OpenAI's New Leadership. Who's In, Who's Out?

CEO Sam Altman remains at the helm, with immediate priorities revolving around advancing research, bolstering safety measures, and refining customer-centric products.

Brian

Brian

In 2024, the Web3 game industry will present a complex situation, making significant progress while also facing many challenges. Although the number of daily active users has surged by more than 300%, and traditional game companies have begun to make specific arrangements in this field, judging from market performance, the market value of this sector only increased by 60.5%, significantly lagging behind the Meme currency and AI sectors. As Bitcoin hits new all-time highs and various crypto sectors thrive, a key question emerges: "Have Web3 games missed the best opportunity to develop in this bull market?"

Behind these superficial figures, however, 2024 marks an important period of transformation for the industry. The industry has moved from a purely speculative stage to maturity. This report will analyze how Web3 games will evolve through the 2024 market cycle, exploring the sector’s key metrics, technological advancements, and strategic shifts. From infrastructure development to user engagement models, we'll explore how the industry can build sustainable growth while addressing mainstream adoption challenges.

Note: Unless otherwise stated, all data in this report are as of December 15, 2024. Data sources are Footprint Analytics and CoinMarketCap.

Market value: reached US$31.8 billion, an increase of 60.5%;

Volume: $5.2 billion, up 18.5%

Number of transactions: 5.3 billion, down 30.3%

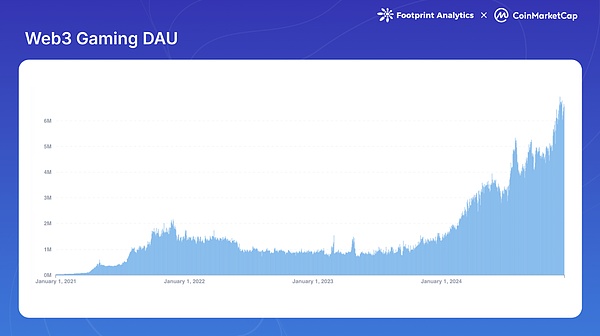

Daily active users: 6.6 million at the end of the year, an increase of 308.6% compared to the beginning of the year;

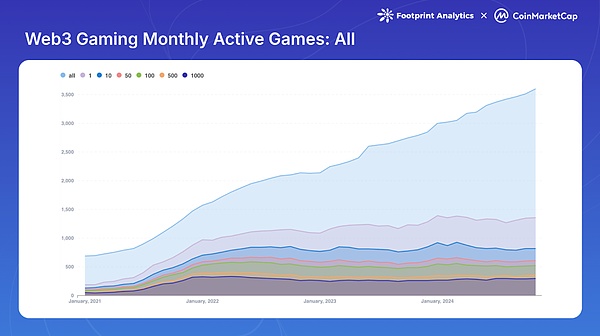

Active games: 1,361 of 3,602 games remain active (37.8%);

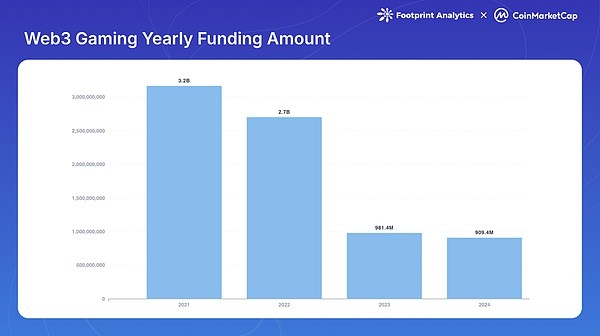

Annual financing: 220 financing events, totaling US$910 million;

Leading public chain:

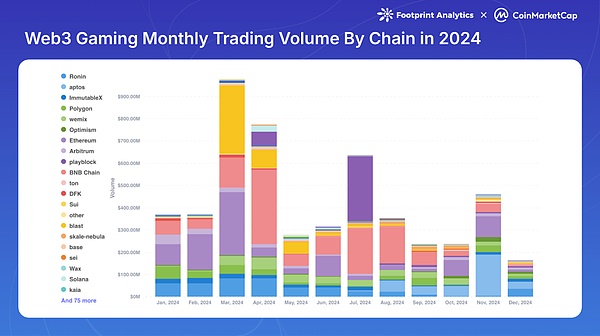

Transaction volume proportion: BNB chain (23.1%), Ethereum (17.6%), Blast (9.2%);

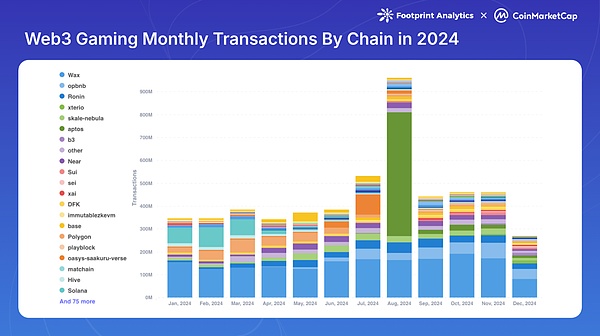

Proportion of transactions: WAX (33.6%), Aptos (11.6%), Ronin (6.1%);

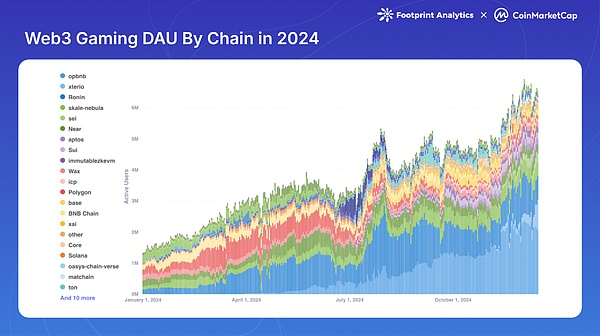

< /li>Daily active users: opBNB (2.2 million), Ronin (1.1 million), Nebula (458,000) (December daily average).

The Web3 gaming sector will achieve strong growth in 2024, but its performance is inferior to other crypto sectors. According to Footprint Analytics, the market value of game tokens reached US$31.8 billion at the end of the year, an increase of 60.5% from the previous year. While the sector hit a yearly high of $47.4 billion in March, it's still significantly below the all-time high of $114.1 billion set in November 2021.

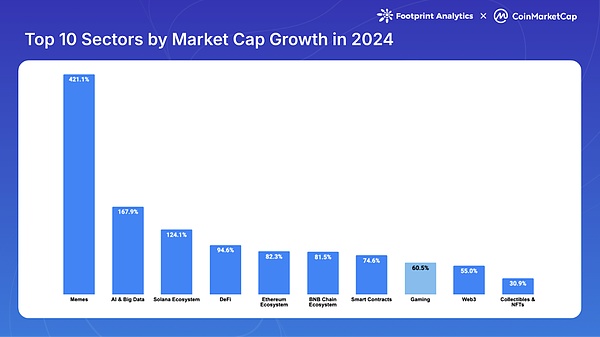

While the overall crypto market performed strongly in the second half of 2024, especially the last two months of the year driven by Bitcoin, gaming token performance lagged other sectors. CoinMarketCap data shows that Web3 games rank eighth among the top ten sectors in terms of market capitalization growth, significantly lagging behind the leading sectors: Meme Coin (421.1%), AI and Big Data (168.0%), and Solana Ecosystem (124.1%).

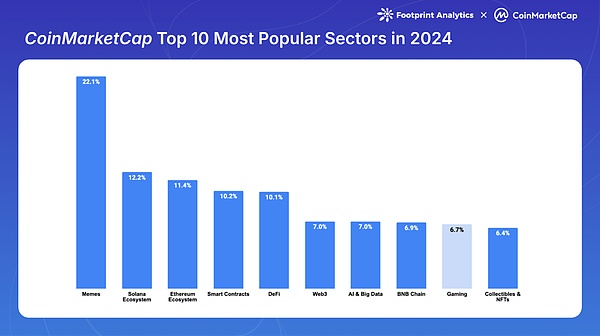

This poor performance also extends to community attention. Among the most watched sectors on CoinMarketCap, Web3 games accounted for only 6.7% of the views in the top ten sectors, ranking ninth, as the focus throughout the year was mainly on Meme coin-related projects.

The performance of key indicators of the Web3 game sector in 2024 is uneven, and transaction volume realization growth, but the number of transactions continues to decline.

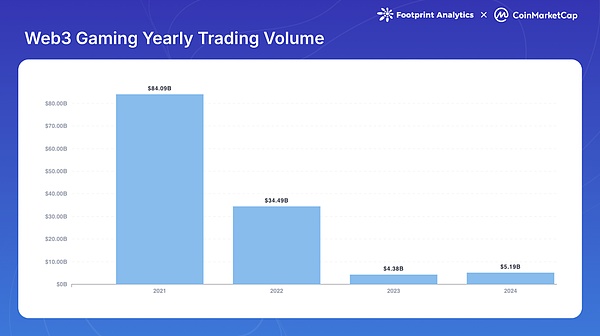

The total transaction volume of Web3 games in 2024 will reach US$5.2 billion, an increase of 18.5% compared with 2023. While reversing the downward trend from 2021, trading volumes remain significantly below previous cycle highs. The 2024 figure is only 6.2% of the 2021 peak ($84.1 billion) and 15.1% of the 2022 volume ($34.5 billion).

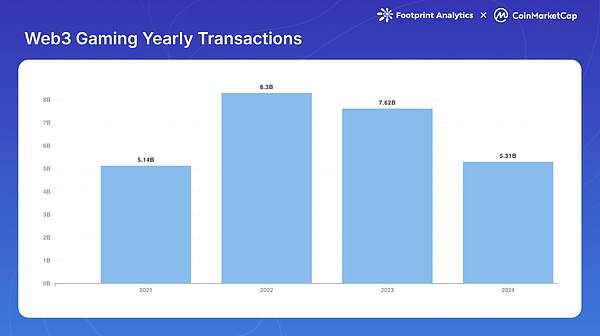

The total number of transactions in 2024 will reach 5.3 billion pens, down 30.3% from the previous year. This level, while comparable to 2021's 5.1 billion transactions, failed to reverse the downward trend that began in 2022.

Daily active users (DAU) in 2024 Significant growth was achieved in the year, from an average of 1.6 million per day in January to 6.6 million in December, an increase of 308.6% during the year. This growth surpasses the previous cycle peak of 1.8 million DAU created in November 2021. While this data may include some bot activity, this increase still demonstrates significant user engagement in this industry.

2024 The dominance of different public chains in Web3 games has changed significantly, with each chain showing different advantages in terms of transaction volume, number of transactions and user participation.

BNB Chain maintained its dominance in terms of transaction volume, achieving $1.2 billion in transaction volume (23.1% market share), followed by Ethereum with $920 million (17.6%). Blast and Ronin hold 9.2% and 9.0% of the market respectively.

Although the overall number of transactions in the industry dropped by 30.3 %, but some public chains showed strong performance. WAX leads the way with 1.8 billion transactions (33.6% of the total). Aptos rose to prominence with its "tap-to-earn" Telegram game Tapos, reaching 620 million transactions (11.6%), including 540 million transactions in August alone. Ronin and opBNB maintain transaction counts of 321 million and 318 million respectively.

User activity of each chain shows significant growth, especially in the second half of 2024. opBNB has exploded in terms of user engagement, reaching 2.2 million average daily active users in December, surpassing long-time leader Ronin (1.1 million). Nebula, a SKALE Layer 2 player, ranks third with 458,000 average DAU. Public chains such as NEAR, Sui, and Sei are among the top ten by DAU, demonstrating the expansion of the competitive landscape of the ecosystem and the willingness of users to try new platforms.

The diversified trend in the use of various chains shows that the ecosystem is becoming increasingly mature, and different public chains are finding their own positioning for various game experiences and user preferences. Major networks have moved beyond simply providing basic blockchain facilities and have evolved into comprehensive platforms for game developers. The Arbitrum Foundation’s 2 billion ARB game catalyst program, the Starknet Foundation’s 50 million STRK token distribution program, and important Grant programs from Sui and Xai all demonstrate how each chain can attract and retain high-quality games through strategic incentives project.

Blockchain processing capabilities have been significantly improved. Currently, the network’s per second Transaction processing volume has increased by more than 50 times compared with four years ago. This growth has been driven by the rise of Ethereum Layer 2 and Layer 3 networks, including Immutable zkEVM, gaming chains based on Avalanche L1, Oasys, SKALE, Arbitrum Orbit, and other high-throughput blockchains such as Solana, Sui, and Aptos.

Game-specific chains have also made significant progress. Ronin announced its Layer 2 initiative, Ronin zkEVM, in June 2024, enabling Ronin developers to create their own zkEVM Layer 2. Immutable zkEVM takes a strategic step towards greater accessibility by removing deployment whitelisting and enabling permissionless deployment. In addition, Avalanche completed its most important “Avalanche9000” upgrade since the mainnet launch in 2020, focusing on solving obstacles for customized L1 builds and improving interoperability.

Ethereum's "Cancun" upgrade in March 2024 (also known as "Proto-Danksharding" or "EIP-4844") was a major milestone that significantly reduced the fees on the L2 network. The impact has been dramatic, with gas fees dropping from a few dollars to a few cents or even less, eliminating one of the biggest friction points facing blockchain game developers and players.

Chainlink Cross-Chain Interoperability Protocol (CCIP) has gained significant momentum in 2024, enabling developers to create games that interact with multi-chain assets. This improvement significantly improves the interoperability of in-game items.

The adoption of standardized formats for digital assets, specifically ERC-721 and ERC-1155, has become more widespread. These standards ensure that in-game NFTs can be recognized and used across a variety of games and platforms, simplifying asset transfer and interaction.

2024 will also see the significant rise of decentralized platforms that support cross-chain gaming. Platforms such as Portal, Fractal ID and Web3Games provide the necessary infrastructure for seamless asset transfer and interaction between different blockchain ecosystems.

2024 is an important year for the development of Web3 games. In addition to the entry of traditional gaming companies, the ecosystem has also witnessed several major game launches. Highly anticipated games like Off The Grid and MapleStory Universe enter early access, while Illuvium is finally officially live. Pirate Nation successfully completed its Token Generation Event (TGE) and launched its successful “play-to-airdrop” campaign.

As of November 30, 2024, the total number of blockchain games reached 3,602, an increase from 2,997 in January. However, the active games indicator shows some challenging trends. Of the total number of games, only 1,361 (37.8%) remain active on the chain, that is, 2,241 (62.2%) are inactive. Additionally, while the total number of games grew, the number of active games fell from 1,387 in January.

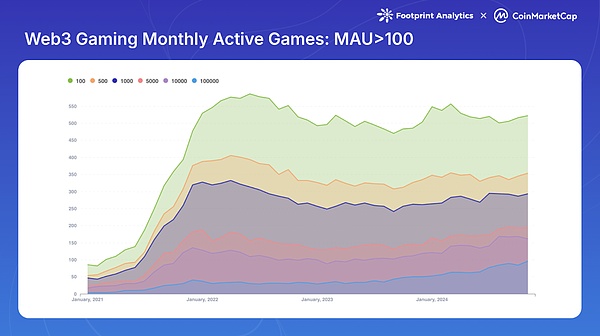

Deep analysis of user engagement metrics shows further market concentration. The number of games with more than 100 monthly active users (MAU) fell from 586 in June 2022 to 522 at the end of 2024. In November 2024, 161 games (4.5% of the total) achieved more than 10,000 MAU, and 96 games (2.7% of the total) exceeded 100,000 MAU.

This user concentration trend indicates that the market is maturing and successful games are attracting larger audiences. This phenomenon is affected by multiple factors, including fierce competition, rapid iteration strategies, and the "head effect" formed by top games in the ecosystem.

Mobile games emphasize accessibility and seamless user experience, establishing themselves as Web3 games in 2024 status of major platforms. A mobile-first approach has influenced the way developers design blockchain games, focusing on intuitive interfaces and streamlined onboarding processes. Mobile games will account for 29.4% of newly released Web3 games in 2024.

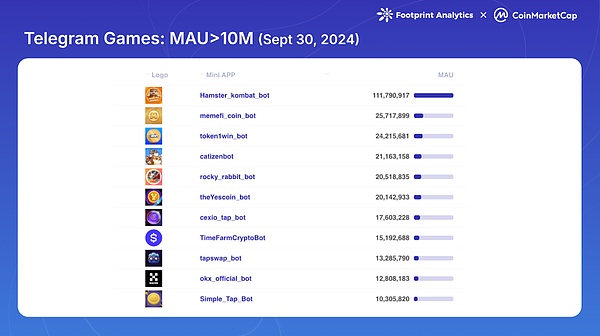

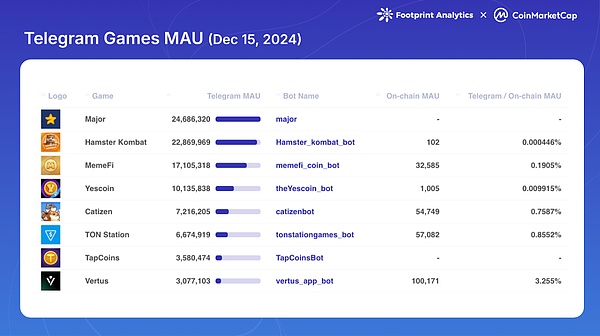

Social platforms, especially Telegram, have become powerful catalysts for Web3 game adoption, accounting for 20.9% of newly released Web3 games. Telegram's success stems from its large user base, streamlined in-app experience, and ability to bypass traditional app store restrictions. The platform’s reach peaked in the third quarter of 2024, with 11 games surpassing 10 million MAUs. It is worth noting that TON has successfully transformed this huge user base into on-chain participants, producing spillover effects in Web3 games, Meme coins and DeFi sectors. This success has prompted multiple blockchain networks outside of TON to compete for Telegram traffic. Aptos, Sui, Core, etc. have launched or supported games based on Telegram.

Similarly, Line announced plans to launch 20 mini-dApps in December 2024, marking the growing interest of mainstream messaging platforms in integrating blockchain games.

The console gaming space remains relatively untapped in terms of Web3 gaming, with major manufacturers Microsoft and Sony maintaining a cautious stance. However, new approaches are beginning to emerge to bridge this gap. Some developers, like Gunzilla Games' Off The Grid, choose to separate core gameplay from blockchain functionality to match the expectations of traditional console games. At the same time, blockchain platforms have begun to develop their own Web3 game consoles, such as Sui's SuiPlay0X1 and Solana's Play Solana Gen1 (PSG1), potentially creating a new category of dedicated Web3 game devices.

2024 marks a major shift in traditional game companies’ attitudes toward blockchain games, with major game studios shifting from experimental moves to strategic developments.

Ubisoft will release Champions Tactics: Grimoria Chronicles on the Oasys Layer 2 HOME Verse in October. This tactical RPG implements a range of NFT-based features while maintaining traditional game elements.

Square Enix strengthens the development of its blockchain sector through strategic investments and partnerships. In addition to investing in gaming platforms Elixir Games and HyperPlay, the company also announced it is bringing its Symbiogenesis game to HyperPlay.

Sony Group's participation marks a major push into blockchain gaming, both through investment and infrastructure development. In conjunction with backing double jump.tokyo Inc.'s $10 million Series D funding round, Sony also announced the launch of Soneium, a Layer 2 network designed to connect Web3 innovation to consumer applications in gaming and entertainment.

As artificial intelligence revolutionizes various industries in 2024, the Web3 gaming field has become an important beneficiary of AI innovation, opening up new opportunities for game development and player experience.

AI has revolutionized in-game interaction and content generation. Game studios are using AI to create more complex non-player characters (NPCs) that adapt to player behavior and generate personalized missions based on individual gaming history and preferences. This personalization enhances player engagement by making the gaming experience more relevant and personal.

When it comes to development, AI significantly simplifies the creative process. Developers are using AI tools to automatically generate game environments and assets, significantly reducing production time and costs. This gives small teams a chance to create high-quality games that can compete with larger studios.

AI also enhances the operational aspects of Web3 games. The technology is used to automate the game testing process and monitor on-chain transactions to prevent potential fraud or cheating, which is especially important in games with complex economic systems. Additionally, AI algorithms are helping to optimize game economies and token models, solving one of the major challenges in Web3 game design.

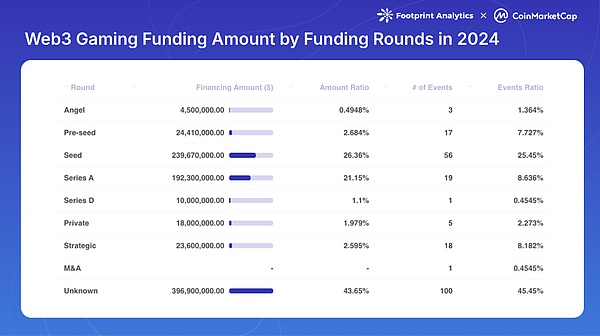

Web3 games raised $910 million in 2024 through 220 funding events. Although the amount of financing is down 7.3% from 2023 and significantly lower than the 2021-2022 boom period (USD 3.2 billion and USD 2.7 billion respectively), the number of financing events increased by 48.7% from 2023, indicating continued investor interest. Although the size of a single transaction is reduced.

This year shows a clear trend towards early-stage investment, with 76 early-stage deals (accounting for 34.6% of total events) compared with only 20 rounds of Series A or later financing (accounting for 9.1%). This trend suggests that while new projects continue to attract initial funding, many projects in the 2021-2022 boom are facing challenges in securing follow-on financing.

Among investors, Animoca Brands maintained its leading position, completing 38 investments, a 192.3% increase from 2023, and participating in 17.3% of all financing events in 2024. Spartan Group and Big Brain Holdings followed with 22 and 15 investments respectively, and the top ten investors completed a total of 152 investments.

Seven projects raised more than $20 million in single events in 2024. Azra Games led the way with $42.7 million in Series A funding and is focused on bringing console-level gaming experiences to mobile platforms.

From the perspective of cumulative financing, Monkey Tilt raised US$51 million through two rounds of financing. They are a "game-entertainment-gambling" hybrid model platform. Gunzilla Games has demonstrated strong investor confidence with four rounds of funding from high-profile investors including VanEck, Coinbase Ventures, Delphi Ventures, and Avalanche's Blizzard Fund.

As the industry matures from the heady period of 2021-2022, the focus has shifted to fewer but higher quality projects, and investors have become more selective in their approach.

Financing is increasingly targeting game infrastructure and development tools, not just the games themselves. Notable examples include NPC Labs’ $18 million seed round for building Web3 games on Base, and Alliance Games’ $5 million Series A for AI-driven decentralized infrastructure. The trend reflects growing investor interest in underlying technology capable of supporting multiple games and platforms.

Platform and multi-chain development have attracted a lot of attention, especially projects to build a cross-chain gaming ecosystem. Seeds Labs raises $12 million for Bladerite, its flagship product on Solana, while B3 launches Open Gaming Layer, demonstrating investor interest in expanding cross-chain gaming capabilities.

In addition, new game categories will gain significant investor attention in 2024, especially Telegram-based games and gambling game projects, although Facing regulatory challenges.

Web3 The gaming industry has experienced significant evolution in gaming models in 2024. The "play-to-earn" model that dominated the previous cycle gave way to a more sustainable approach. Telegram-based "tap-to-earn" games demonstrate unprecedented user acquisition capabilities, while Pirate Nation and Pixels' "play-to-airdrop" strategies provide new user acquisition methods. At the same time, mature projects are turning to a "play-and-earn" model that puts gameplay over financial incentives.

However, the field still faces ongoing challenges. Technical barriers remain significant, especially in achieving seamless blockchain integration without compromising the gaming experience. Regulatory uncertainty, particularly around gambling features and token classification, continues to impact development decisions.

The most critical thing is that maintaining on-chain participation has become a fundamental issue. This is particularly evident in the performance of Telegram games: Hamster Kombat’s monthly active users dropped from more than 100 million in September to 22.9 million in mid-December, with only 0.0004% of users participating in on-chain gaming activities. While other Telegram games show higher conversion rates, most are still below 1%. It’s worth noting that these metrics specifically reflect on-chain gaming activity, as the core gameplay of most Telegram games remains off-chain and users may be more active in other sectors such as Meme coins or DeFi. This highlights the ongoing challenge of converting platform users into active blockchain gamers.

As Web3 games seek to re-establish their place in the crypto landscape status, several key trends emerge as potential catalysts for transformation:

Social platform integration stands as the most promising path to mainstream relevance on the road. The astonishing success of the Telegram game demonstrates the power of meeting users where they are, and platforms like Line and TikTok are poised to take off. This approach may ultimately solve the user acquisition challenges in this space, by leveraging existing social networks rather than building communities from scratch.

AI integration will evolve from a marketing feature to a fundamental driver of innovation. In addition to enhancing game development and NPC interaction, AI may solve the field's core challenges in economic design and user retention. These are areas where Web3 games have traditionally struggled to compete with traditional gaming experiences.

Achieving sustainable growth through consolidation may ultimately determine the field's relevance. Success may not come from competing with traditional gaming or other crypto sectors, but integrating seamlessly with them. This means focusing on how blockchain can enhance rather than define gaming experiences, developing more complex token economics, and prioritizing user experience over crypto-native features.

To sum up, the role of Web3 games in the crypto ecosystem may not be about dominance, but about integration. By cleverly connecting traditional games, social platforms and blockchain technology, Web3 games are expected to create truly innovative value. This evolution will not only help the industry break through the current limitations of "another crypto vertical", but may also become a key force in reshaping the future of the gaming industry.

This report is an annual report jointly produced by Footprint Analytics and CoinMarketCap Research.

CEO Sam Altman remains at the helm, with immediate priorities revolving around advancing research, bolstering safety measures, and refining customer-centric products.

BrianA clandestine operation in Malaysia exposed a fraudulent investment syndicate that operated under the guise of an independent bungalow, once a foreign consulate, employing armed guards to obfuscate its true intentions. However, despite their efforts to evade detection, law enforcement agencies thwarted their activities, apprehending 28 individuals, comprising both locals and foreigners, aiding in the investigation.

Joy

JoyPizza Hut and Spark Foundry have clinched the esteemed title of Best Brand Experience of the Year at The Drum Awards for Metaverse. This recognition stems from their exceptional collaboration with End of the World Pizza (EOWP), delving into the Metaverse with an innovative approach.

JoyRevised figures for Q3 disclosed the fastest quarterly expansion in almost two years, with consumer spending rising at a healthy 3.6% annual rate, albeit slightly lower than the initial 4% estimate.

BrianAmir Hossein Golshan, a 25-year-old Los Angeles resident, has been sentenced to 96 months in federal prison for orchestrating various scams, including "SIM swapping" to hijack Instagram accounts. Golshan's schemes, resulting in over $1.2 million in losses, involved impersonating individuals, fraudulent advertising, and exploiting two-step authentication vulnerabilities, showcasing the escalating sophistication of digital fraud.

Jixu

JixuLouis Vuitton unveils the VIA Tile Trunk, a €6,000 NFT symbolizing its bold move into Web3, blending high fashion with the digital landscape. This marks the brand's pioneering step into direct digital sales, showcasing a unique fusion of NFTs and physical luxury products, setting the stage for a dynamic future in the digital luxury market.

JixuCristiano Ronaldo faces legal repercussions as a class-action lawsuit accuses him of promoting Binance's unregistered securities through his NFT collections. The lawsuit alleges Ronaldo's endorsements fueled Binance's surge, leading to claims of influencing users' investment decisions, while the broader legal turmoil involving Binance and its founder adds to the scrutiny of celebrities in cryptocurrency promotions.

JixuSão Paulo Football Club pioneers NFT tickets for their upcoming match with Flamengo on December 6th, using the Smart Ticket system from their tech hub. This blockchain-based innovation challenges traditional ticketing, offering fans tiered pricing for tokenized tickets with tangible and digital experiences, aligning with the 'Loyalty 3.0' trend to enhance customer engagement.

JixuAnimoca Brands Japan and Quidd join forces to pioneer the convergence of anime and manga with Web3, offering a unique blend of Japanese intellectual properties and digital collectibles. This collaboration aims to cater to global fandom, providing innovative digital collectibles accessible to enthusiasts worldwide, bridging the cultural richness of Japanese anime and manga with cutting-edge technology.

JixuWormhole, a trailblazing messaging protocol facilitating blockchain cross-communication, has hit a new high in the crypto sphere, amassing $225 million in its latest fundraising.

YouQuan

YouQuan