Author: Lucas Campbell

Source: Bankless

DeFi's experiments with different token designs in the past two years have accumulated a lot of valuable knowledge about token design. This article divides tokens into the following three categories: (valueless) governance tokens, production tokens, and voting escrow tokens. In a bear market, which tokens will survive to the end?

Token economics is an emerging field.

The industry is collectively exploring the best design, distribution, utility, governance framework and everything else. In fact, it's still a blank canvas.

As token teams have experimented over the years, we have seen a few different token models emerge as the standard.

In DeFi Summer, we saw the rise of worthless governance tokens like UNI and COMP.

There are also cash flow tokens like MKR and SNX that have been staples for years.

Recently, we’ve seen voting escrow tokens (veTokens) gain traction among industry-leading projects.

Which is the best?

First, let's start with an overview of the different token models and their designs.

We will then evaluate the price performance index of these tokens to see if there is a consistent winner.

Different Token Models

As mentioned earlier, we see three main types of token models:

1. Governance Tokens

2. Productive tokens (staking/cash flow)

3. Voting Escrow Token (veToken)

governance token

Examples: UNI, COMP, ENS

For a while, governance tokens were the standard in DeFi. Governance tokens, popularized by Compound and Uniswap in 2020, are exactly what their name sounds like — governance rights over the protocol.

The peculiarity of such tokens is that they have no value and no economic rights. One token equals one vote, nothing more.

From this perspective, governance tokens have received a lot of flak from the community.

No cash flow! What is the value of this?

This is a fair criticism. Prominent governance tokens like UNI and COMP do not receive any dividends from the protocol’s business activities (trading on Uniswap and lending on Compound). This is mainly for legal reasons. To a large extent, governance tokens help minimize regulatory risk due to lack of cash flow rights.

Nonetheless, governance tokens can exert influence over the protocol and clearly have some value. It's hard to value, but it exists.

There is also a common assumption that these tokens will eventually vote for the economic rights of the protocol in the future - Uniswap is currently working on this. The protocol is currently discussing whether to turn on the fee switch to collect a portion of profits from liquidity providers.

While profits from the fee switch won’t accrue directly to UNI tokens (it goes to the DAO treasury), it’s an early sign that the theory will work in the long-term. All it takes is a proposal.

While naysayers will argue that governance tokens have no place in investment portfolios, Uniswap’s $9 billion valuation argues otherwise.

And whether it is the best performing token model is another question, which we will answer below.

Staking/Cashflow Tokens

Examples: MKR, SNX, SUSHI

While some protocols have chosen the route of worthless governance tokens, others like MKR, SNX, SUSHI, etc. have decided to grant economic rights to token holders.

These tokens all generate income from the business activities of the protocol. MakerDAO is one of the companies pioneering this work. Protocol revenue (accrued interest) from Dai loans is used to buy back and burn MKR. This provision has been in place for many years. By holding MKR, you indirectly gain cash flow rights through the dwindling supply of MKR in the market.

MKR provides passive holding, while SNX and SUSHI require users to hold tokens in order to obtain dividend rights. Both protocols generate fees from transaction activity and redistribute them to stakeholders on the protocol. For SNX, in addition to the awarded SNX, users can also earn sUSD (Synthetix’s native stablecoin) every week. On the other hand, SUSHI stakers automatically buy SHUSHI in the market through the agreement to earn more income.

Note that for staking/cashflow tokens we should not consider local inflation as part of the income. The most typical example is Aave. It's like a token of a pseudo-productive token. While the protocol allows users to stake AAVE (stkAAVE), staking does not generate any exogenous cash flow from protocol activity - it is just AAVE in the DAO treasury.

Voting Escrow Token (veToken)

Examples: CRV, BAL, YFI

Voting escrow tokens, popularized by Curve Finance, are a hot topic in token economic design right now. With this model, holders have the option to lock their tokens for a predefined period of time (usually ranging from 1 week to 4 years).

By locking their tokens, users receive a veToken based on the length of the stake (e.g. CRV's veCRV). For example, a user who stakes 1000 CRV for 1 year will get 250 veCRV, whereas if they stake the same amount for 4 years, they will get 1000 (250 x 4) veCRV.

The key here is that vetokens usually have a special scope of authority over the protocol. For Curve, veCRV holders have the right to vote on which liquidity pools receive CRV liquidity mining rewards, as well as increasing their rewards for providing liquidity. Additionally, holders of veCRV receive dividends from transaction fees and bribes through the protocol.

Overall, the veToken model takes the two aforementioned token models and adds some additional utility around it, creating a very compelling case.

To know which of these three tokens can survive the bear market, we need to delve into the historical performance of these tokens.

historical performance

We’ll take an evenly weighted index of the three coins in each category and then measure their price performance year-to-date – near the relative top of the cryptocurrency market.

From this, we will be able to gauge which token model is the most price-resilient in a prolonged bear market. Obviously, there's a lot of nuance going on here -- fundamentals, catalysts, narrative, and so on.

- Governance Tokens: UNI, COMP, ENS

- Production Tokens: MKR, SNX, SUSHI

- Voting Escrow Tokens: CRV, BAL, FXS

We know that 2022 is not the best year for cryptocurrencies. Both BTC and ETH are down about 50% compared to the beginning of the year.

So, given that most other coins are riskier and financial markets overall are in a risk-off environment, it shouldn’t be a surprise if they fall by the same amount or even more.

Regardless, it will be interesting to see how these assets perform when categorized by token model.

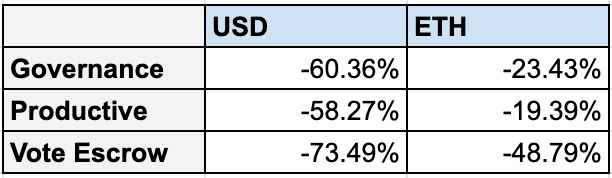

We evenly weighted the 3 tokens in each category to obtain the following data.

While it is intuitive to many that governance tokens should perform the worst since they are widely considered “worthless,” voting escrow tokens are actually the worst performers on average of the three token models. Note that this performance does not include any dividends holders receive from protocol fees, bribes, and any other cash flow positive activity.

Regardless, this is still rather surprising given the positive sentiment among crypto investors towards the token’s model. Voting escrow models are a hot topic in the token economy design world right now. It has a strong lock-up period mechanism, earns cash flow, and has strong governance rights (such as directing liquidity incentives).

Interestingly, it wasn't one of the tokens that beat the other two. All 3 coins performed poorly against USD and ETH. Curve, the pioneer of the voting custody token model, fell 71%. Meanwhile, Frax's FXS is down 84%. Even after applying the voting escrow model in March, BAL dropped 61%.

why?

On the one hand, voting escrow tokens usually have a large token release. For example, Curve currently distributes over 1 million CRV per day to the protocol’s liquidity providers. According to CoinGecko’s Circulating Supply Report, this equates to over 100% inflation over the next year. Similarly, Balancer currently distributes 145,000 Bals per week, with an annualized inflation rate of over 21%.

Frax, on the other hand, only uses about 7% of its token supply to incentivize LPs. While that number isn’t crazy, Frax’s poor performance could largely be attributed to the algorithmic stablecoin’s post-Terra drop, and the resulting failure of 4pool.

Taking a step back, on average, production tokens perform best. This is largely driven by SNX, which is down only 35% since the start of the year. This could be due to the recent successful integration of the protocol’s atomic swaps (i.e. 1inch) on different aggregators, the token rose 135% from the bottom in June.

Outside of SNX, MKR performed in-line with the basket, down 57%, while SUSHI saw the biggest drop of 87% during the governance and operational chaos.

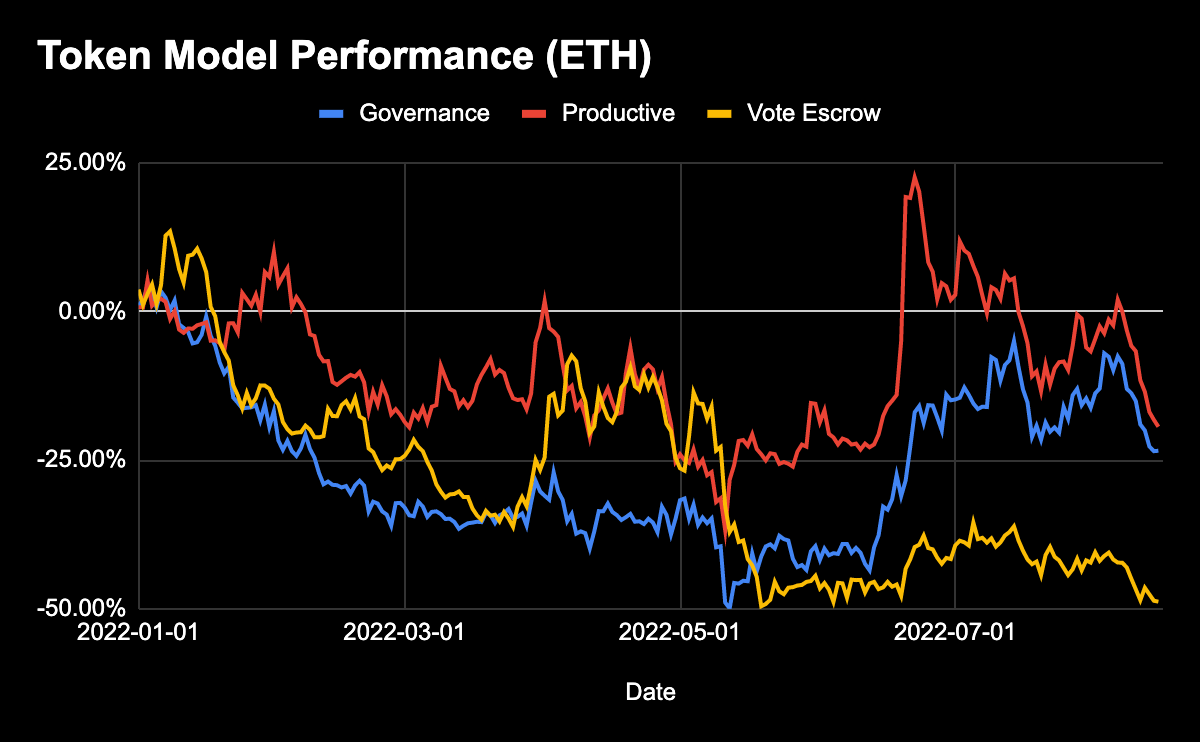

While underperforming in USD terms in a volatile macro environment, when looking at these assets in terms of ETH - as we always want to outperform ETH - it's not that bad.

For a while, around the recent market bottom, the ETH-denominated production token was actually on the rise.

Fundamentals > Cash Flow

Obviously there's a lot of nuance here. The value accretion token model is not the end goal.

Each protocol has its own independent drivers. Ultimately, it’s these catalysts, not the underlying token model, that are driving the macro price up. While locking in floats or dividends that benefit token holders helps, it’s not a panacea.

There is no doubt that cash flow rights have positive benefits for token holders and increase the attractiveness of holding assets, especially when the protocol earns meaningful fees.

But in the final analysis, it is still a question of fundamentals.

These token models - unless severely disrupted - should merely be a push to what is already happening.

Jixu

Jixu