Decoding Bitcoin MEV: Insights and Implications

The reduction in mining rewards is a significant issue. As block rewards decrease further in the future, it could have various effects on the network.

JinseFinance

JinseFinance

Author: Shehan Chandrasekera, Source: TaxDAO

As the cryptocurrency industry rejoices over the long-awaited approval of a Bitcoin spot exchange-traded fund (ETF), investors must understand U.S. tax How the bureau will tax these products.

ETF is a financial instrument that allows investors to invest in a variety of assets and industries through a single share. Bitcoin ETFs allow investors to invest in Bitcoin without directly holding it.

The launch of ETFs involves multiple parties. In a Bitcoin ETF, an authorized participant (AP), typically a market maker or a large bank, provides cash to a grantor trust set up by a sponsor such as Ark Invest or Blackrock. The trust then uses the provided cash to purchase Bitcoins and issues trust shares to the AP representing the underlying Bitcoins. These ETF shares are then sold to retail investors through public exchanges such as the New York Stock Exchange or Nasdaq. ETF sponsors typically charge an annual fee (expense ratio) to cover their operating and administrative costs. As of December 31, 2022, the industry average expense ratio was 0.47%. Last but not least, the regulatory player, the Securities and Exchange Commission (SEC), must approve the sponsor’s application before the ETF can trade.

Futures Bitcoin (or any other cryptocurrency) ETF tracks the price of Bitcoin through futures contracts. Since October 2021, there are a variety of futures-based Bitcoin ETFs approved for trading, such as ProShares Bitcoin Strategy ETF (BITO), ProShares Short Bitcoin ETF (BITI), VanEck Bitcoin Strategy ETF (XBTF), etc. BITO is the market leader with $2 billion in assets under management.

Taxation of ETFs starts with capital gains assessment, but it doesn’t stop there.

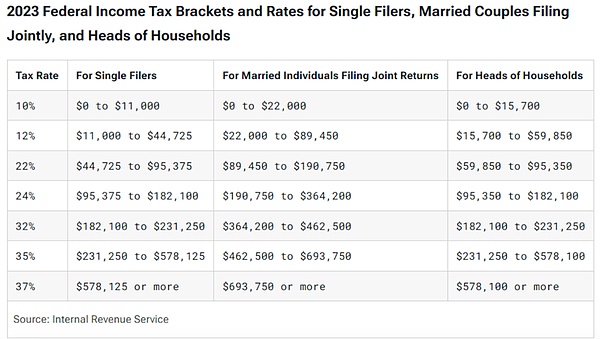

If you sell Bitcoin ETF assets after holding them for less than a year, the resulting short-term capital gains will be subject to ordinary income taxes. The tax rate may range from 10% to 37%, depending on your overall taxable income and filing status.

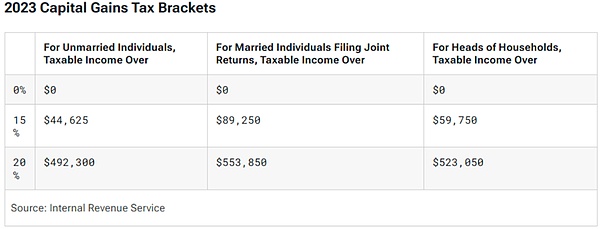

If you sell ETF assets after holding them for more than 12 months, then Long-term capital gains incurred will be subject to capital gains tax. The tax rate may be 0%, 15%, or 20%, depending on your overall taxable income and filing status.

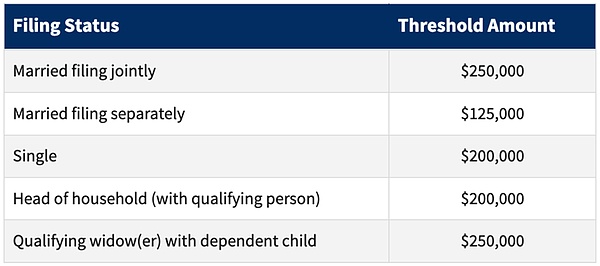

In addition, if your income exceeds the following thresholds, in addition to the capital gains tax mentioned above In addition, you may also be required to pay a 3.8% tax.

But this is not the only way to assess capital gains tax. Bitcoin ETFs cost a small portion of Bitcoin to cover management fees throughout the year. These transactions result in capital gains and losses due to the difference between the cost basis of the Bitcoins spent and their market value at the time of spending. For example, if a fund sold Bitcoin at a profit of $40,000 to pay management fees, those gains would be taxed proportionately based on each investor's holdings in the fund.

Prior to the passage of the Tax Cuts and Jobs Act of 2018, investors could deduct their pro rata share of fund expenses as a miscellaneous itemized deduction on Schedule A. Unfortunately, due to the restrictions introduced by the Bill, these expenses are not deductible now and will become deductible again after 31 December 2025.

A Bitcoin ETF based on a futures contract, such as BITO, may have slightly different tax implications for holders than a spot ETF. The specific details depend on how these funds are structured, particularly whether they have underlying exposure to regulated or unregulated (set forth in IRC § 1256) futures contracts. If the fund holds regulated futures contracts (which typically trade on the Chicago Mercantile Exchange, the dominant platform for Bitcoin futures), 60% of the gain is treated as long-term capital gains under IRC § 1256, regardless of the holding period. , 40% of the gain is considered short-term capital gains.

If a Fund has exposure to non-regulated contracts, gains are subject to normal capital gains rules similar to those for stocks. Please note that the taxation of futures contracts can be complex, depending on the facts and circumstances of the contract and certain tax elections made by the Fund and you. These factors can have a significant impact on when taxpayers pay their taxes and how much they pay.

Additionally, if you trade a crypto futures ETF, fund fees are typically paid in cash, which does not result in the same capital gains or basis adjustments as with spot ETFs.

ETF holders can file two types of tax compliance reports at the end of the year, namely Form 1099-B and trust tax information statements to satisfy tax obligations.

Brokers may issue Form 1099-B to report gains and losses resulting from the disposition of ETF units. This form will report the cost basis, sales price, and resulting gain or loss of the ETF units. (Under the proposed broker regulations, starting with the 2025 tax year, this information may be reported on a new Form 1099-DA specifically for digital asset transactions).

At the same time, the trust tax information statement will show the amount of Bitcoin used to pay management fees throughout the year. Using Bitcoin to pay fund fees may result in capital gains (or losses). This document will explain how to calculate your prorated share of the capital gain or loss incurred on these transactions. You must calculate this information manually by referring to the Trust Tax Information Statement because this information is not reported on Form 1099-B. These statements are unique to ETFs established as trusts. Most investors are likely unfamiliar with these statements.

Finally, in the year you sell the ETF, the basis reported on the Form 1099-B will need to be adjusted by incorporating the information reported on the Trust Tax Information Statement to arrive at the correct gain or loss. This can make tax compliance cumbersome for the average taxpayer. That’s why it’s important to continue to watch the progress of the next spot BTC ETF approval.

The reduction in mining rewards is a significant issue. As block rewards decrease further in the future, it could have various effects on the network.

JinseFinanceFor many large groups of non-crypto native capital, Ethereum has much lower buy-in as a key portfolio allocation.

JinseFinanceThe conference was held in Hong Kong. Does this indicate that Hong Kong and even China will return to a dominant position in the encryption industry?

JinseFinanceBitcoin's mining revenue has sharply declined post-halving, raising concerns about network security and miner profitability. Some miners may exit the industry, potentially compromising security. Industry leaders are taking proactive measures, but the situation warrants close monitoring for long-term viability.

Huang Bo

Huang BoTD Cowen analysts say MicroStrategy stock’s premium over BTC will compress but not disappear as spot Bitcoin funds come online.

JinseFinanceA mysterious transfer of $1.2 million in Bitcoin to Satoshi Nakamoto's wallet raises legal and identity questions.

Sanya

SanyaThis article will analyze the taxability of merged ETH and what it means for you.

Cointelegraph

CointelegraphCoinbase joins Grayscale in claiming that the SEC is failing to give spot market Bitcoin ETFs fair consideration.

Others

OthersLawmakers in a European country have drafted a 2023 budget that revealed a 28% tax on crypto assets held for under a year.

Beincrypto

BeincryptoIndia’s introduction of new crypto taxes had a negative impact on overall trading, forcing entrepreneurs to move to friendlier jurisdictions.

Cointelegraph