi, Celsius, and Voyager collapsed, DEX volumes surged, recording massive single-day trading days. The SVB collapse (and decoupling from USDC) resulted in the largest single day of DEX trading volume being ~$19.7B.

“MEV and large-scale adoption are still difficult problems facing DEX, and DEX has also launched many mechanism innovations this year.”

Uniswap is a representative example X: Allows users to sign orders offline, and solver Dutch auction execution; Maverick provides four modes, allowing to automatically follow prices or adjust liquidity in one or two directions; DODO V3 allows LPs to entrust funds to professional market makers Active market making increases returns.

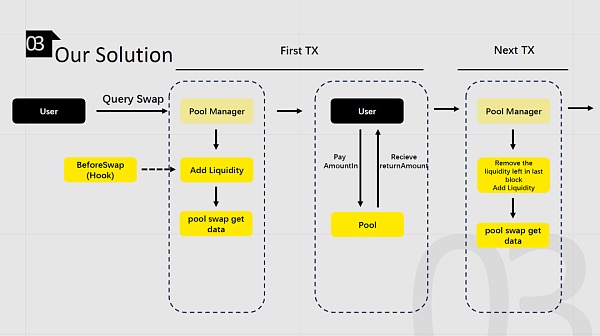

Hook in Uniswap V4 allows customizing the functions of the pool, providing an innovative platform with more possibilities for DEX. Based on this, the Aggregator_Hook developed by the DODO team created a system that can accurately map liquidity positions on various DEX platforms to Uniswap V4 quotes, simplifying LP operations and enhancing user experience and market liquidity.

Product Updates

Uniswap launches V4 and Uniswap X; Trader Joe launches AutoPool; Balancer V3, etc. will be launched soon

Uniswap front-end charges will charge 0.15% for transactions of certain tokens from October 17, causing huge controversy in the community

< /li>Curve issued crvUSD stable currency, with a total amount of ~$150M

Uniswap and Paraswap launched wallet apps

DODO's Hook aggregator Aggregator_Hook won the Best Hook Use Award at the Istanbul Hackathon

Governance Token

DODO suspends DODO emissions in the vDODO pledge pool and reduces the vDODO exit fee to 0%.

Pancakeswap launches veCake’s token governance model, enhancing $CAKE’s governance rights

Sushiswap targets transaction fees, routing Fees, staking fees, partnerships propose new SUSHI economic model

User experience

DODO will launch intelligent slippage prediction function

Matcha launches historical transaction query function

Sushiswap automatically detects "tax tokens"

Trader Joe's Quick-Picks intelligently recommends popular tokens

Pancakeswap’s Dumb mode allows automatic closing of positions after expiration

Hacking

On July 30, Curve was attacked by hackers. Due to vulnerabilities in the underlying code version, TVL fell by a minimum of 51%, resulting in a loss of US$62 million. Currently, about 79% of the funds have been successfully recovered

On September 20th and November 18th, the front-ends of Balancer and Trader Joe were attacked successively, resulting in losses of ~$238K and ~$87k respectively

DEX is the core infrastructure in DeFi and a bridge for circulation between different tokens. LP assets are also the mainstay of the underlying assets in many Defi protocols. TVL and trading volume can reflect market activity, and capital efficiency reflects the response of different DEX mechanisms to capital utilization. This year may be an inflection point for the market.

DEX has withstood the test of the market by operating without permission and supervision. In response to the crisis and market pain points, each DEX has made colorful and unremitting efforts, innovating along the way. Despite this, DEX still faces challenges in its development, such as hacker attacks, MEV, large-scale applications... But there is always a lack of newcomers in the market, which makes people shine.

DEX is always developing and has never stopped. It is bound to achieve a decentralized experience of market making without trust and threshold.

Why should your next exchange be CEX?

The carry trade has broken down, and in any case, the game is over for Japan.

JinseFinanceBinance launches Funding Rate Arbitrage Bot and expands Spot Copy Trading for traders during the bull run, streamlining arbitrage and offering strategies from experienced traders.

Huang Bo

Huang BoIf we follow the previous example of destroying MGP to obtain EGP IDO quota, there will be a strategy with relatively high profit and loss.

JinseFinanceThis article looks at the mechanics of CEX/DEX arbitrage trading, focusing on the AMM aspects of execution, aiming to show the relationship between block time, block base fee, and the participants involved in these trades.

JinseFinanceThe brick-and-mortar arbitrage model has actually been around for a long time. To put it bluntly, it means "buying low and selling high" and relying on the price difference to obtain profits.

JinseFinanceNFT tax-loss harvesting platforms witness a surge as the NFT market faces a downturn. Unsellable, Harvest.art, and others offer solutions, attracting users seeking to offset losses. The trend reflects a changing approach to tax strategies in the crypto space.

Bernice

BerniceAn exploration of arbitrage trading, a strategy that leverages price differences between markets to generate profit. This article covers various types of arbitrage trading, how it works, associated risks, and its profitability, emphasizing the importance of quick and efficient execution.

BerniceJinseFinance遵循这8条建议 避免掉入巨鲸的“套利陷阱”

fx168news

fx168newsA lot can be analyzed from here, and I strive to pass this incident so that I can learn more risk management knowledge, arbitrage strategies and risk avoidance actions.

Ftftx

Ftftx