Golden Chart | Bitcoin holdings by governments around the world

The US government wallet address sends 4,000 BTC to Coinbase.

JinseFinance

JinseFinance

Author: Hal Press

Source: Bankless

With the Ethereum merger looming, what should we think about the Ethereum ecosystem and the price action of ETH? This long article by Hal Press may give us some useful references (note: there are deletions, this article is for reference only, not investment or trading advice).

The argument for the merger has not changed, Ethereum will undergo a massive structural shift and fees will effectively drop to zero. This shift will give rise to the first massive structural demand asset in cryptocurrency history.

First, we want to highlight some aspects of Ethereum's core model to understand some key fundamentals such as supply reduction and combined collateralization ratios.

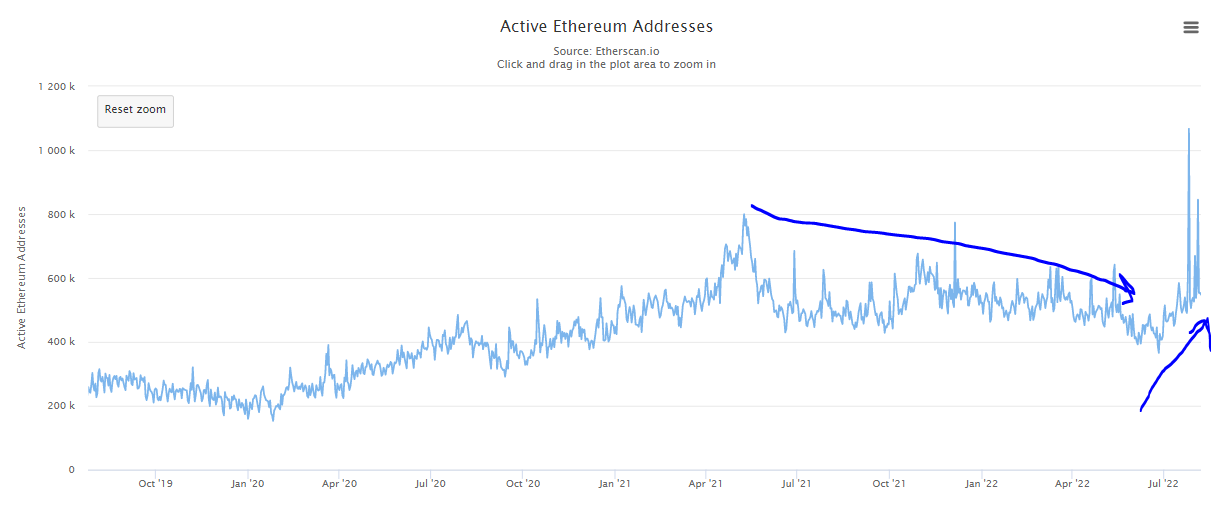

The biggest change since December is the massive drop in ETH-denominated fees. However, there is an interesting dynamic here. While fees have declined, active users have been on a steady upward trend since late June.

This seems counterintuitive since more users should result in higher gas fees. We believe this dynamic is caused by recent efficiency optimizations for various popular Ethereum applications. The most notable example is Opensea, which improved gas efficiency by 35% when migrating from Wyvern to Seaport. Therefore, the gas fee will be reduced, which does not mean that the activity will decrease.

In fact, multiple indicators suggest that despite the lower Gas readings, activity has been increasing recently (more on that later). This raises an interesting question: what is the optimal operating fee rate for Ethereum? Higher fees mean more ETH is burned and when combined are also associated with higher collateralization ratios, but these higher fees also limit adoption.

As we'll see in 2021, when fees become too high, some users get pushed to other L1 ecosystems. With a properly scaled rollup, Ethereum should be able to achieve both high fees and sustained adoption. We believe the sweet spot is around the point where fees are high enough to burn all newly minted tokens. This will stabilize the ETH supply while keeping fees low enough not to inhibit adoption. Interestingly, fees have found an equilibrium around this point recently. Lower fees also appear to have had a positive impact on adoption, with active users starting to increase after a long-term downward trend.

Although we appear to be close to an optimal operating fee rate, the reduced fee does have a negative impact on the output of various models. This effect is not significant because at the current operating rate, the ETH burned is still large enough that ETH will be slightly deflationary after the merger. Importantly, current operating fee rates will continue to drive structural demand, as most of the released ETH is unlikely to be sold, while used fees must be purchased on the open market.

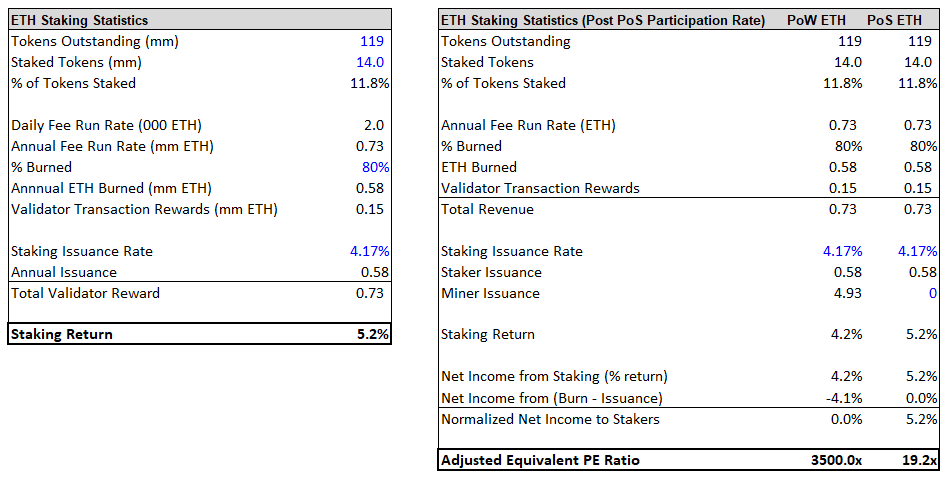

The combined collateralization ratio will increase by about 100 basis points, from 4.2% to 5.2%. However, this does not properly account for the real impact. To fully appreciate this shift, we must assess real, not nominal, rates of return. While the nominal yield is currently ~4.2%, the real yield is close to zero as 4.4% of new ETH is issued each year. In this case, the actual yield is currently ~0%, but will increase to ~5% after the merger. This is a massive shift that will go a long way toward creating some of the highest real yields in cryptocurrencies. The only other comparable yield is BNB with a real yield of 1%. A 5% yield on ETH would be a market leading figure. What is the meaning of this rate of return?

Stakers will earn a net 5% interest rate, which equates to 100/5 = ~20x yield. This multiple is much lower than the earnings multiple because the staking participation rate is low, meaning that stakers receive a disproportionate share of the total rewards. This is one of the key advantages of ETH from an investment perspective.

There are many other uses for ETH throughout the crypto ecosystem, and most ETH ends up locked in these applications rather than being staked. This, in turn, allowed investors to earn super-high real yields.

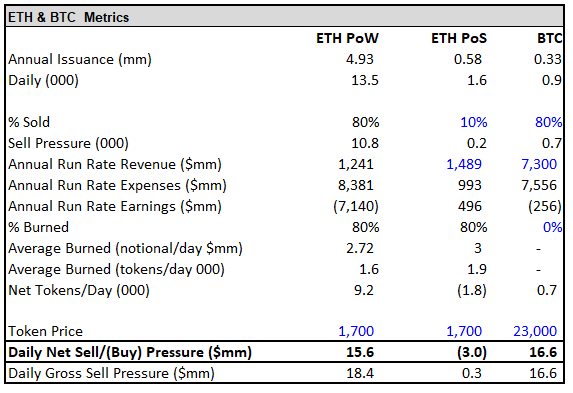

On the flow side, ETH will transition from a sustained ~$18M/day structured outflow to ~$300K/day structured inflow. While the flow equation on the demand side has softened, the full reduction on the supply side remains the most important variable. Our estimate of ETH-denominated supply reduction is actually larger than before. This is due to the price drop from the highs not being accompanied by a corresponding drop in hash rate. As a result, the profitability of miners has dropped significantly, and they may be selling close to 100% of their ETH.

For the sake of calculation, I assume that 80% of the miners' ETH has been sold. In this case, ETH has found an equilibrium, with miners selling about 108,000 ETH ($18 million) per day. Considering that the average fee is around $2 million, this would result in a net outflow of $16 million. After the merger, this selling pressure will be reduced to zero, and it is expected that there will be a structural inflow of about 300,000 USD/day after the merger.

In summary, while many of the numbers have changed significantly over the past eight months, the conclusion remains largely the same, and ETH will go from needing $18 million in new inflows to keep prices from falling, to needing $300,000 in outflows to keep prices from falling. prevent price increases.

To sum up, the pledge rate and structural demand have decreased compared to 6 months ago. However, this is to be expected in periods of slow activity, and if activity continues to rebound, these ratios will rise.

Another point that I think is often overlooked here is that consolidation is not just a shift in supply and demand. This is also a massive fundamental upgrade for Ethereum as the network becomes more efficient and secure in many ways. This is one of the differences between the Ethereum merger and the previous Bitcoin halving.

Compared to the fundamental decline in the case of Bitcoin halving (declining security), here the supply is greatly reduced and the fundamentals are greatly improved.

Finally, there are two more factors worth discussing.

1. Time Harvest

We also need to lay some background groundwork.

Why has the SPX (or pretty much any US/global stock index) been a long-term profitable and stable investment vehicle? Most agree that this trend is driven almost entirely by earnings growth and P/E expansion. They will assume that if economic growth slows, or if price-to-earnings ratios stop expanding, those investments are unlikely to earn positive returns in the future. This is not correct.

The main and most reliable source of price growth for these indices is the passage of time.

This example illustrates the point well. A lemonade stand, lemons(lemons = business, $lemons = lemons stock), earns $1 per year. There are 10 shares of $lemon stock outstanding. Lemon has no cash or debt on its balance sheet. The market is currently valuing $1 growth stocks at 10x earnings. How much are lemons worth now? What about $lemons per share?

If we assume that lemons will continue to make $1 a year next year, and the market is at the same P/E ratio, what will lemons/$lemons be worth a year from now?

If the answer to the first set of questions is $10/$1, you got it right. If the answer to the second set of questions is $10/$1, it is wrong. In the first part, the lemon is worth $10 because the market counts its $1 earnings as 10 times, and its value on the balance sheet is 0. The second part, the market is still trading at 10 times earnings on $1 of earnings, but importantly, it also allocates $1 to $1 of cash on Lemon's balance sheet. Lemons are now worth $11, or $1.10 per share. When a company makes money, the money doesn't disappear, it flows into the company's balance sheet, and its value flows to the owners of the business (equity holders). $Lemons appreciated 10% in a year because of the earnings they generated despite 0 growth and 0 P/E expansion.

This is the power of yield versus the passage of time.

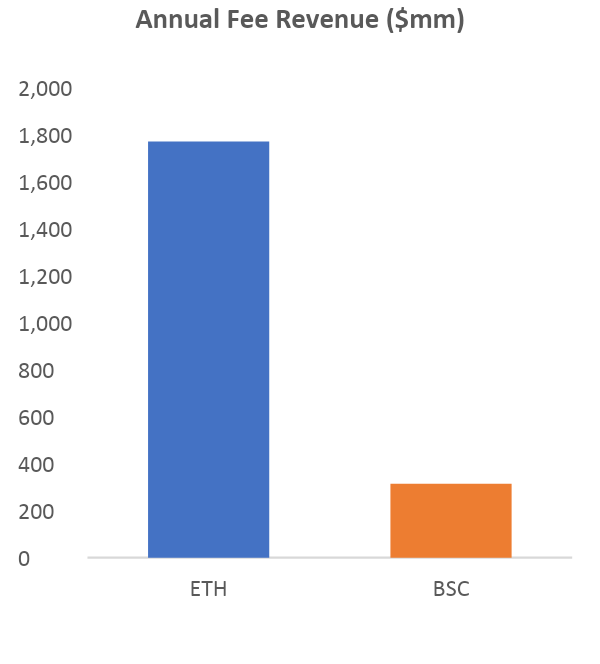

Cryptocurrencies have not benefited from this dynamic at all. In fact, cryptocurrencies have actually been affected in the opposite direction. Since nearly all crypto projects spend more than they earn, they must dilute their holders to generate the funds necessary to cover their negative net income. Therefore, unless earnings grow or its P/E ratio expands, the price per token will drop. The most notable exception I can think of is BNB, which is currently the only L1 whose revenue is greater than its expenses.

When ETH transitions to PoS, it will enter this exclusive category. The combined ETH will generate a real yield of about 5%. This rate of return will be very different from almost all other (except BNB) L1s, whose investment rate of return comes simply from inflation that offsets the rate of return. All other things being equal, ETH holders will receive 5% per annum. For 99.9% of other projects, time will be a tailwind rather than a headwind.

It will also change the psychology of holders, incentivizing them to adopt a stronger long-term buy-and-hold strategy, effectively locking in more illiquid supply. Additionally, the "real yield" theory and the fact that ETH will be the first mass real yield crypto asset will be of particular interest to many institutions and should help accelerate institutional adoption.

2. The Wall of Worry

Over the past few months, investors have been extremely skeptical of technical risks, edge cases and timing risks.

A recent fringe case that has attracted attention is the possibility that Ethereum’s PoW fork may survive the merger. Some PoW supremacists (miners, etc.) prefer to use PoW ETH, and believe that the current forked version of ETH is superior to ETC, which already exists as a PoW replacement. We don't think there's much value in forking, but our views on the issue aren't particularly relevant.

Importantly, this fork will not have an impact on the merged PoS ETH. All potential risks are either easily managed or not risks at all. For example, replay attacks will most likely not be an issue since PoW chains are unlikely to use the same chain ID. Furthermore, even if they maliciously choose to use the same chain ID, it can be managed by not interacting with the PoW chain or sending assets to the split contract first.

Finally, even if a user suffers a replay attack, it will only affect that user's personal assets and not the health of the entire chain. What PoW forks do is provide dividends to ETH holders, further increasing the value of the merger. If the forked coin has any value, ETH holders will be able to send it to exchanges and sell the forked coin for additional capital, most of which will be recycled back into PoS ETH. While we think this is good for the merger-related investment case, many are concerned about potential risks and a host of other fringe cases. We weighed each risk and concluded that the benefits far outweigh the risks.

Still, these concerns sideline many longtime believers.

Many of these issues will be resolved as we get closer to the merger. Eventually, many skeptics will change their minds, and as the event draws closer, creating momentum for continued inflows, there will eventually be a large number of buyers buying ETH on the day the merger succeeds. That should help offset any "sell the news" dynamic.

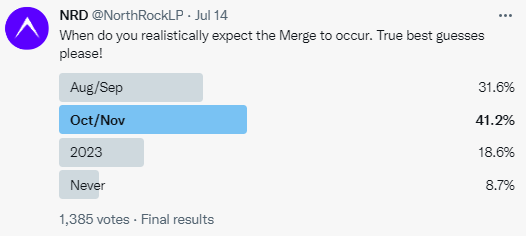

Just last month, less than a third thought the merger would happen by October. Now, that date has been confirmed as mid-September, but the market still sees only a two-thirds chance of it happening by October.

Against this backdrop, how should we expect price movements as the merger looms? This is the core issue.

First, we acknowledge that despite consolidation, macroeconomics will still have a significant impact on absolute price levels. However, it is still reasonable to consider how the merger-related alpha will develop in the coming weeks. It seems to us that the farther you go, the less predictable the path becomes, but at some point, when you get far enough, it starts to get easier again.

While a narrative has built up around the merger, positioning remains fairly loose among the more casual segments of the market. Perpetual funding has been negative for most of the rally since June, suggesting that there are more bears than bulls in the perpetual contract market.

Recently, another notable discretionary ETH exposure long position on Bitfinex was reduced to lows.

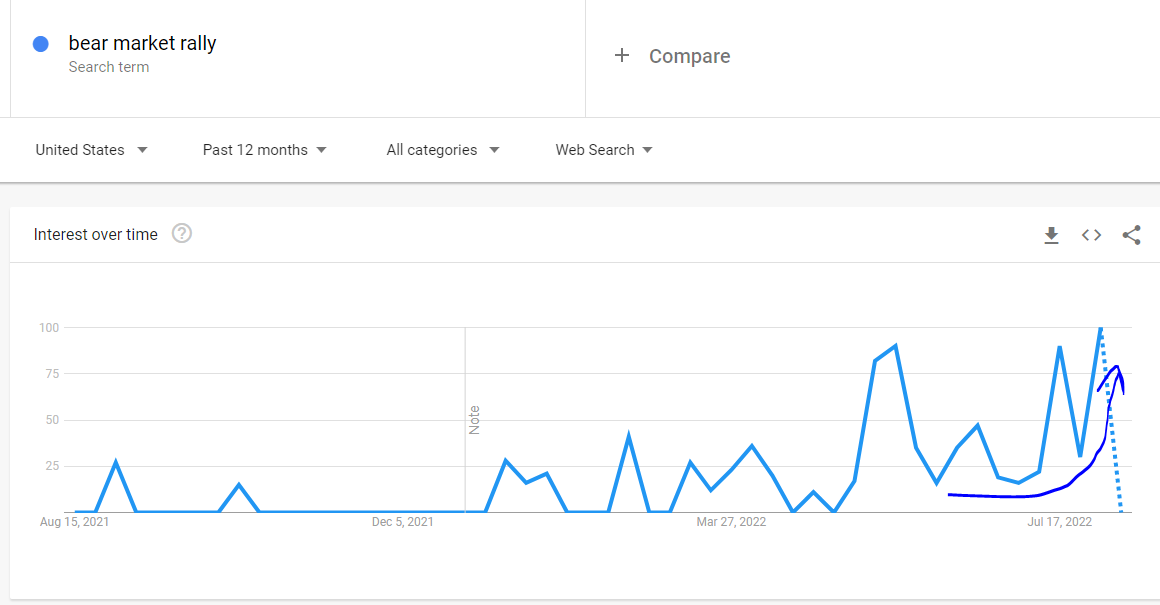

It seems to me that this lower positioning is likely due to the fact that many of the larger players see this as a "bear market rally" and therefore want to hedge as we continue higher.

Historically, there has been a large group of investors leaning in the direction of BTC supremacy and always looking to downplay the merger narrative. Their arguments revolve around one of two central points.

The first is: "For the past 6 years it has been said that the merger is 6 months away." The second question is about technical/execution risk. After assessing the time and execution risks, we became familiar with both. Earlier this week, core developers set a date for the mainnet merge of September 15-16 following the successful merger of the final testnet Goerli. The rest is coordination.

While many are concerned about execution risk, the upgrade has been tested extremely rigorously over many years and cross-checked by many teams. Furthermore, one of the core pillars of Ethereum is resilience. That's why there are so many different clients - redundancy is like a safety net against a single edge case or bug. Multiple (usually two or more) unrelated contingencies need to occur simultaneously to affect the protocol.

This built-in resilience, the most accomplished development team in the space, and years of preparation give us reason to believe that technical issues (though risky) are unlikely to arise.

I expect the next four weeks to follow a similar path to the previous four weeks, given investors' cautious positioning and continued desire to "fade" trades. There are periods of palpable fear when people overanalyze extremely improbable edge cases. However, I don't expect the price declines to be significant during these periods, as there are many underexposed institutions looking to increase exposure in any weakness. Also, almost everyone who sells ETH in the next few weeks is just selling strategically with the plan to buy it back at some point before or after the merger happens.

This dynamic implies measuring net outflows. On the other hand, I hope that the hype surrounding the merger will be amplified as the merger date gets closer and the mainstream media reports it. I believe this paper is very convincing and digestible for both institutional capital and retail capital. I expect inflows to accelerate as the merger nears, creating higher highs and higher lows.

What happens once the merger actually happens? Normally, you'd think there would be a risk of a "sell the news" reaction. Many investors are worried about technical risks and plan to buy after the merger. They believe they will reap the structural effects of the merger without the technical risk. The post-merger period will also depend on how much FOMO is generated as we get closer to the merger.

We expect significant buying and follow through after the merger, as the merger effectively "de-risks".

We expect a period of range-bound trading by short-term traders selling, with this sell-off flow being absorbed by structural demand and larger, less liquid institutional accounts. Price action during this period is less predictable and depends on the macro environment. As I said before, the macro environment is unpredictable, but we try to provide some ideas.

The macro environment for cryptocurrencies is driven by one core metric: whether adoption is growing, stabilizing, or declining. This metric is influenced to some extent by the broader macro environment, but ultimately what matters most is the adoption metric. The reason this metric affects price is that adoption also drives long-term inflows or outflows of money. Simply put, when users adopt cryptocurrencies, they often also put new money into the crypto ecosystem, which is what drives the macro. The macro environment is unfavorable when adoption falls, neutral when adoption is flat, and compliant when adoption grows. So, what is the macroeconomic situation today?

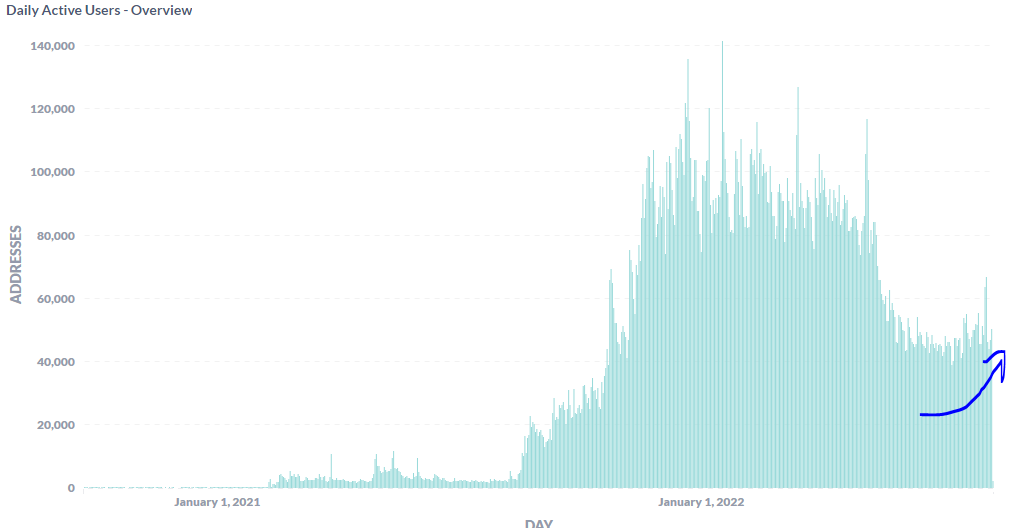

For the better part of the last 8-9 months, we've been in an environment of declining usage and the ecosystem has experienced a net outflow of users.

Daily active users showed a downward trend from May 21 to the end of June. Over the past 6 weeks, we have seen a nascent resurgence with a steady increase in user numbers. These are the green shoots of an economic recovery, suggesting a possible thaw in the macro environment. We were in a phase of declining adoption, and now, we're at least in a phase of steady adoption, and probably a phase of increasing adoption. A few other "green shoots" have emerged recently.

After weeks of redemptions, Tether began slowly minting new coins. After a long period of money outflows, new money is starting to come in again.

This effect is not unique to the Ethereum ecosystem, AVAX has also recently seen an increase in daily active users.

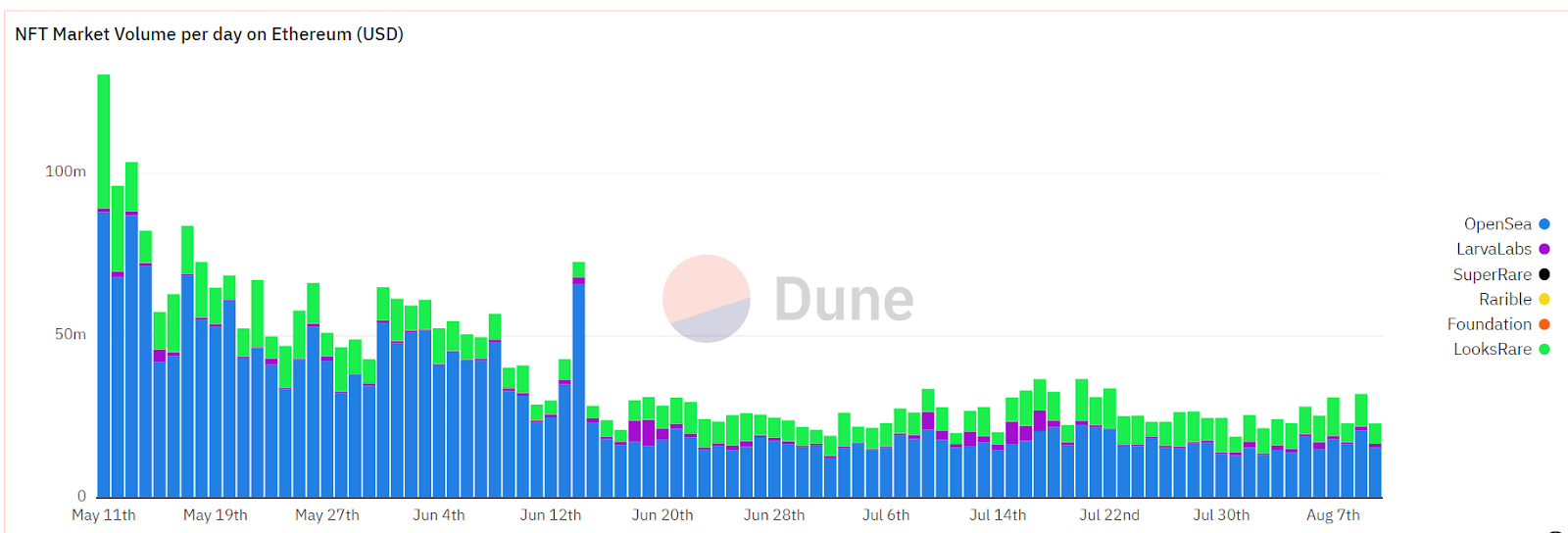

Recently, NFT users and transactions have been stable.

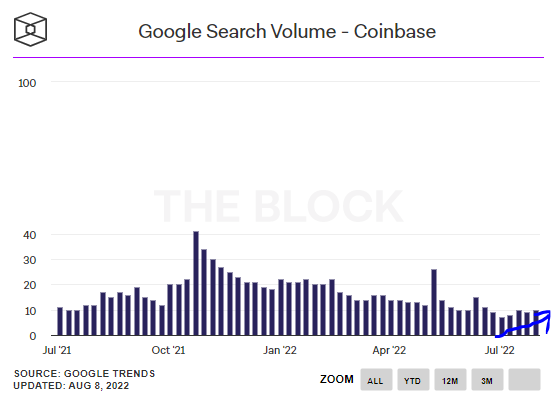

Certain web searches have started to have a positive impact, while others have been more stable.

These increases are not dramatic, unlike the exponential growth we saw at the start of the '21 bull market. That's why I call them "green shoots". They are still young and fragile, and may shrivel and die, but can grow into substantial progression if properly cultivated.

We believe the broader macro environment will play a key role in determining whether these "green shoots" live or die. For us, inflation is the most important macroeconomic variable. Therefore, we think there is a good chance that these "green shoots" will grow stronger if inflation moderates and the Fed is allowed to adjust and ease monetary policy. However, if inflation remains high and the Fed is forced to keep tightening policy, they will likely suffocate. We assess that moderating inflation is the most likely outcome, which should give these "green shoots" a chance to blossom.

Another advantage in favor of a more durable bottom is that a significant amount of investment from projects launched over the past 24 months has now been absorbed. In addition, the notional size of all future investments has been significantly reduced as investments in most projects have declined by 70-95%. Taken together, these two dynamics serve to intentionally reduce the overall daily supply that the crypto space has to absorb.

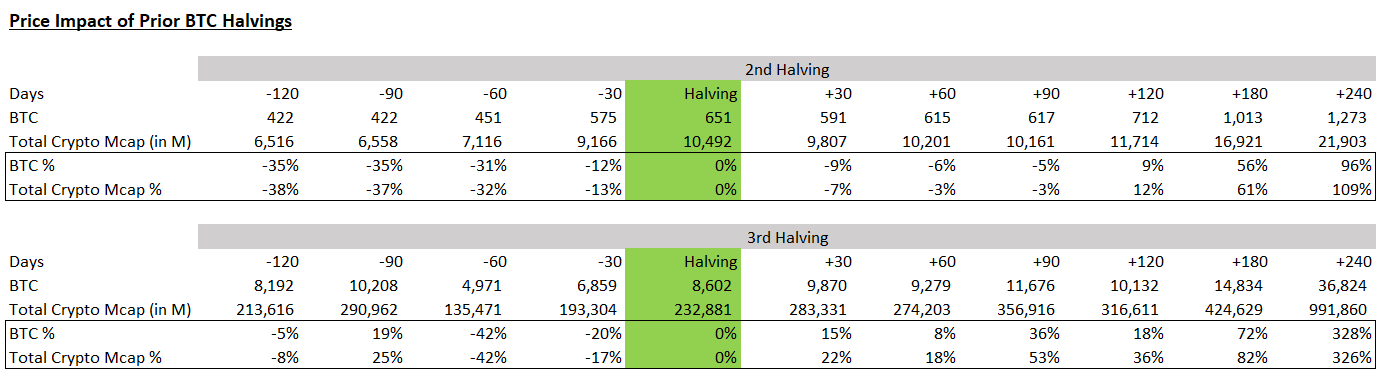

Finally, we think the last variable that affects this equation is merging. Investors are underestimating the impact of the merger on the macro environment across the sector. There is some uncertainty as to the extent to which supply reductions resulting from previous Bitcoin halvings drove subsequent price action rather than coincidentally matching the natural cycles of human sentiment and monetary policy. We acknowledge these uncertainties and believe there is an element of luck in the timing. However, we believe that reduced supply also has an effect, and the truth may be somewhere in between. Another common criticism is that changes in supply do not drive prices, it is changes in demand that matter. We disagree with this thinking. A decrease in supply is no different from an increase in demand.

Let's assume miners sell 10k ETH per day, we just add 10k ETH/day of buying pressure, not get rid of this selling pressure. This would have the exact same effect as removing miner selling pressure, but would be a change in demand, not supply. Clearly, both options have the same impact,

If we believe that Bitcoin’s halving has affected the macro environment for cryptocurrencies, then we should also believe that the merger of Ethereum will also affect the macro environment for cryptocurrencies. While Ethereum’s dominance was significantly lower than Bitcoin’s during Bitcoin’s last halving, the impact of the merger was almost as large (as a percentage of total market cap) as Bitcoin’s previous halving on the total market capitalization of cryptocurrencies, and absolutely significantly larger base.

The combined cryptocurrency will reduce the daily supply by approximately $16 million. This is not an insignificant number. To realize this, cumulative effects need to be considered.

We think a TWAP (Time Weighted Average Price) of 70k ETH per week will have an impact on the market. That's the effective effect the merger will have, unless it stops after a year; it's going to keep going. This has the potential to have a positive effect on the entire space as positive flow effects trickle into the rest of the market. This will provide an additional macro wind to help nurture those "green shoots" we mentioned earlier and increase their chances of survival.

Taken together, if the macro environment moderates, there is a good chance that the recovery from the capitulation bottom bounce will turn into a more sustainable and organic recovery, and consolidation should help this process.

In the long run, the future becomes easier to predict because structural flows are most important and easier to predict in this time frame. This is where the impact of the merger is most pronounced. We believe that as long as the Ethereum network continues to gain adoption, structural demand will continue to exist, as will further capital inflows. This should lead to sustainable and consistent appreciation for many years (hopefully decades) to come, especially compared to other tokens. We expect Ethereum to surpass Bitcoin as the largest cryptocurrency within the next few years, as we believe liquidity is the most important variable in cryptocurrencies. Ethereum will always be smooth sailing after the merger. Bitcoin will always face headwinds. To get an idea of what that might look like, take a look at the BNB/BTC chart.

BNB/BTC has grown steadily in this bear market and made multiple all-time highs despite the lack of narrative momentum. We think this is mainly because BNB is the only L1 with structural demand. The combined Ethereum will have greater structural demand than BNB on both an absolute basis and a market cap-weighted basis.

Ethereum consolidation is coming, there is no doubt about it. This would be the biggest structural change in cryptocurrency history, and right now, the Ethereum merger is undervalued.

The US government wallet address sends 4,000 BTC to Coinbase.

JinseFinanceThe world’s largest Bitcoin address dates back to October 2018, with a balance of 0.1 BTC (worth $660 at the time).

JinseFinanceOn March 11, Bitcoin exceeded $71,000 for the first time during the Asian trading session.

JinseFinanceIn its fourth-quarter financial report, MicroStrategy characterized itself as “the world’s first Bitcoin development company,” which is rare in history.

JinseFinanceSolana ($SOL) is primed for a potential surge, breaking out from a bull flag pattern. Analysts predict a 47% increase, propelling SOL's price to $150-$165. Despite recent challenges, growing adoption and positive sentiment contribute to a favorable outlook.

Edmund

EdmundAmong his early NFTs, "Crossroad," a commentary on the 2020 U.S. presidential election, made headlines by selling for $6.6 million in February 2021.

Brian

BrianA closer look at how it all started, the major hard forks, and where Ethereum is headed next.

cryptopotato

cryptopotatoDecentralized storage is an indispensable infrastructure for Web3. But at this stage, whether it is storage scale or performance, decentralized storage is still in its infancy and is far from centralized storage. This article selects some representative storage projects: Storj, Filecoin, Arweave, Stratos Network, Ceramic, summarizes and compares their performance, cost, market positioning, market value and other information, and analyzes the technical principles, Ecological progress is summarized.

链向资讯

链向资讯While Ethereum created history by taking over Bitcoin in the options market, the ETH futures contract entered price backwardation.

Cointelegraph

CointelegraphETH's latest plunge could bring more pain despite expectations that $1,200 should hold.

Cointelegraph