Unpacking bitsCrunch: High Community Activity but Severe Lack of Scale

According to Certik's Skynet Ranking, bitsCrunch ranks 38th in the field of artificial intelligence and 8th among AI projects not yet listed on exchanges.

Snake

Snake

Author: Arthur Hayes

Source: Bitmex Blog

(Any of the opinions below are the personal opinions of the original author and should not be used as the basis for making investment decisions, nor should they be interpreted as suggestions for engaging in investment transactions.)

I am currently reading Alchemy of Finance by George Soros, which inspired me to write this macro paper on ETH mergers. In terms of macro investment, Soros is the greatest man. His followers — such as Paul Tudor Jones and Stan Druckenmiller — were superstars in their own right, but owed much of their success to the strategies and principles Soros articulated over the years. "Financial Alchemy" offers an interesting philosophical discussion of what drives the markets—a must-read if you're interested in techniques for managing your own or other people's money.

At the heart of Soros's theory—which he calls his "Theory of Reflexivity"—is that there is a feedback loop between market participants and market prices. The basic idea is that market participants' perceptions of a particular market situation will influence and shape the development of that situation. Market participants' expectations affect market facts (or so-called "fundamentals"), which in turn shape participants' expectations, and so on. Put more simply, the actors—consciously or not—often play an important role in bringing about the future they predict. Their bias reinforces the tendency for prices to rise or fall as the future becomes a self-fulfilling prophecy.

This explanation is short and incomplete, but I will explain it in more detail later. Now, let's get back to cryptocurrency and how it relates to consolidation.

Merge or don't merge. That's the future event we're trading. The merger itself is not affected by the price of Ethereum, and its success or failure depends entirely on the skills of Ethereum core developers.

Merge will do two things:

1. It will remove the proof-of-work ETH release for each block (that is, the ETH that is paid to miners in exchange for their computing power to maintain the Ethereum network). Currently, about 13,000 ETH are released every day. After the merger, it is expected that the 13,000 ETH that was originally paid to miners per day will be replaced by 1,000 to 2,000 ETH, and will be paid to the validators of the network (that is, those who pledge ETH, who help determine which ETH transactions are valid and which are valid). invalid in exchange for more ETH). These releases will occur at the same rate regardless of the price of ETH and usage of the Ethereum network.

2. Each block will burn a certain amount of Gas fees (this means that the ETH used to pay these fees will be permanently withdrawn from circulation). This variable depends on network usage. Web usage is a reflexive variable, which I will explain in more detail later.

Total ETH Inflation = Block Release – Gas Burned

I make the block release a constant at the current local condition. These local conditions may be disrupted, but only after a long time (ie hundreds of years or so). Therefore, we can treat this variable as a constant.

The gas fee burned depends on the usage of the network.

Inflation = block release > gas fee burned

Deflation = block release

Those who believe that ETH will become a deflationary currency must also believe that network usage (and thus, the fees consumed by ETH paid by users) will be high enough to offset the release of ETH every block as rewards for validators. However, to assess whether they are likely to be correct, we must first ask - what determines the degree of usage of a given cryptographic network like Ethereum?

Users have many options when it comes to choosing a layer 1 smart contract network blockchain. Other layer 1 blockchains include Solana, Cardano, Near, etc. Here are the factors that I think influence users to choose a chain:

Mind share - which chain is better known? Social media and blog posts are the main medium for disseminating information about various layer1 blockchains.

Apps - Which network has the most robust decentralized applications (DApps)? Which of these applications are leading the way? Which of these applications has the greatest trading liquidity? etc.

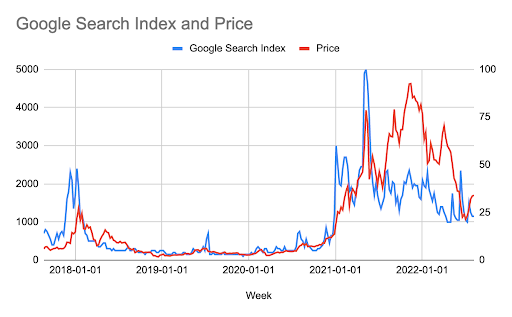

Psych share has a reflexive relationship with ETH price. The graph above shows Google search trends for "Ethereum" and the price of Ethereum. As you can see, they are closely related. If I run a correlation between the two data series, r = 0.77. Conceptually, this makes sense. Interest in the Ethereum network fluctuates with the price of its native token — as the price rises, more and more people hear about Ethereum and want to buy and use the network, further driving the price up.

The quality of applications on the web depends on the quality and quantity of network engineers. As a developer, you create things for people to use. If no one is using the web, you're less likely to use it for development. Obviously, developers want to write code in a language they are familiar with, but this preference is secondary to the number of users that can interact on a given decentralized network.

The number of developers is directly related to the number of users their work can serve. As we established above, the number of users of a given network is directly related to the price of the native token. Because the number of users and price share a reflexive relationship, the number of developers and price must also share a reflexive relationship. As the price rises, more people hear about Ethereum, more people use the network, and more developers are drawn to build applications on the network in order to attract its large and ever-growing Growing user base. The better the application, the more users will join the network. So back and forth, this is reflexivity.

The deflation rate of ETH depends on the gas fee burned.

The amount of Gas fee burned depends on the usage of the network.

Network usage depends on the number of users and the quality of the application.

There is a reflexive relationship between the number of users and the quality of applications and the price of ETH.

Therefore, we can deduce that there is a reflexive relationship between the deflation rate and the ETH price.

With this in mind, we can speculate that there are two potential states for the future.

If the merger is successful, there is a positive reflexive relationship between prices and the amount of monetary deflation. So traders will buy ETH today, knowing that the higher the price, the more the network will be used, the more deflationary it will become, driving the price up, causing more usage, and so on. This is a virtuous cycle for bulls. It will only peak when everyone has an Ethereum wallet address.

If the merger is unsuccessful, there will be a negative reflexive relationship between price and deflationary volume. Or, to put it another way, there would be a positive reflexive relationship between prices and monetary inflation. So, in this case, I think traders are either short or not holding ETH.

There is a bottom line to this relationship, as the ETH network is the longest operating decentralized network. ETH gained massive market cap without consolidation. The most popular dapps are built using Ethereum, which also has the most developers than any other layer 1 blockchain. Given this, I believe that the price of ETH will not fall below the $800-$1000 it experienced during the TerraUSD and Three Arrows Capital crypto credit crash.

We now need to determine the market's perception of the success or failure of the merger.

In my opinion, this can best be determined from the chart below, which shows the ETH/BTC exchange rate. The higher it is, the better ETH will outperform Bitcoin. Since Bitcoin is the reserve asset of the crypto capital market, in my opinion, if ETH outperforms Bitcoin at this stage, it means that the market believes that a successful merger is more and more likely.

Since the unraveling of the crypto credit crisis, ETH has outperformed BTC by about 50%. Therefore, I think it's reasonable to assume that the market is growing more confident about a successful Ethereum merger. The current expected merge date proposed by Ethereum core developers is September 15, 2022.

But this is just the point of view of the spot market. What about the derivatives market?

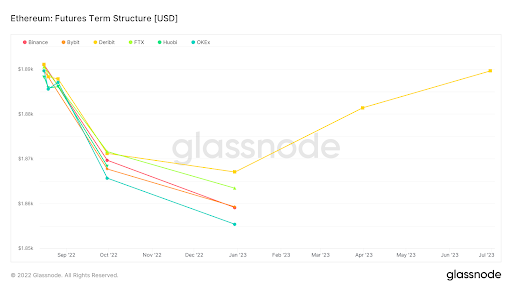

The chart above illustrates the term structure of Ether futures. The futures term structure plots the current price of a futures contract against the time to expiration. Based on this, we can predict the supply and demand of different maturities by calculating the premium or discount of the futures contract relative to the underlying spot price.

backwardation = futures price

Contango > current spot price; contango trading

Considering that the entire curve through June 2023 is trading in backwardation – meaning that the futures market predicts that ETH will be priced below the current spot price by the expiry date – selling pressure outweighs buying on margins pressure.

Here is a chart of ETH futures open interest. Open interest is the total number of open futures contracts held by market participants at a given point in time. As you can see, it is recovering from its lows during the crypto credit crash in mid-June. The curve is in backwardation while the open interest is increasing. In my opinion, this means that the selling pressure is increasing. Conversely, if the curve is in contango (futures price > current spot price), the amount of open interest increases, which would indicate significant and rising buying pressure on the margin.

There are two potential reasons for the current selling pressure:

1. You are long physical ETH, but not sure if or when the consolidation will succeed or when it will happen, so you fully or partially hedge your ETH exposure by selling futures contracts at a price above the current spot price.

2. You want the merge to be successful, and you want to be able to pick up free forked tokens that will be taken away when certain factions of ETH inevitably resist the merge and create a fork to maintain ETH's proof-of-work chain Minted and distributed to all ETH holders. So, you are long physical ETH, but you also want to hedge your ETH exposure by selling futures contracts. If you sell the futures contract at a discount to the value of the forked coin you received, then you can make a profit.

On the other side of these directional futures flows are market makers. Their portfolio is Delta neutral, meaning they do not invest in ETH directly. So when they buy futures from the seller, they have to sell ETH on the spot market to hedge. This adds to selling pressure in spot or cash markets.

But remember - the above shows that ETH has outperformed BTC by 50% recently. Selling by market makers in the spot market is no match for the long-term flow of bulls. This is very encouraging. This means that market confidence in a successful merger is undervalued and overshadowed by short hedging flows from market makers.

If the market thinks the odds of a successful merger are increasing every day, what will happen to those who are hedging through futures contracts if the merger succeeds?

1. If the merger is successful, those holding ETH spot will buy back their hedges so they can benefit from the reflexivity I described above.

2. If the merger is successful and the forked coins are distributed, they will be sold for whatever value and those who hedged their positions will unwind them immediately. Now, they may decide to sell spot ETH to close out their positions completely - but I bet these traders will be in the minority. Their ETH will not close out and benefit from the reflexivity.

I think the success of the merger will create some buying pressure, reversing market makers' futures positions in the process. They will switch from being long/short in futures to being short/long in futures. The spot they are short must cover (meaning buy spot), and if they are net short futures, they must now go into the market and buy additional spot. The unwinding of derivative flows that resulted in backwardation prior to the consolidation will result in contango post-consolidation.

For those who believe the merger will go through as planned, the question becomes: How do you express your bullish view?

The most straightforward transaction is to exchange fiat for ETH, or to add ETH to your crypto portfolio.

Lido Finance

Lido Finance is the largest validator node for the new standard chain of Ethereum. Lido allows users to stake ETH to earn validator rewards. In return, Lido will receive 10% of the ETH rewards they earn. Lido has a DAO that issues LDO tokens.

This is an attractive option if you want to take on more consolidation risk. It is riskier than owning spot ETH because Lido's value proposition is entirely dependent on the success of the merger - whereas with spot ETH it could still be profitable without the merger because it has other value propositions (i.e., it is powered by the second largest public blockchain by market capitalization).

LDO has rallied more than 6x since the crypto credit crash in mid-June thanks to Lido's bold bet on mergers.

Long ETH futures

For those who want to gain more income by increasing leverage trading, long ETH futures is a good choice. Because of the negative basis, those who are long futures are rewarded by holding exposure to ETH.

Basis = futures - spot

Looking at the term structure, futures contracts expiring in December 2023 are the cheapest. If the merger is successful, these prices will oscillate violently into contango when shorts are covered due to the remaining time value. The September 2023 futures contract still has 1-2 weeks of time value after the combination, and you won't get the same basis effect as if you were long December futures.

Long ETH call options

Buying call options is a good strategy for those who like leverage but don't want to worry about being liquidated like with futures contracts. Implied volatility for September and December futures is currently lower than realized volatility. This is to be expected since hedgers use not only futures contracts but also options.

Interestingly, when I entered the market to buy a December 2022 $3000 strike ETH call option, I was able to trade at a much larger quote than what was on the screen. I am told that this is because traders are heavily long calls and hedgers are overwriting calls to hedge their long ETH positions. Traders are more than happy to reduce their long call exposure as this frees up margin and they show very tight prices on the offer side.

Similar to the futures term structure, the implied volatility of December options is lower than that of September options, especially on the wing side. Another reason I prefer the December option is that I don't need to be as precise on the timing of the consolidation. The technical delivery date is known, although the developers tell us that the merged date is September 15th.

Long December Options vs. Short September Options

This is a curve steepening trading strategy. You need to watch your profits very carefully. While you have no exposure to the ETH price, one of your legs will show an unrealized loss, while the other leg will show an unrealized profit. If your exchange does not allow you to hedge these, then you will have to add margin to prevent losses on the trade - otherwise, you will be liquidated.

You are short September futures at a discount, which means you pay theta (or time value). You are long December futures at a discount, which means you receive theta. When you have net theta exposure, you are actually making money every day due to net positive theta (assuming no movement in the spot price). If we believe that there will be intensive short covering after the merger, then December futures will trade higher than September futures. So the curve steepens and you make more money long the December position than short the September position.

Buy on rumor, sell on confirmation?

Assuming you are long via some ETH financial instrument, the question becomes - do you fully unload or close your position before the consolidation happens?

Since reflexivity drives up the price of ETH before the merger, textbook trading suggests that you should at least reduce your holdings before the merger. Reality rarely lives up to expectations, though.

but……

Structural declines in inflation can only occur post-consolidation. I hope we see something similar to the Bitcoin halving - that is, we all know the dates they will happen, but Bitcoin will always bounce back after the halving.

That said, there is a chance that the price of ETH will drop slightly after the merger. Those who cut some or all of their holdings will initially feel good about their decision. However, with the onset of deflation, prices may gradually grind higher due to the reflexive relationship between high and rising ETH prices and network usage. At that point, you have to decide when to add to your holdings. This is often a very challenging trading situation. You believe in the long-term trend but want to trade around your position - now, you have to pay a higher price to re-establish the position. It hurts because you're always waiting for a dip when you know it's time to buy back. But that dip—or at least the magnitude of the dip you were expecting—never happened, and you either never re-entered the same position, or you would have missed out on a significant portion of the gains.

With this thought experiment, and my belief in the reflexive nature of the situation, I wouldn't be underweight entering a merger or immediately after it. If anything, I'd add to my holdings as the market sells off - because I believe the market hasn't (and can't) set a top price right now.

how to sell

We also have to consider the best strategy for shorting a consolidation event. Given the current market sentiment and price action, those who were shorting ETH ahead of the merger are fighting a reflexive trade. This is a very dangerous situation. When you short something, your maximum gain is 100% unleveraged since the price can only go to zero (while the maximum loss when long is unlimited). Therefore, timing is very important.

The best time to go short is before a merger takes place. This is going to be when expectations are highest, you have a very short period of time between entering a deal and when the merger happens or doesn't happen. If the merger fails, the sell-off will happen quickly, given the market's high expectations and objective reality. This way you can get out of the trade quickly and win triumphantly.

I recommend using put options. Referring to the futures curve above, March 2023 futures are the least discounted. This means that, as a short, you pay the least. This also means that the March 2023 put option will be the most attractive. If I were short, I would buy 1000 March 2023 ETH puts on September 14th. You know in advance your maximum loss, which is the premium you put on the put option. This will allow you to eliminate unlimited losses if the merge is successful.

For me, writing these articles has been a great way to help me really think about my trades and ultimately increase my confidence in where my portfolio is positioned.

If I can't rationalize the thinking behind my portfolio, then I need to reexamine my trading decisions. In the course of writing articles in the past, I've made a lot of changes to my portfolio. If I can't defend previous beliefs well in written words, I lose faith in them.

This increased my confidence as I tried to apply Soros' theory of reflexivity to the ETH merger. After sorting out these thoughts, I finally knew what to do.

According to Certik's Skynet Ranking, bitsCrunch ranks 38th in the field of artificial intelligence and 8th among AI projects not yet listed on exchanges.

SnakeAmidst speculation, Cosmos Network's ATOM token eyes potential growth following the proposed merger of two key decentralised exchanges, Osmosis and UX Chain, within its ecosystem.

YouQuan

YouQuanThe OpenAI controversy reflects a battle between corporate profits and altruistic goals in AI, prompting concerns about societal impact and the call for democratic governance.

Hui Xin

Hui XinMistral AI, a French startup, is securing a remarkable $487 million in funding led by Andreessen Horowitz, positioning it as a strong competitor in the AI market against giants like OpenAI.

YouQuanThe Internal Revenue Service's Criminal Investigations Unit is reportedly grappling with a surge in crypto-related tax evasion cases

Aaron

AaronOpenSea, once a dominant player, now holds only 17% of the market share

Alex

AlexDespite this, Bukele has declared that El Salvador has no intention to sell.

AlexThe U.S. Securities and Exchange Commission (SEC) has prolonged the evaluation period for NYSE Arca's proposed rule change, aiming to list Grayscale Ethereum Trust shares as an exchange-traded product.

AaronAmidst a surge in cryptocurrency interest, Phoenix Group's debut on the Abu Dhabi Securities Exchange marks a pivotal moment in the region's financial evolution.

Hui XinThe developments in Belarus echo similar events in Moscow

Alex