The Future of Ethereum ETF from the Success of Bitcoin ETF

For many large groups of non-crypto native capital, Ethereum has much lower buy-in as a key portfolio allocation.

JinseFinance

JinseFinance

Author: E2M Research, Steven Source: mirror

Looking back, the approval of Ethereum futures ETF seems a bit hasty. Ethereum is much more complicated than Bitcoin. The reason why Ethereum was rejected will definitely set an example for future crypto assets to apply for spot ETFs. However, in the traditional world, there are also ETF products for commodities with particularly wide usage scenarios such as pork ETF and oil ETF.

CM: Whether the spot ETF is approved or not does not depend on the technical level (POS or POW). The technical guidance is centralized, and the network is decentralized. The failure of Ethereum to pass means that subsequent crypto assets basically cannot pass, because from the perspective of decentralization, Ethereum is the second most decentralized product besides Bitcoin.

70% passed! ! ! ! Dongzhen: ETH is not large in scale, and Grayscale and other project parties are not very driven. From the perspective of game theory, it is not as driven as the Bitcoin spot ETF. There are no decisive events, such as BlackRock’s first application for Bitcoin spot ETF and Grayscale’s victory in the court lawsuit. 50%!!! 50%!!!

3.20

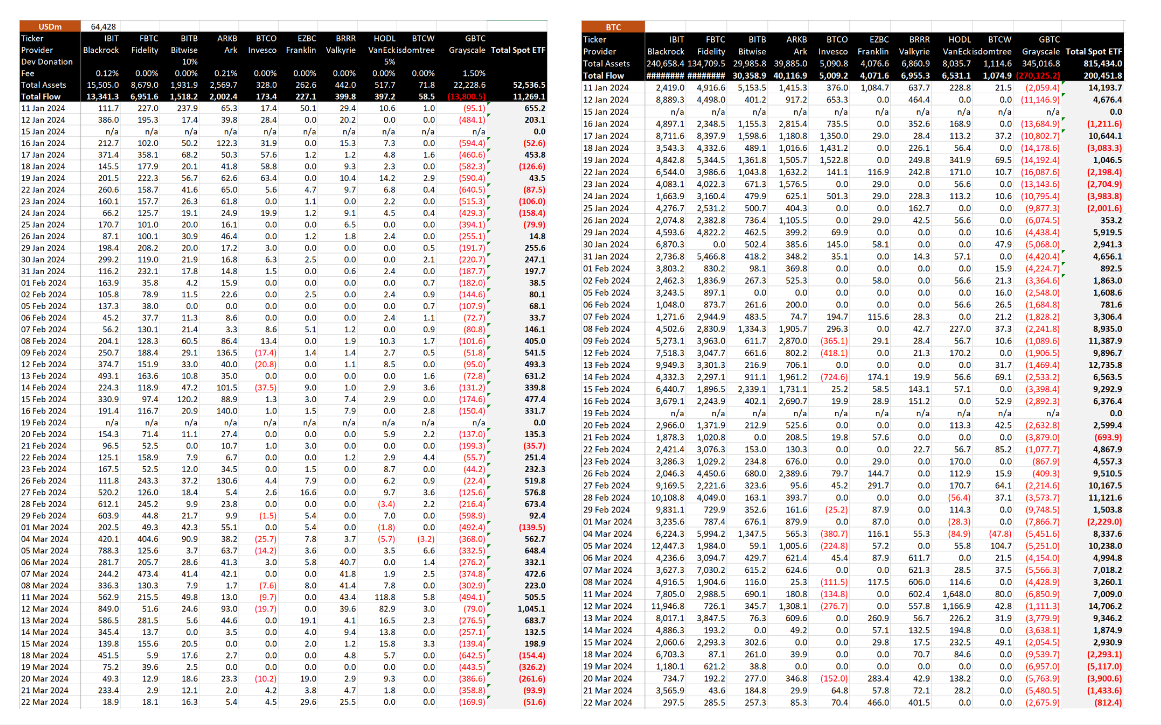

There has been net outflow for 5 consecutive days, but the total outflow has begun to narrow.

ETF Bitcoin holdings 800,000 pieces

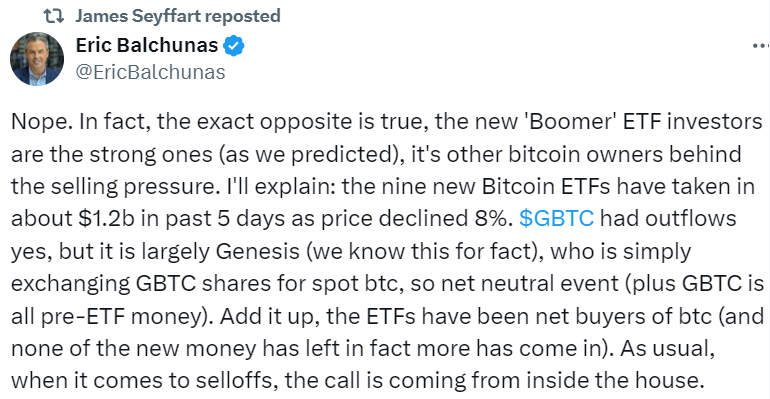

New ETF investors are strong, and selling pressure comes from other Bitcoin owners. In the past 5 days, the net inflows of the nine new (except GBTC) Bitcoin spot ETFs were about $1.2 billion, but the price fell 8%. GBTC did have outflows, but it was mainly Genesis selling, but he just exchanged GBTC shares for spot BTC, so this was a neutral event. All in all, ETFs have been net buyers of BTC, and more funds will flow in.

Text source: https://twitter.com/EricBalchunas

Supplement:

Cryptocurrency lending company Genesis declared bankruptcy last year, but on Wednesday, February 14, U.S. time, it was approved by the bankruptcy court to sell about 35 million shares of Grayscale Bitcoin Trust Fund (GBTC) worth more than $1.3 billion. The proceeds from this transaction will be used to repay creditors.

Source: https://cn.cryptonews.com/news/genesis-huo-fa-yuan-pi-zhun-chu-shou-yu13yi-mei-yuangbtc-jiftx-qing-suan-hou-zai-mian-lin-mai-ya.htm

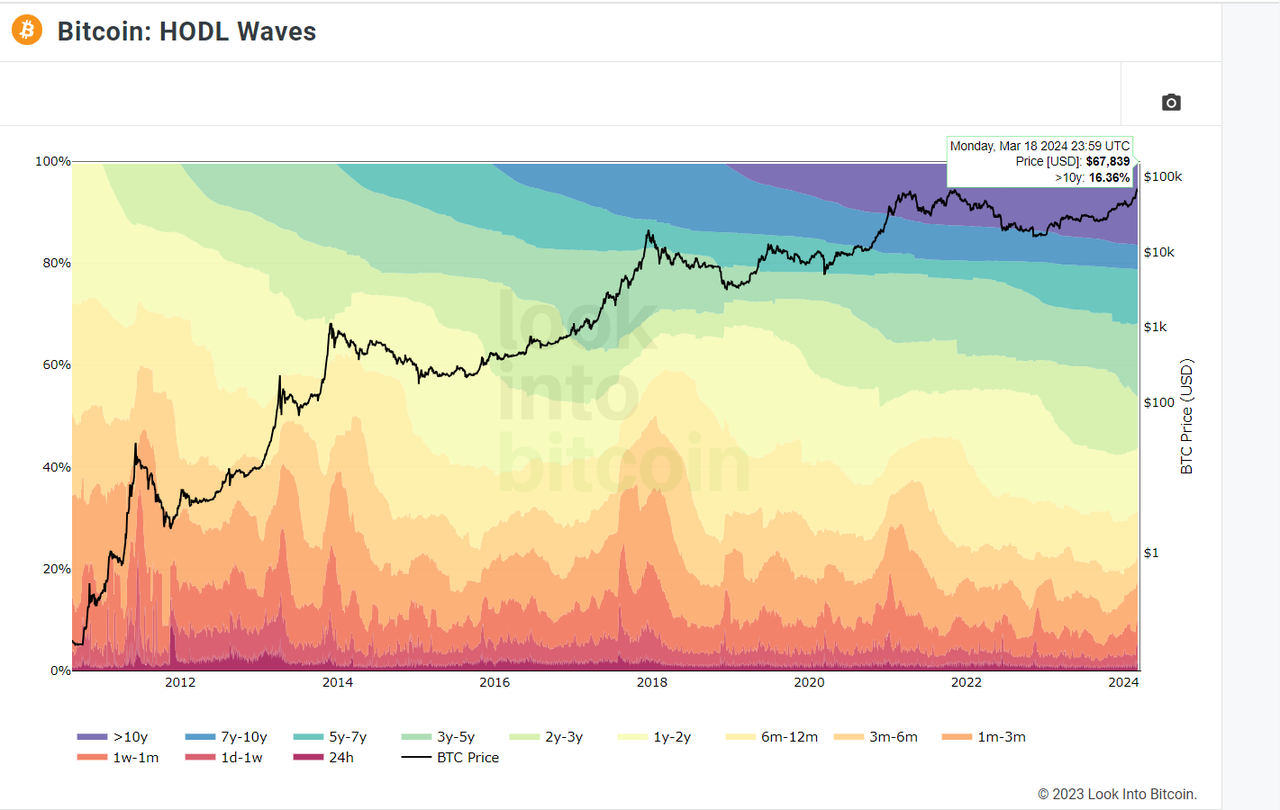

**16.36%** of Bitcoin has not been traded for more than 10 years, and most of this part may be the lost Bitcoin.

2100*16.36% = 3.4356 million bitcoins

Data link: https://www.lookintobitcoin.com/charts/hodl-waves/

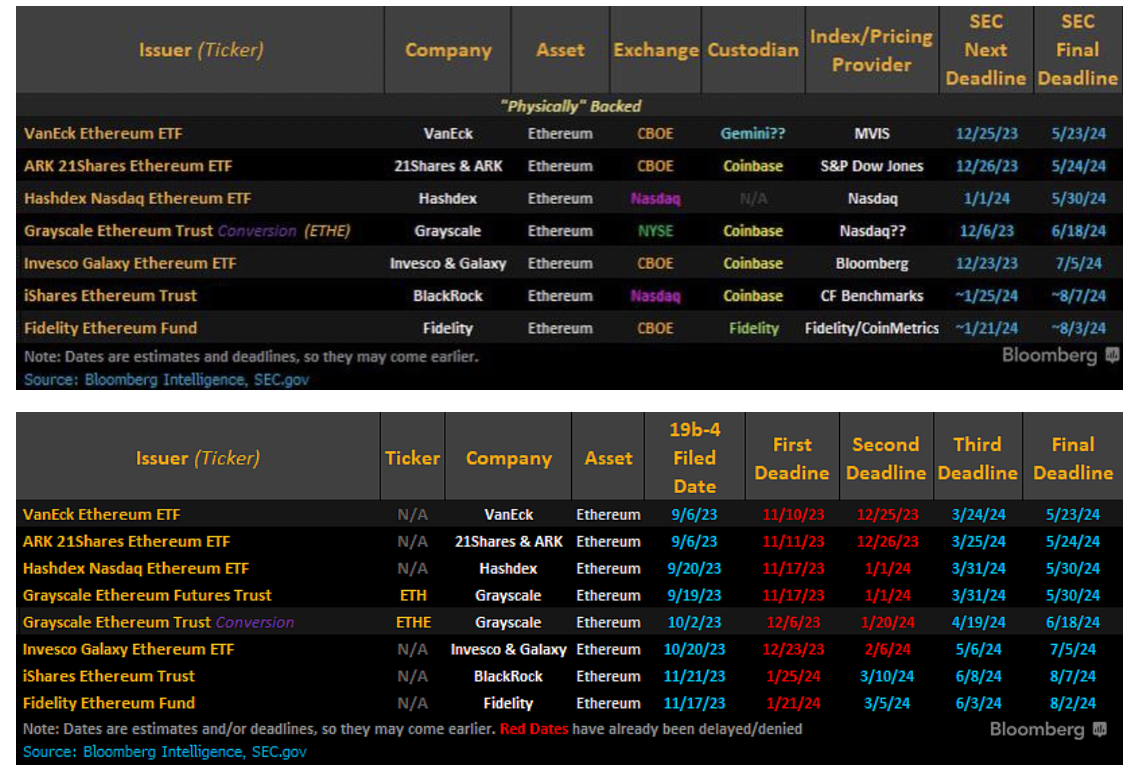

Application status of Ethereum spot ETF

Ethereum is defined as a security

According to the GitHub of the organization’s website repository, the Ethereum Foundation (a Swiss nonprofit at the heart of the Ethereum ecosystem) is facing questions from unnamed “national authorities.”

The confidential investigation comes at a time when Ethereum technology is undergoing a transformation, and its native asset ETH may be facing an inflection point, with many U.S. investment firms seeking to offer it as an exchange-traded fund. Despite the recent approval of a series of Bitcoin ETFs, the U.S. Securities and Exchange Commission (SEC) has been slow to make progress in its efforts.

After this article was published, Fortune reported that the SEC is seeking to classify ETH as a security, a move that would have significant implications for Ethereum, ETH ETFs, and cryptocurrencies as a whole. According to Fortune, the financial regulator has issued investigative subpoenas to U.S. companies in the past few weeks.

If there is a suitable explanation that allows Ethereum to be defined as a “security,” then Ethereum’s current level of disclosure and materials will definitely not pass. But Gary himself has said in disguise that Ethereum is a commodity, not a security, and the Ethereum futures ETF has already passed.

In addition, if Ethereum is defined as a "security" and the supplementary materials are passed, it will have a demonstration effect on other cryptocurrencies that have been defined as "securities", so if it is not passed on May 24, it is not entirely a bad thing.

In the lawsuit against Coinbase, the SEC identified SOL, ADA, MATIC, FIL, SAND, AXS, CHZ, FLOW, ICP, NEAR, VGX, DASH and NEXO tokens as securities.

In the lawsuit against Binance, the SEC listed SOL, ADA, MATIC, FIL, ATOM, SAND, MANA, ALGO, AXS and COTI as securities.

The fact that cryptocurrencies are defined as securities and commodities means that they will be subject to different regulatory frameworks and laws, depending on which one they are classified as. It is important to understand this because it will affect the way cryptocurrency businesses and investors operate, their profit models, and their compliance requirements.

Cryptocurrency as a Security: When a cryptocurrency is defined as a security, it is usually based on the so-called "Howey Test," a standard established by the U.S. Supreme Court for determining whether an investment is a security. If a cryptocurrency project involves investors' funds being invested in a common enterprise with the expectation of gaining benefits through the efforts of others, then the cryptocurrency may be considered a security. As a result, it will be strictly regulated by the U.S. Securities and Exchange Commission (SEC) and other relevant financial regulators and must comply with a range of legal requirements including registration requirements, disclosure requirements, and other investor protection regulations.

Cryptocurrency as a Commodity: On the other hand, if cryptocurrencies are viewed more as commodities, such as Bitcoin and Ethereum, which are widely considered to be decentralized and not controlled by any specific entity, they are more likely to be considered a commodity. A commodity is generally defined as an underlying physical resource that can be traded, invested in, or consumed. In the US, this means they are regulated by the Commodity Futures Trading Commission (CFTC). This involves different rules and regulatory approaches that focus on market integrity, prevention of manipulation and fraud, etc., rather than the registration and disclosure requirements of securities.

Summary: Cryptocurrencies are classified as securities or commodities, which means they will face different regulatory structures and compliance requirements. This classification affects how cryptocurrencies can be sold, traded and held, and how related businesses can operate. It is extremely important for investors and entrepreneurs to understand how cryptocurrencies are regulated and what this means for their obligations and responsibilities.

Ethereum spot ETF is not as hotly discussed and frequently communicated as the months before the Bitcoin spot ETF was approved

The main basis for James Seyffart of Bloomberg (one of the big names who predicted the approval of the Bitcoin spot ETF) is that the SEC has not had as much communication with those Ethereum spot ETF applicants as it did in the months before the Bitcoin spot ETF was approved.

It is not a professional analysis.

Personal speculation:

Is there a possibility that most of the problems have been solved in the months of frequent discussions on BTC spot ETF, resulting in Issuers having highly repeated materials when applying for Ethereum spot ETF, so there is no need for too much discussion

The SEC did not find strong evidence to refute it, just like it could not refute the approval of BTC spot ETF

Bitcoin's economic model of halving rewards after reaching a certain number of blocks is an absolute deflationary model, but Ethereum is not.

As for the issue of Ethereum's centralization, the only thing mentioned in the application materials for Ethereum futures ETF is the price fluctuations caused by Ethereum's hard fork and the fluctuations of various financial products. In fact, I think this is a manifestation of incomplete and incomplete research on Ethereum. The degree of decentralization has a great weight on whether the product can be manipulated by the market.

Reference: Valkyrie ETF Trust II

The deflation in Ethereum's economic model is that a portion of the transaction fee will be destroyed every time a transaction occurs, resulting in a decrease in supply. If the transaction volume on the Ethereum network continues to increase, and the growth rate of transaction fees exceeds the destruction rate, then the total supply of Ethereum may begin to increase, that is, deflation will no longer occur. This may happen when network activity increases, transaction fees rise, or other factors cause the destruction rate to be insufficient to offset the new supply.

For example, the period from August 2023 to November 2023 in the figure.

Image source: https://ultrasound.money/

If you dig deeper, the change from Ethereum PoW to PoS is not controllable by the SEC, but decided by the Ethereum Foundation headed by Vitalik Buterin. One of the extreme things about Bitcoin is the complete delegation of power by the founding team. Until now, no one knows who Satoshi Nakamoto is.

This means that Ethereum can actually manipulate the progress of inflation/deflation through some methods, such as:

EIP-1559 changes: EIP-1559 is a proposal on the Ethereum network that introduces the concept of a base fee and uses it to destroy ETH. If the implementation of EIP-1559 is adjusted in the future, such as reducing the destruction ratio or completely canceling the destruction mechanism, the supply of Ethereum will no longer decrease.

Changes in the issuance mechanism: The issuance of Ethereum is controlled by a variety of factors, including mining rewards, staking rewards, etc. If the issuance mechanism of Ethereum changes in the future, such as increasing mining rewards or adjusting staking rewards, the supply of new ETH will increase, which may also stop Ethereum's deflationary trend.

Technology or protocol updates: The Ethereum community may update the protocol through hard forks or soft forks, and these updates may affect the supply and destruction mechanism of ETH. For example, if new technologies emerge that can reduce transaction costs or change the way transaction fees are distributed, it may affect the supply of ETH.

Jokingly speaking, is LTC easier to pass? In a sense, it is true.

Both PoS and PoW have the risk of being manipulated by the market, and there is no better or worse (besides, the less environmentally friendly PoW has been passed)

Proof of Stake (PoS) and Proof of Work (PoW) are two different consensus mechanisms, and they have their own characteristics in resisting market manipulation.

In a PoS system, validators must lock up a certain amount of tokens as collateral in order to participate in the generation and verification of blocks. If validators attempt to cheat or engage in malicious behavior, their collateralized tokens may be confiscated, which is called "slashing". This mechanism can theoretically improve the integrity of validators because they have a greater economic incentive to maintain the security and stability of the network. Therefore, compared to PoW, PoS may be more difficult to suffer from a single entity controlling the network through computing power in some cases.

However, PoS systems also face their own manipulation risks. For example, if a validator or a few validators have a large number of collateralized tokens, they may gain disproportionate control over the network, which is called "staking centralization". This centralization may lead to excessive concentration of power, thereby increasing the risk of manipulation. In addition, since validators in a PoS system are usually rewarded with transaction fees and/or newly minted tokens, this may attract wealthy individuals or entities to participate, further exacerbating the centralization problem.

In the PoW system, miners compete to generate new blocks by solving complex mathematical puzzles, a process that consumes a lot of computing resources and energy. In theory, the PoW system resists manipulation through decentralized computing power distribution, because any attempt to control most of the network computing power will be very expensive and difficult to achieve. However, if a miner group (mining pool) controls more than 50% of the network computing power, they have the ability to conduct a double-spending attack, that is, confirming two different transaction branches at the same time, thereby undermining the security and integrity of the network.

In general, both PoS and PoW have their own advantages and disadvantages, and both have potential risks of market manipulation. The choice of which consensus mechanism depends more on the preferences of the community, the specific needs of the project, and the trade-off between security and decentralization.

Of course, except for Ethereum, any project except Bitcoin basically has insufficient degree of decentralization. Many people think that SOL will be the next after the Ethereum spot ETF is passed, but no one has mentioned that Solana nodes are all enterprise-level nodes, and the possibility of doing evil is far greater than Ethereum. This does not take into account that the possibility of doing evil in Ethereum is already far greater than that of Bitcoin.

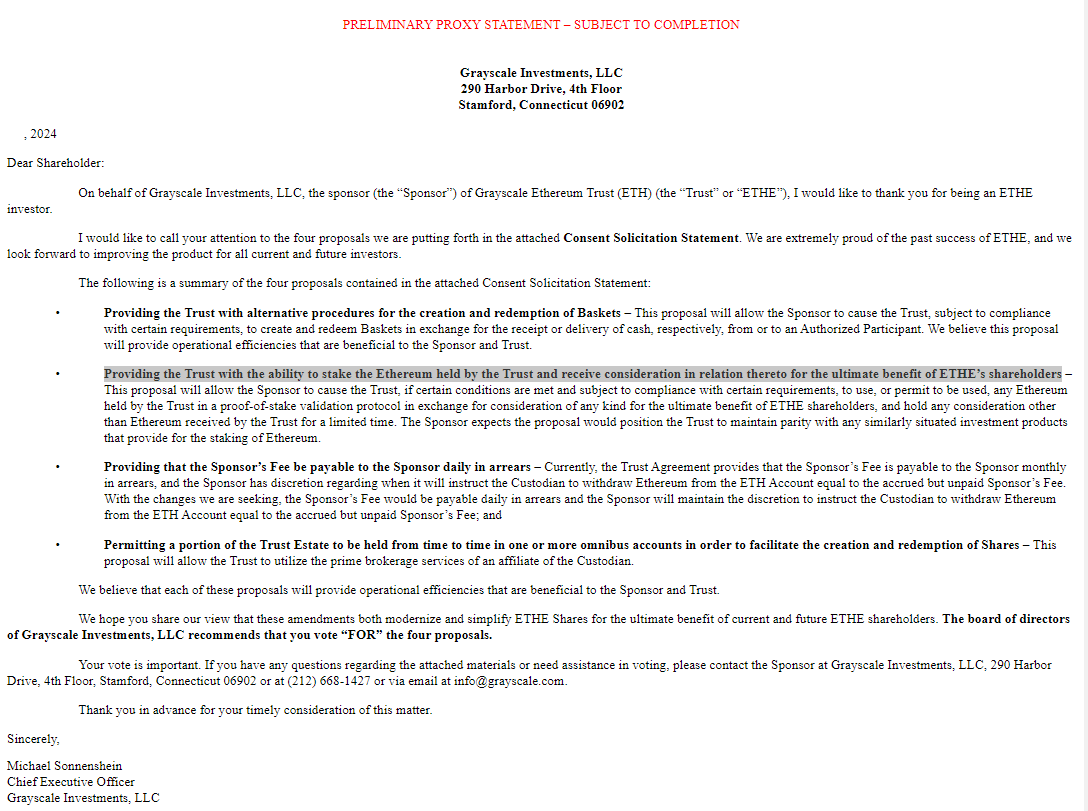

Grayscale's requirements:

Allow ETHE redemption (in other words, spot ETF)

Allow Ethereum in the trust to be pledged (this is more radical)

14A refers to Form 14A of the U.S. Securities and Exchange Commission (SEC), which is a specific form of document, commonly known as a proxy statement. When a company is preparing to hold a shareholders' meeting or is involved in any matter that requires a shareholder vote, it must submit this document to the SEC and send it to its shareholders. The proxy statement provides detailed information about upcoming meetings and voting matters, including but not limited to:

Upcoming board of directors

Compensation information for executive officers

Major decision proposals, such as mergers, acquisitions, and changes to the company's articles of incorporation

Voting guidelines recommended by the board of directors

Corporate governance related information

Potential conflicts of interest or other important information about the company's management The purpose of the proxy statement is to ensure that shareholders have sufficient information when making voting decisions. It is a mechanism under the U.S. securities law framework to protect the rights of investors and ensure transparency in corporate governance. This transparency required by the SEC helps shareholders make informed decisions about the company

Grayscale's latest 14A, GRAYSCALE ETHEREUM ETF enables the trust to pledge the Ethereum held by the trust and receive consideration associated therewith to achieve the ultimate benefit of ETHE shareholders.

Link: https://www.sec.gov/Archives/edgar/data/1725210/000095017024033515/ethe_pre_14a.htm

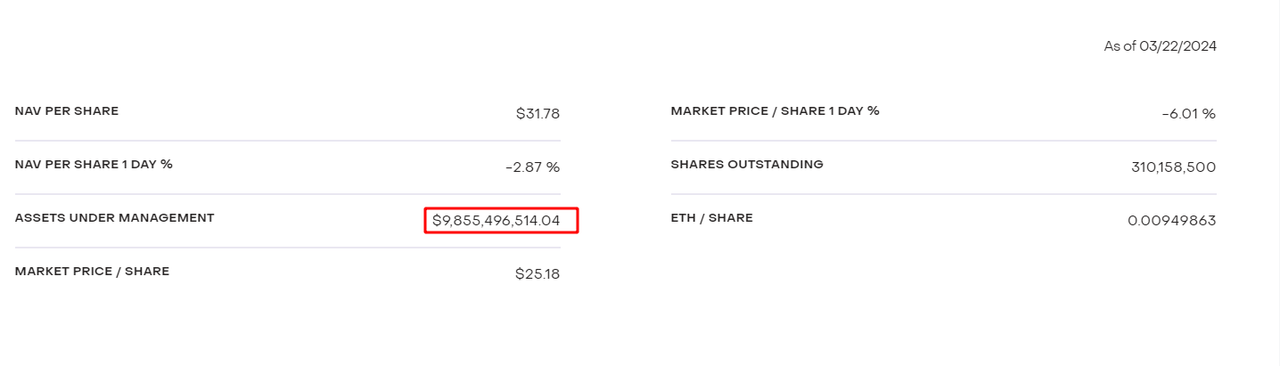

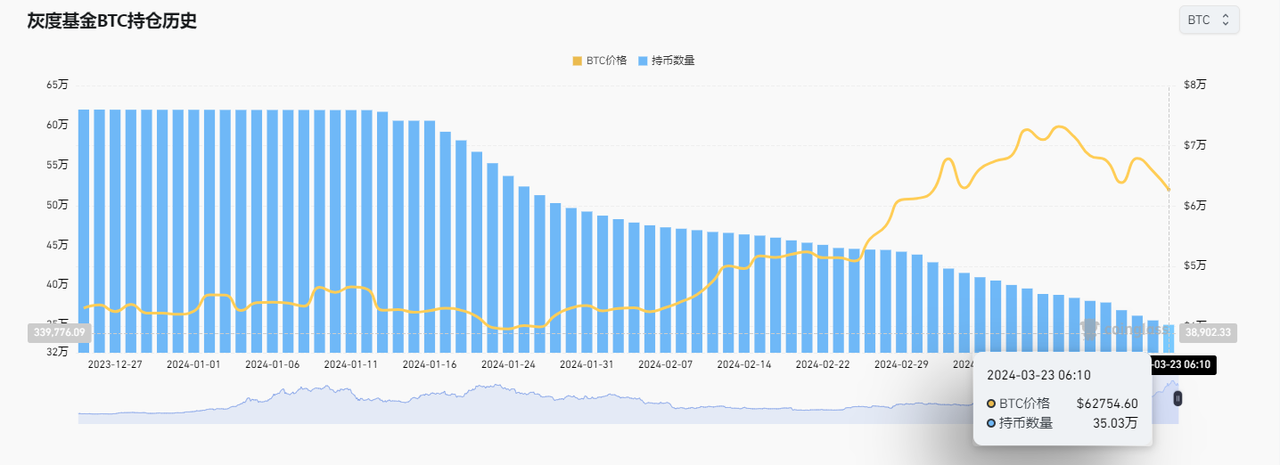

ETHE is worth less than $10 billion (compared with Grayscale's peak market value of Bitcoin: 600,000*70,000=420 billion U.S. dollars, current market value: 350,000*70,000=245 billion U.S. dollars). It can be seen that the approval of the ETF spot may not have such a severe impact on the market.

Grayscale's Bitcoin holdings have dropped from 600,000 at the beginning to 350,000.

Data source: https://www.coinglass.com/zh/Grayscale

For many large groups of non-crypto native capital, Ethereum has much lower buy-in as a key portfolio allocation.

JinseFinanceIf an ETH ETF gets the green light, changes in the regulatory and political landscape could increase the chances of approval for the Solana ETF.

JinseFinanceGolden Weekly is a weekly blockchain industry summary column launched by Golden Finance. The content covers key news of the week, mining information, project trends, technology progress and other industry trends.

JinseFinanceThere are two major narratives in the crypto market. First up, Bitcoin. Followed by Ethereum, and Ethereum may explode in 2024.

JinseFinanceRecommended reading for tonight: 1. Learn more about the upcoming Jupiter airdrop on Solana; 2. Meson tokens will be sold in the Coinlist community. One article to understand the Meson network; 3. One article to understand the RaaS platform AltLayer and its cooperative ecological projects;

JinseFinanceAfter many reversals and mistakes, the Bitcoin Spot ETF was finally approved by the U.S. Securities and Exchange Commission.

JinseFinanceExplore the Future of Finance with Blockchain ETFs and Bitcoin. Diversify, Navigate, and Embrace Innovation in the Evolving Landscape of Investment Opportunities.

Xu Lin

Xu LinIt is an unpopular opinion to think that Grayscale's spot-based Bitcoin ETF could get approved, but the company is confidently ...

Bitcoinist

BitcoinistTwo ETF issuers filed two new and innovative applications for an inverse fund and a leveraged fund.

Cointelegraph

CointelegraphU.S. Securities and Exchange Commission has approved another Bitcoin futures ETF. Could this mean a spot ETF is on its way?

Cointelegraph