Signature Bank, Stablecoins Might Benefit From Silvergate Exchange Network's Demise

Coinlive

Coinlive

Author: LeftsideEmiri

Source: Frogs Anonymous

We all know the importance of stablecoins. They have quickly become one of the most popular offerings in cryptocurrencies over the past few years. Currently, the total market capitalization of all stablecoins is $157 billion, with USDT, USDC, and BUSD accounting for $141 billion. Currently 89% of the stablecoin market capitalization is dominated by three centralized stablecoins. In order to live up to the original purpose of cryptocurrency, we need to make some changes.

While centralized stablecoins are proven to be more secure than decentralized ones, they expose a large portion of the crypto ecosystem to the risks of centralization. In the long run, the lack of transparency combined with the reliance on centralized entities could cause problems for the industry as a whole.

Many people realized this early on and started experimenting with many different mechanisms in the hope of creating a truly decentralized stablecoin. Now let's take a look at the most popular mechanics so far, along with the risks and advantages of each.

There are currently four decentralized stablecoins:

Algorithmic Stablecoins

Unpegged Stablecoins

Overcollateralized Stablecoins

Some Algorithmic Stablecoins

Algorithmic stablecoins are one of the most controversial stablecoin mechanisms. They usually use a two-token model. One token is a stablecoin pegged to a fiat currency, and the second token is a native token meant to absorb the volatility of the stablecoin. Suppose the stablecoin is pegged to $1. When a stablecoin is minted, $1 worth of native tokens are burned. When a stablecoin is burned, $1 worth of native tokens are minted. Therefore, this mechanism controls the supply through an algorithm.

Algorithmic stablecoins are controversial because the mechanism has historically been unsustainable. The entire mechanism relies on the constant demand for stablecoins. Once demand and liquidity disappear, they enter what is known as a “death spiral,” a mechanism that undermines the design of stablecoins and native tokens. We’ve seen many algorithms suffer this fate steadily, including the ever-popular Basis Cash, TITAN, and UST.

Non-pegged stablecoins are very rare. Its core idea is to make stablecoins not pegged 1:1 to any legal currency. If one of the purposes of cryptocurrencies is to create an alternative financial system, then relying on fiat-pegged stablecoins is counterintuitive. The most popular non-pegged stablecoin is RAI by the Reflexer Finance team. These stablecoins are backed by algorithmically adjusted target prices and interest rates. Instead of fixing the asset at a certain price, use a PID controller to dampen volatility. This allows stablecoins to remain within a certain price range, with relatively stable prices, while reducing the risk of centralization linked to fiat currencies.

Then there are over-collateralized stablecoins. This is the first iteration of a decentralized stablecoin backed by the MakerDAO team. The premise is fairly simple: users who want to borrow stablecoins can only do so by over-collateralizing. Users deposit accepted collateral into the protocol and receive stablecoins in return for less than the value of the deposited collateral. As such, the protocol has sufficient collateral in its reserves to mitigate the risk of default and decoupling.

The last mechanism is a partially algorithmic stablecoin, pioneered by the FRAX financial team. Some algorithmic stablecoins try to combine the power of algorithmic stablecoins and collateralized stablecoins, mixing them together. In these systems, a portion of the stablecoin will be locked algorithmically, while another portion will be secured by eligible collateral. According to market conditions, the mortgage ratio will be adjusted. The worse the market environment, the higher the guarantee ratio; the better the market environment, the lower the guarantee ratio.

Even though there are so many different options for decentralized stablecoins, none of them can beat centralized stablecoins. To understand why, we need to look at the different risk profiles and the advantages of each mechanism. Through this, we can potentially identify a decentralized stablecoin and see if it can break the dominance of centralized stablecoins.

To analyze the risk profile, we will look at the following factors:

Mechanism Sustainability

Performance under different market conditions

potential source of attack

previous stress test

UST price chart

The first is algorithmic stablecoins. In general, this type of stablecoin is not sustainable. The lack of sustainability can be attributed to its reflexive nature. Considering that its stability is driven by high demand, algorithmic stablecoins rely on momentum and favorable market sentiment. Once the situation changes, reflexivity turns just as hard in the other direction, leading to the dreaded "death spiral." With the collapse of the stablecoin, its native token will also collapse, which will not only mean the end of the protocol, but also cause serious losses to investors.

So, obviously, in a bullish market environment, they do very well, and in a bearish market environment, they crash just as quickly. But you might be wondering, since the probability of a crash is so high, why would anyone choose to make it in the first place? This is mainly due to the fact that scalability is so easy to achieve. Reflexivity allows for faster growth and adoption of stablecoins. As in the case of UST, it reached such a high level of adoption at one point that many people relied on it, trying to create a Bitcoin reserve to achieve some escape velocity. This ultimately didn’t work out, but it shows how quickly algorithmic stablecoins can grow in favorable market conditions.

As far as the source of the attack is concerned, the most common is creating panic in the market. When there is illiquidity, it only takes a few large sell orders to cause a brief decoupling. A slight decoupling will create fear among participants as they begin to lose trust in the system. When fear starts to spread and people scramble to get out, stablecoins can crash completely — just push it over the edge just a little bit and it will panic the entire market. As a result, algorithmic stablecoins tend to underperform in stress tests. In the past, temporary dips have resumed, but most algos have been unable to recover from massive stress tests amid massive sell-offs and market panics.

RAI price chart

Then there are non-pegged stablecoins. We will use RAI as an example for our analysis as it is the most prominent non-pegged stablecoin in the market. From the perspective of the stability of the mechanism alone, it can be considered sustainable, mainly because the unpegged stablecoin itself will not be decoupled. Having prices float within a range, rather than being fixed at a certain price, makes it less likely that people will lose faith in the system. This system uses a mix of collateral and algorithms to dampen volatility. ETH is used as collateral to mint the stablecoin, while RAI’s interest rate and target price are adjusted algorithmically, incentivizing users to keep the price within a certain range.

Since launching in 2021, RAI has only faced one major stress test, with the price dropping from $3.52 to $2.89 in the first month. Its price has since stabilized between $2.90 and $3.10. Breaking out of current market conditions will now be considered a major success for the protocol. Given that there haven't been any major price moves yet, RAI has held up well in a bear market environment so far. In addition, the protocol locked a total of 39,861 ETH, and the system has 507,776 RAI remaining, which means the system is healthy.

The main source of attack for RAI comes from its reliance on PID controllers. In terms of stability, the PID controller enforces a negative feedback loop to ensure that the RAI remains relatively stable. However, if the market does not respond to the algorithmically adjusted redemption rate, it will cause the redemption price to become unstable, thus destabilizing RAI itself.

The PID controller is crucial to suppress the price fluctuation of RAI. In addition to the market being unresponsive to incentives, any compromises, disturbances, or vulnerabilities in the PID controller itself could compromise the stability of the protocol.

Another potential source of attack is governance. Even though Reflexer Finance is a governance-minimized protocol, there are still parameters left to governance that can lead to suboptimal outcomes for the protocol.

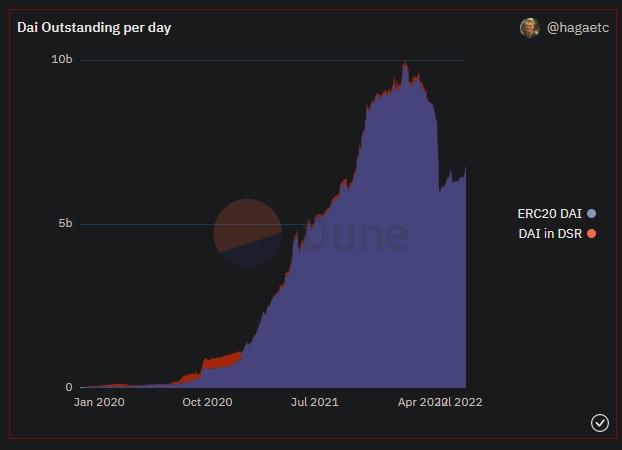

DAI supply

Overcollateralized stablecoins have proven to be the least risky mechanism for decentralized stablecoins. The fact that every stablecoin in circulation is backed by more collateral in reserves makes decoupling nearly impossible. To measure the sustainability of over-collateralized stablecoins, we can use DAI as an example. DAI has been around for years, and it has maintained its peg to the U.S. dollar during times of market downturn. It went through the most extreme stress tests and came out stronger. This further builds trust in the system, allows it to evolve and further maintains its stability, quickly putting it on track for long-term adoption.

While this low-risk approach has definite sustainability and stability, it has also proven to be a source of problems for the mechanism. Overcollateralization often results in very inefficient funding compared to algorithmic stablecoins. Simplifying the borrowing and lending experience from a user perspective can lead to more usage if less collateral is used to obtain greater leverage, allowing the system to scale faster.

In addition to being very fund-inefficient, over-collateralized stablecoins are also vulnerable to crises, depending on the quality of the collateral they accept. Most over-collateralized stablecoins accept collateral in the form of USDT, USDC, and ETH. Some protocols also accept other forms of crypto collateral. This kind of collateral is often exposed in the market. When the market is turbulent and down, if the value of the collateral is below a certain amount, there will be a great risk of liquidation. If the liquidation mechanism set by the protocol cannot be liquidated in an orderly manner, the stablecoin may lose some support, leading to decoupling. This risk becomes even more pronounced when the accepted collateral is a high-risk cryptocurrency asset.

The key takeaway from overcollateralized stablecoins is that the tradeoffs being made here are more in favor of security and sustainability than scalability and capital efficiency.

FRAX's changing market dominance chart

Finally there are partially algorithmic stablecoins. This type of stablecoin combines the security and sustainability of staking with the scalability and capital efficiency of the algorithmic model. Still, since the stablecoin is pegged to fiat, its system relies on arbitrage to maintain its peg. Therefore, if the market loses confidence in the solvency of the system, it is likely to be decoupled. Even if the reflexive feedback loops often associated with algorithmic stablecoins are minimized, there is still a degree of risk involved. So while it can be considered sustainable, there are some reservations.

This mechanism may perform well in all market conditions because the collateral ratio adjusts to market conditions. The only risk is the quality of the collateral - if the collateral accepted is riskier than during periods of high volatility, there is a risk of mass liquidations. So far, this hasn't been a huge problem. In the case of FRAX, it has only experienced two decouplings: one at $0.96 and another at $1.07. It has successfully recovered from two turbulences and has remained stable.

The main source of risk or attack on this mechanism comes from the solvency of the protocol. In the event of mass liquidations or collapse of the native token, the protocol could face liquidity issues. This can lead to a loss of confidence in the financial system, which can lead to panic and fear, which can eventually lead to the collapse of the system.

It is difficult for us to predict who will be the ultimate winner. The main determinants of the success of a stablecoin are sustainability and adoption. Adoption tends to occur in bull market cycles, and sustainability allows stablecoins to remain stable in bear market cycles as well. Being able to stand the test of time builds trust in the system, which leads to further adoption. So far, only over-collateralized stablecoins have stood the test of time. Unpegged stablecoins are a worthwhile product to try, but they are difficult to adopt due to the mindset of users. It will take time for users to get used to the concept of transacting with fiat-pegged stablecoins.

This leads to some algorithmic stablecoins. Sustainability, capital efficiency, growth, and safety, they all seem to have it, but they still face issues when it comes to accepting eligible collateral. For example, 90% of the collateral on FRAX is USDC, essentially making it a stand-in for USDC at times.

I believe the stablecoin winners in the long run will be non-pegged or partially algorithmic stablecoins. Under adverse market conditions, over-collateralized stablecoins appear beneficial but not strong enough to support mass adoption, while algorithmic stablecoins are too reflexive to be a viable long-term solution. Non-pegged stablecoins and partially algorithmic stablecoins are relatively new experiments, but the system will become more robust over time. Both types of stablecoins fit most criteria when looking for viable solutions. In order to live up to the true spirit of decentralization, we need decentralized stablecoins. Whichever of these two mechanisms survives a bear market and grows aggressively in a bull market will one day be the big winner.

Coinlive Crypto market participants continue to recalibrate following the abrupt shocks emanating from FTX’s woes.

Coin Metrics

Coin MetricsThe Markets in Crypto-Assets framework stands to get in the way of Circle's Euro Coin and other digital assets. Policymakers should revise the proposal.

Others

OthersThe proposed legislation being discussed by the House Financial Services Committee criminalizes stablecoins issued without due approvals.

OthersWazirX will start to convert Tether (USDT), Pax Dollar (USDP), and True USD (TUSD) into Binance USD (BUSD) after delisting the other stablecoins on Sept. 26.

Beincrypto

Beincrypto08 August 2022 – WEB5 Inu, a decentralized finance cryptocurrency, has launched several decentralized finance utilities as it plans to ...

Bitcoinist

BitcoinistIn a recent report, Cred Protocol just disclosed its first credit scores for decentralized finance users. The protocol is a ...

BitcoinistWith the crypto market crash has come a renewed interest in the cover that stablecoins provide investors. As a result ...

Bitcoinist Nulltx

NulltxSnoop’s first NFT collaboration with digital multimedia artist Coldie, “Decentralized Dogg,” was released today on SuperRare.

Cointelegraph

Cointelegraph