This is 2023's crypto crisis

2022 was not crypto's year- and 2023 isn't looking so good either

Clement

Clement

The DeFi lending environment has changed dramatically over the past few months. This article will focus on a brief introduction of some new DeFi lending protocols, data analysis, and general trends that will affect the lending sector in the next cycle.

New DeFi lending protocol:

dAMM and Ribbon compete directly with Maple and Atlendis in the institutional (under-collateralized) lending space.

Arcadia, ArcX, and Frax are variations on existing models we've already seen in this space.

Many protocols continue to pursue product verticalization in an attempt to increase moats and value capture.

Frax: Stablecoin, AMO (Automated Market Operations), AMM (Automated Market Maker), Liquid Staking

AAVE: Stablecoins, Undercollateralized Lending, RWA (Real World Assets)

ArcX: Credit Scoring

Ribbon: treasury + loan

Some lending protocols are more focused on catering to long-tail assets (assets with low short-term demand).

On the institutional side, dAMM is the only one that already supports many long-tail assets.

Euler Finance allows borrowing and lending of any asset, some of which can be used as collateral.

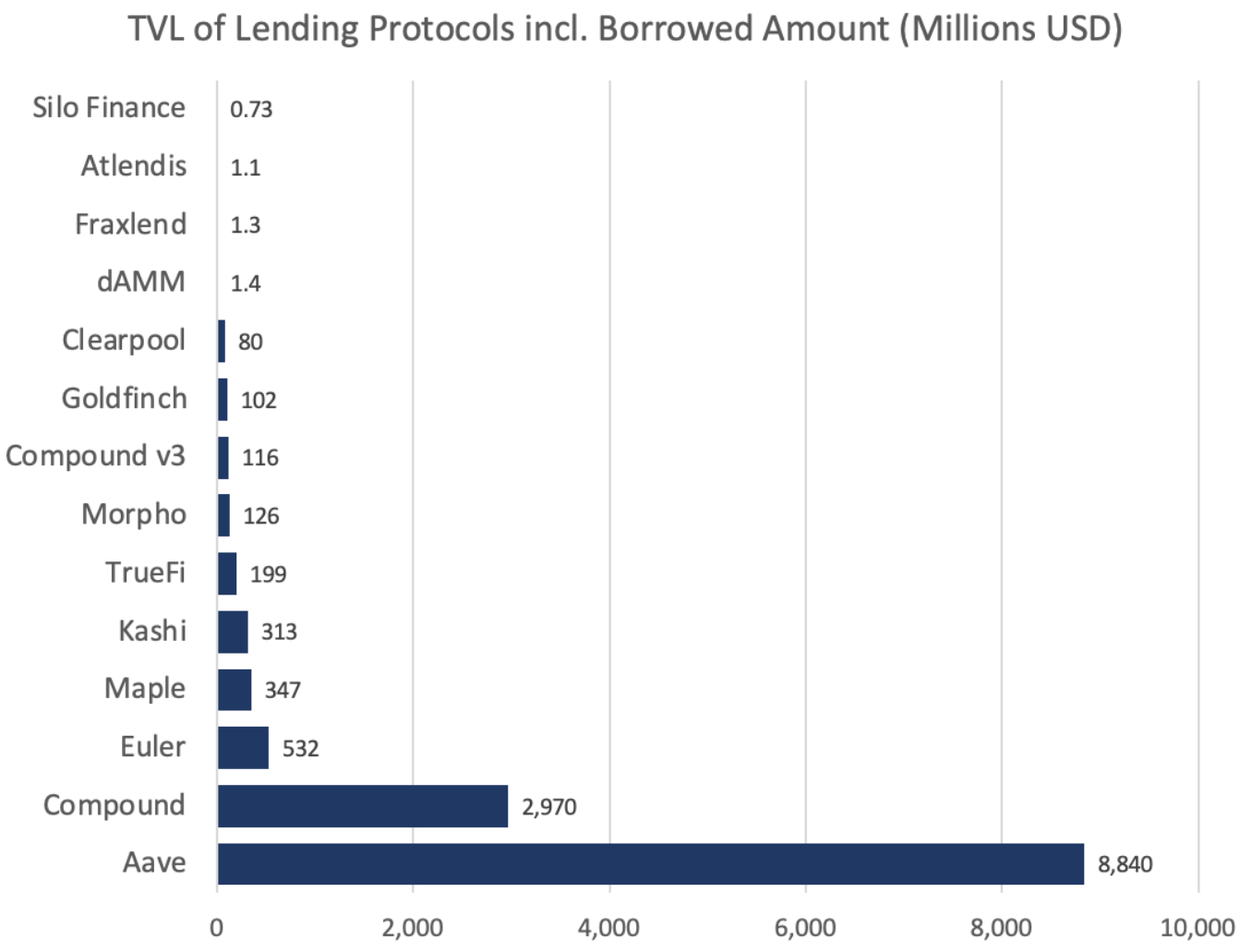

AAVE is the clear winner so far, due in part to its aggressive multi-chain deployment - 37% of its total TVL resides on L2 or EVM.

COMP v3 was slow to migrate funds from v2, which was firmly in second place.

Maple is the most popular under-collateralized lending protocol.

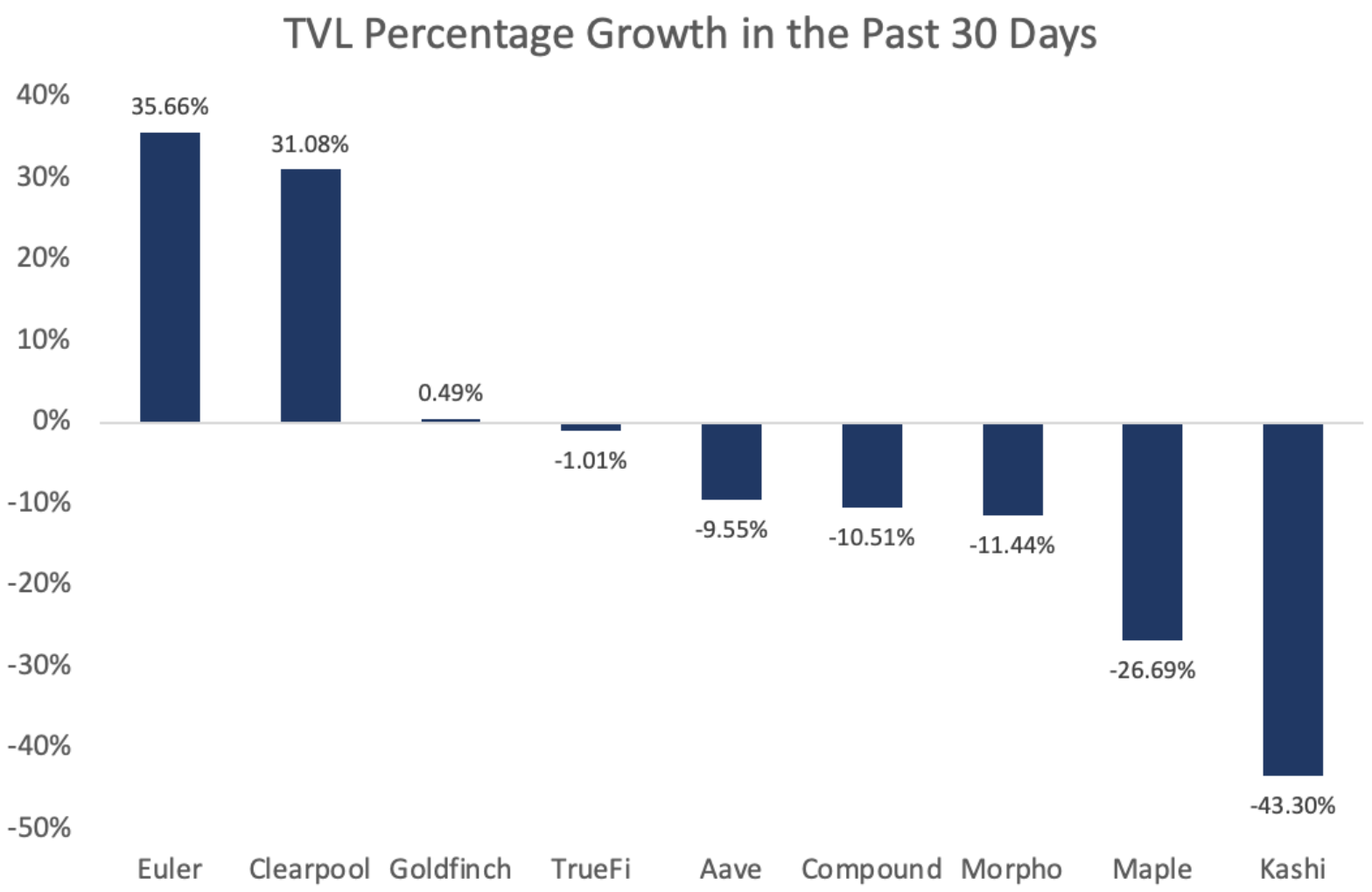

Euler and Clearpool are the only two semi-mature platforms that have seen substantial growth over the past month.

AAVE and Compound performed in the middle, with Kashi shrinking the most.

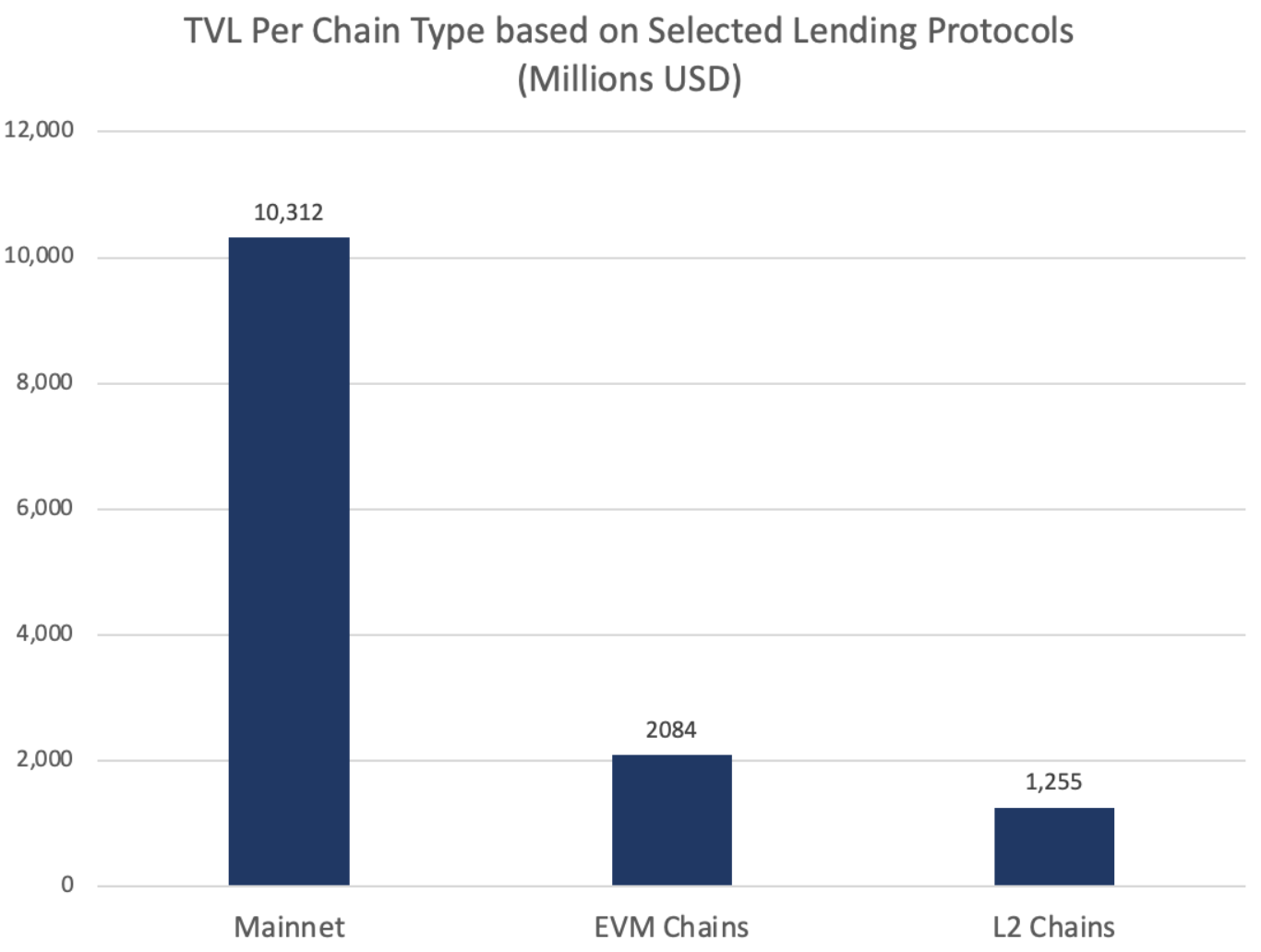

Most of the lending TVL is on the mainnet, but EVM and L2 are slowly gaining market share.

During the next cycle, increased usage and number of projects on L2 will accelerate demand, thereby increasing overall liquidity.

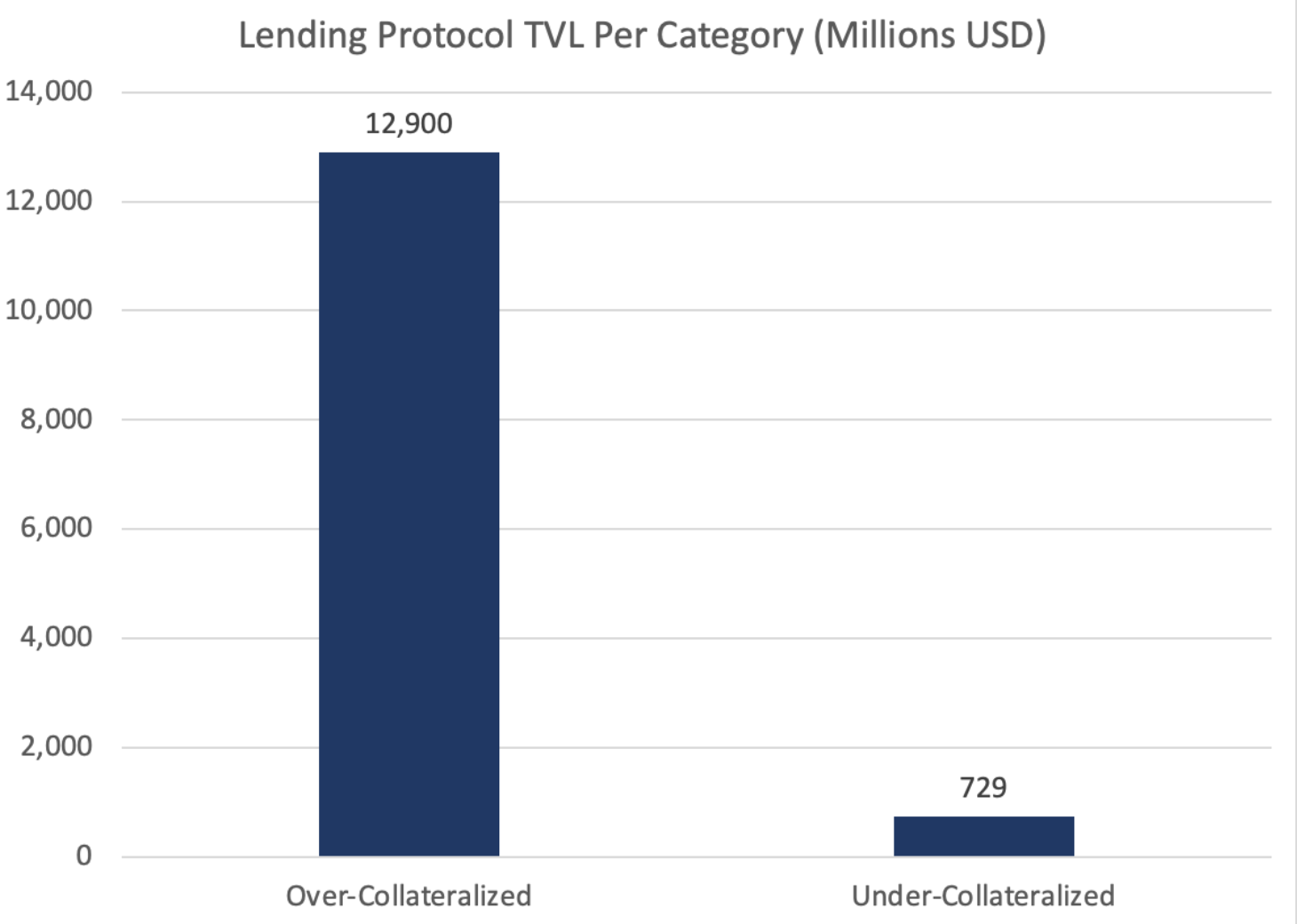

In terms of TVL per category, the overcollateralized model has so far dominated.

Expect this gap to narrow as KYC and ZK-based authentication unlocks new primitives, and more institutional capital comes on-chain.

As far as the lending of blue-chip assets and long-tail assets is concerned, blue-chip assets currently occupy almost all of the liquidity.

Euler is the most prominent protocol focused on long-tail assets with a TVL of less than 5%, mainly due to the opportunity cost of token staking.

Why deposit GRT tokens into Euler when (illiquid) staking can earn much higher APR (10-30x)?

This will change over time as we will see more liquid staking derivatives of web3 and DeFi protocols where tokens can be lent and earn yield at the same time.

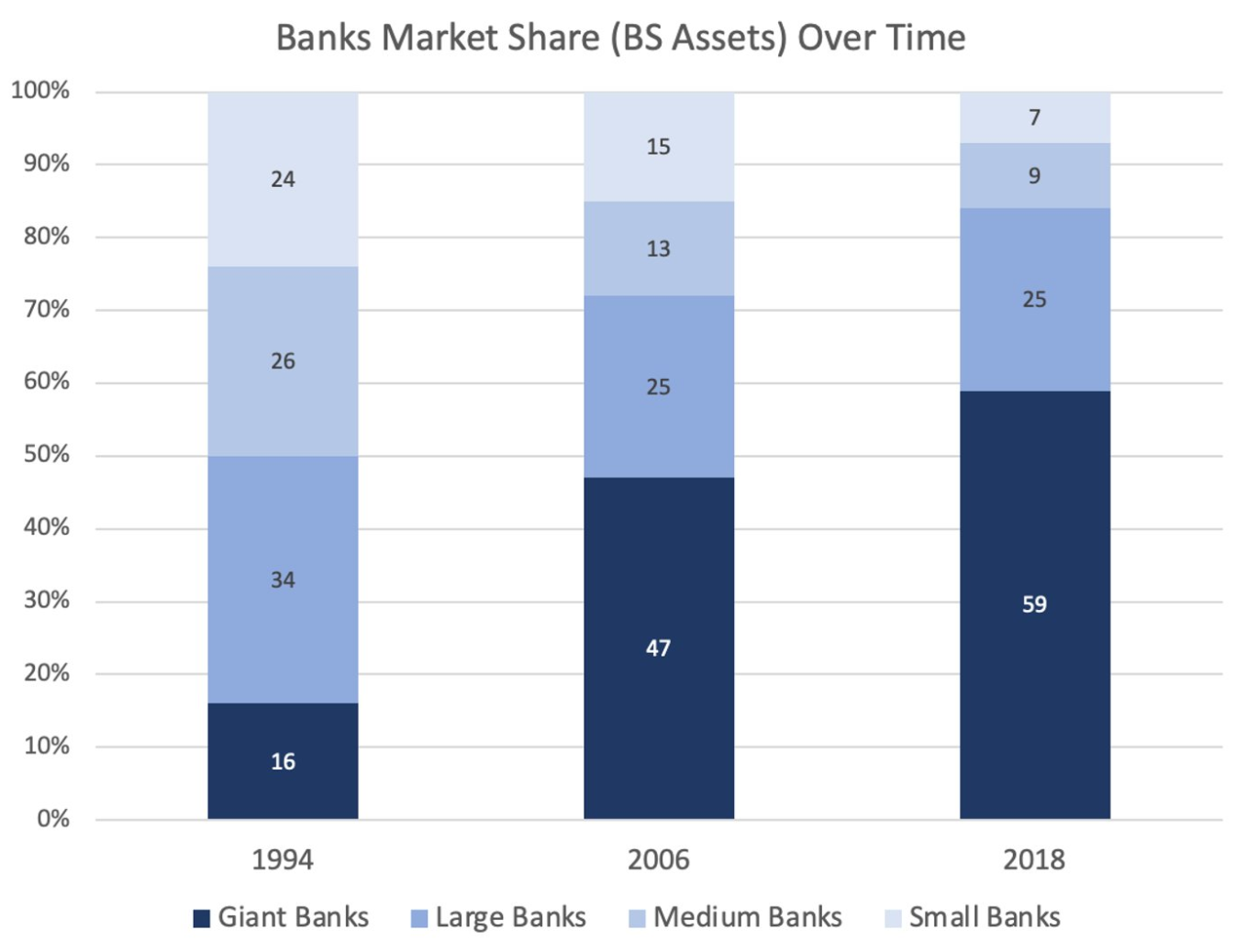

Verticalization is an interesting trend across DeFi, as lending isn’t the only area with an increasingly concentrated market share.

Lido, Uniswap, and MakerDAO have very large market shares in their respective categories.

Over time, we may see DeFi (and lending) continue to concentrate its share, similar to how large banks have grown over the past few decades.

There are three reasons: strong network effects, verticalization (turning products into features), and brand moats.

New Potential Lending Experiments:

1) Insufficient mortgage lending based on zk-proof off-chain collateral

2) Loans using social-based NFTs as collateral

3) Lending focused on DAO

2022 was not crypto's year- and 2023 isn't looking so good either

ClementThe valuations given to some of the tokens on the balance sheet are fiction.

Ledgerinsights

LedgerinsightsHow the composability of Web3 puts technological innovation and growth into maximum overdrive.

Beincrypto

BeincryptoChangeNOW is a scam! ChangeNOW illegally holds my money! ChangeNOW are thieves! These are some of the hostile comments that ...

Bitcoinist

BitcoinistAri Paul emphasized that Bitcoin "has a much better chance" than other cryptocurrencies because it has no competitors as a product.

Cointelegraph

CointelegraphPaul highlighted that Bitcoin has “far better odds” than other cryptocurrencies because it doesn’t have a competitor as a product.

CointelegraphThe U.S. Securities and Exchange Commission (SEC) Chairman Gar Gensler hinted at what could be the future of Bitcoin and ...

BitcoinistThe banking giant said Terra's debacle does not appear to have hurt the venture capital market, and that as long as venture capital remains in the cryptocurrency market, things will improve.

CointelegraphThe development of the metaverse has brought about an extremely complex socio-economic picture, which has a positive side and also brings many risks and challenges.

Ftftx

FtftxAccording to recent surveys, women are still half as likely as men to invest in cryptocurrencies and digital assets.

Cointelegraph