Variant: Bitcoin DEX Satflow explained

Satflow is a new DEX for professional traders built on the Bitcoin network.

JinseFinance

JinseFinance

Author: 0xkyle; Compiler: Felix, PANews

So far, the 2024 cycle has witnessed Solana's dominance, and the main narrative of this cycle, Memecoins, are all generated on Solana. In terms of price, Solana is also the best performing L1 blockchain, up about 680% so far this year. Although memecoin and Solana are deeply intertwined, Solana as an ecosystem has generally ignited people's interest since its recovery in 2023. Its ecosystem has flourished, and protocols such as Drift (Perp-DEX), Jito (Liquid stake), and Jupiter (DEX-Aggregator) all have tokens with valuations of billions of dollars. Solana's active addresses and daily transactions exceed all other chains.

Solana's primary DEX Raydium is at the core of this thriving ecosystem. The old saying “selling shovels during the gold rush” perfectly captures Raydium’s position: powering the liquidity and trading that fueled the memecoin craze. Benefiting from the flow of memecoin trading and broader DeFi activity, Raydium has solidified its position as a critical infrastructure in the Solana ecosystem.

This article aims to use a data-driven approach to unpack Raydium’s position in the Solana ecosystem using a first principles approach.

Launched in 2021, Raydium is an automated market maker (AMM) based on Solana that enables permissionless pool creation, lightning-fast transaction speeds, and a way to earn yield. Raydium’s key differentiator is structure: Raydium is the first AMM on Solana and has launched the first order-compatible hybrid AMM in DeFi.

When Raydium launched, a hybrid AMM model was used that allowed idle pool liquidity to be shared with a central limit order book, whereas a typical DEX at the time could only access liquidity in its own pool. This meant that Raydium's liquidity also created a market for OpenBook, which could be traded on any OpenBook DEX GUI.

While this was a major difference early on, the feature was later turned off. Raydium currently offers three different types of pools, which are:

Standard AMM Pool (AMM v4), formally known as Hybrid AMM

Constant Product Exchange Pool (CPMM), supporting Token 2022

Centralized Liquidity Pool (CLMM)

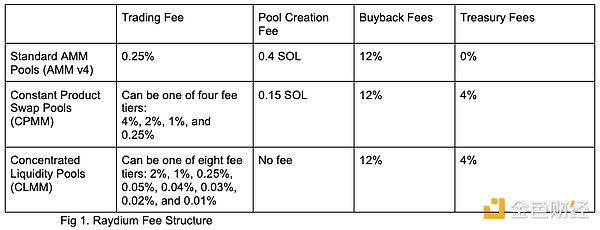

For each exchange that occurs on Raydium, a small fee is charged based on the specific pool type and pool fee level. This fee is divided into two parts, used to incentivize liquidity providers, RAY repurchases, and vaults.

The transaction fees, pool creation fees, and protocol fees of different pools on Raydium are recorded below. Here is a brief description of what each term means and their respective fee levels:

The trading fee is the fee charged to traders on a Swap transaction

The buyback fee is the percentage of trading fees required to buy back Raydium tokens

The fund management fee is the percentage of trading fees allocated to fund management

The pool creation fee is a fee levied when a pool is created, designed to discourage pool spam. The pool creation fee is controlled by the protocol multisig and is reserved for protocol infrastructure costs.

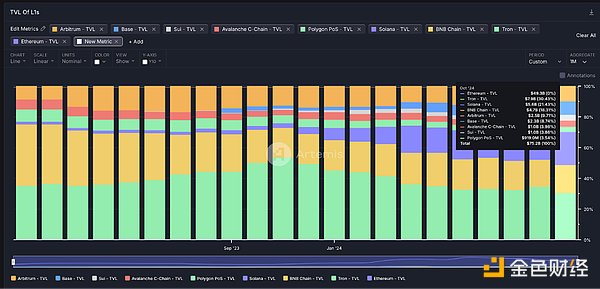

Figure 2: Solana's TVL in DEXThe above mainly analyzes the working principle of Raydium. The following is an evaluation of Raydium's position in the Solana DEX field. There is no doubt that Solana has successfully ranked among the top L1s in the 2024 cycle. Solana's TVL ranks third, behind Tron (second) and Ethereum (first).

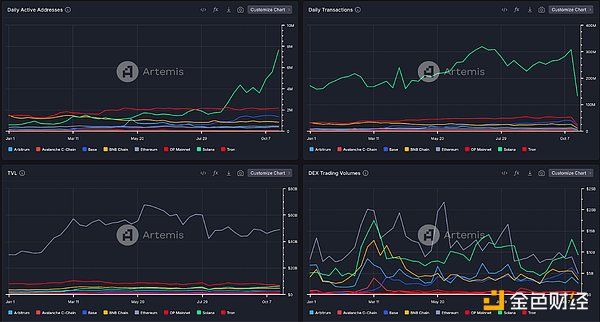

Figure 3: Daily Active Addresses, Daily Trading Volume, TVL and DEX Trading VolumeSolana continues to dominate in terms of user activity indicators such as the number of daily active addresses, daily trading volume, and DEX trading volume. The increase in activity and token liquidity on Solana can be attributed to several factors: The memecoin boom on Solana. Solana's fast and low-cost settlement, coupled with a smooth user experience for DApps, has fueled the growth and prosperity of on-chain transactions. With tokens like $BONK and $WIF reaching multi-billion dollar market caps, and the emergence of Pump.fun. As a memecoin launch platform, Solana has effectively become the home of memecoin trading.

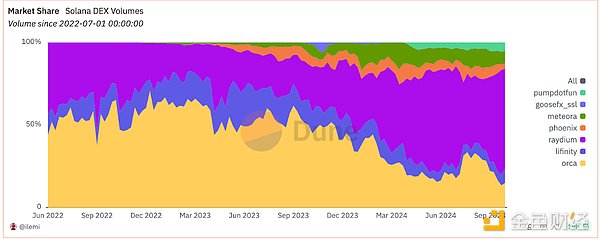

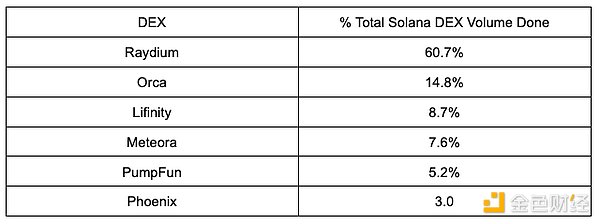

Currently Solana has been the most used L1 in this cycle, and continues to dominate in terms of trading activity. As a direct beneficiary of the increase in activity, this means that DEXs on Solana are doing very well - more traders means more fees, which means more revenue for the protocol. However, even among DEXs, Raydium has managed to capture a sizeable market share, as shown in the figure below:

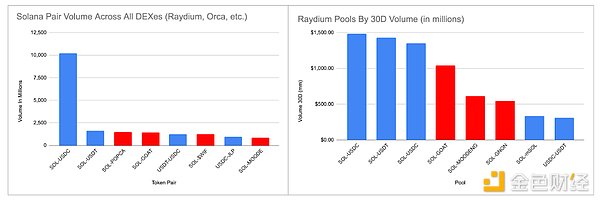

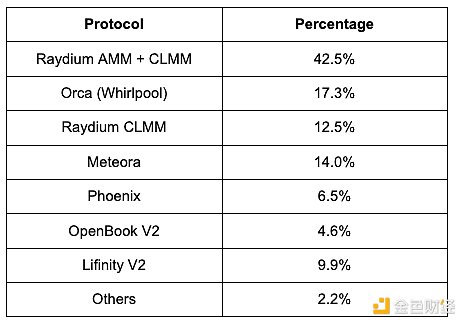

Figure 4: Market share of Solana ecosystem DEX trading volume among various DEXsRaydium ranks first among Solana DEXs, with the highest trading volume among all Solana DEXs, accounting for 60.7% of the market share of Solana DEX's total trading volume. Because Raydium allows a variety of activities on it - from memecoins to stablecoins.

One way Raydium achieves this is by providing pool creators and liquidity providers with multiple options when creating new markets. Users can choose to select a fixed product pool for price discovery at the initial launch, or choose a narrower range for LP in a centralized liquidity pool: allowing initial price discovery on Raydium while still remaining competitive in SOL-USDC, stablecoins, LST and other markets.

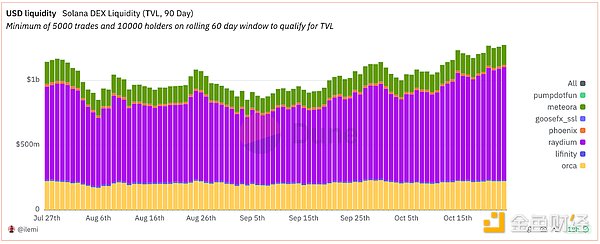

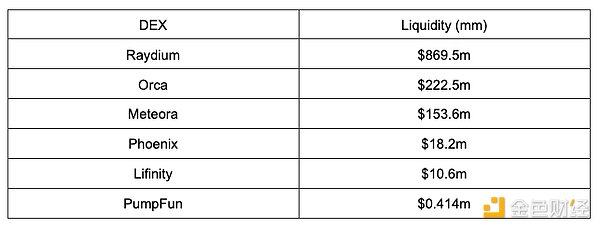

Figure 5: Solana DEX LiquidityMost importantly, Raydium remains the most liquid DEX. It is worth noting that trading is often a matter of economies of scale, as traders flock to the exchanges with the greatest liquidity to avoid slippage in their trades. Liquidity begets liquidity: When the largest DEXs attract the most traders, it becomes a positive flywheel, attracting LPs who make money from fees, which in turn attracts more traders eager to avoid slippage.

Liquidity is often an overlooked factor when comparing DEXs, but it is critical when evaluating the best performing DEXs (especially considering that traders on Solana are trading memecoins). Fragmentation of liquidity between different DEXs can lead to a poor user experience and frustration with buying a different memecoin each time between different DEXs.

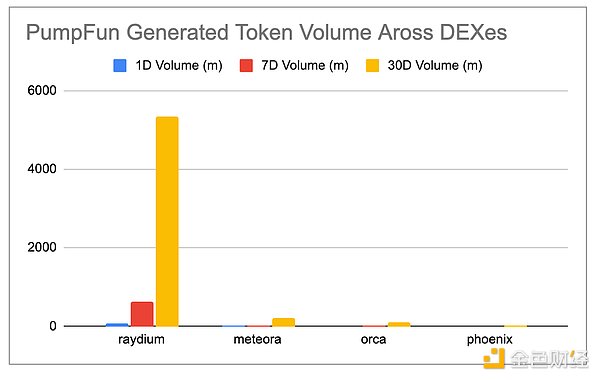

Raydium’s popularity can also be attributed to the resurgence of memecoins on Solana, specifically Pump.fun, a memecoin issuance platform that has earned over $100 million in fees since its inception earlier this year.

Pump.fun memecoins are directly linked to Raydium. When a token launched on Pump.fun reaches a market cap of $69,000, Pump.fun will automatically deposit $12,000 worth of liquidity into Raydium. Continuing with the previous point about liquidity, this means that Raydium is actually the most liquid platform for trading memecoins. It's like a virtuous cycle, pump.fun combines with Raydium -> memecoins are issued there -> people trade there -> get liquidity -> more memecoins are issued there -> get more liquidity, and the cycle repeats.

Figure 6: Number of tokens generated by Pump.Fun on DEXTherefore, Pump.fun is attributed to Raydium, and almost 90% of the memecoin generated by Pump.fun are traded on Raydium. Just like a shopping mall in a city, Raydium is the largest “shopping mall” on Solana. Most people go to Raydium for “shopping”, and most “businesses” (tokens) want to “open stores” there.

Figure 7. Trading volume of DEX token pairs on Solana and trading volume of token pairs on Raydium

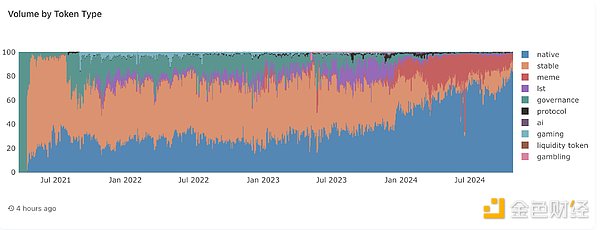

Figure 8: Raydium trading volume (by token type)

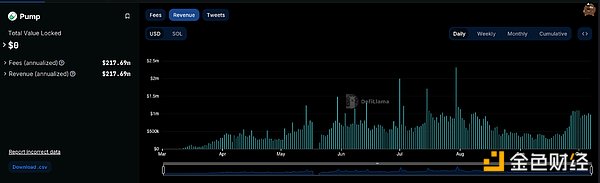

Figure 9: PumpFun Revenue

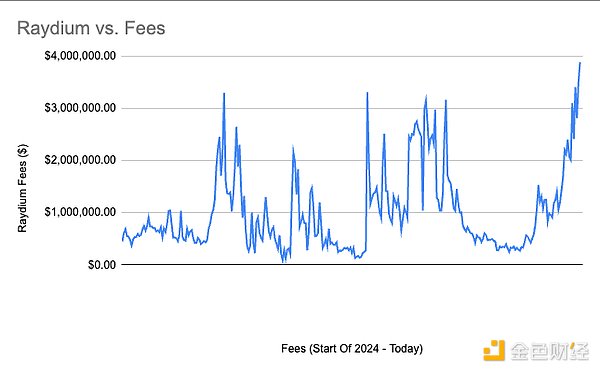

Figure 10: Raydium RevenueThat being said, memecoin is highly volatile, and pools with high volatility typically charge higher fees. So while memecoin may not contribute as much in terms of volume as the Solana pool, it contributes significantly to Raydium’s revenue and fees. This was evident in September, as memecoin is a cyclical asset that tends to underperform significantly in “bad times” as risk appetite wanes. Subsequently, Pump.Fun’s revenues fell 67% from an average of $800,000 per day in July/August to around $350,000 in September; Raydium’s fees fell similarly during this period.

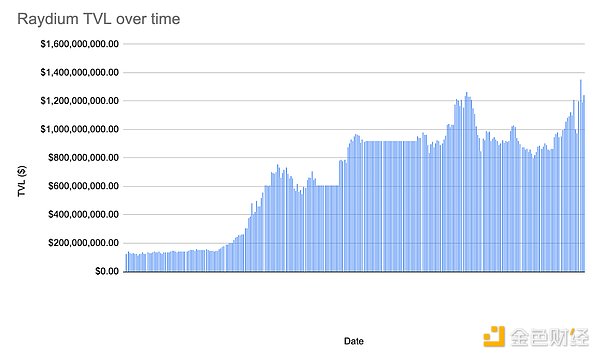

Figure 11: Raydium TVLBut like other areas of the crypto industry, this industry is highly cyclical, and it is normal to see indicators decline during bear markets as risks disappear. Instead, TVL can be used as a measure of the true anti-fragility of the protocol. While revenue is highly cyclical and rises and falls as speculators come or go, TVL is a measure of the sustainability of a DEX and how it will stand the test of time. TVL is similar to the "occupancy rate" of a mall. The utilization rate of a store may change with the seasons, just as in reality, as long as the occupancy rate of a mall is above average, it can be considered successful.

Similar to a crowded shopping mall, Raydium's TVL has remained consistent over time, indicating that while revenue may fluctuate with market prices and sentiment, it has proven its ability to become a staple in the Solana ecosystem and become the best and most liquid DEX on Solana. Therefore, while memecoins do contribute to some of its revenue, memecoin trading volume is not always the case, and liquidity still flocks to Raydium regardless of the market.

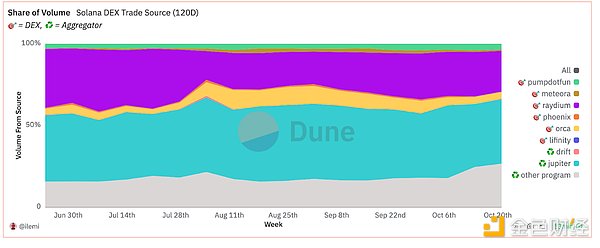

Figure 12: Solana DEX Transaction SourcesWhile Jupiter and Raydium do not compete directly, Jupiter is a key aggregator in the Solana ecosystem, trading through the most efficient path of multiple DEXs, including Raydium. Essentially, Jupiter, as a meta-platform, ensures that users get the best prices by acquiring liquidity from various DEXs (such as Orca, Phoenix, Raydium, etc.). On the other hand, Raydium, as a liquidity provider, supports many of Jupiter's transactions by providing a deep liquidity pool for Solana-based tokens.

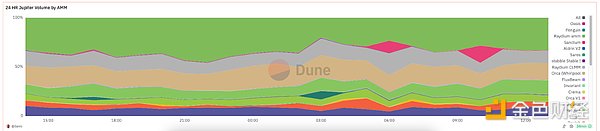

Figure 13: 24-hour Jupiter AMM transaction volumeWhile the two protocols are evenly matched, the share of organic transaction volume directly generated by Raydium is slowly increasing, while Jupiter's share is slowly decreasing. Meanwhile, Raydium accounts for nearly 50% of all pending order volume on Jupiter.

This suggests that Raydium has successfully built a more robust, self-sufficient platform that can engage users directly, rather than relying on third-party aggregators like Jupiter.

The increase in direct volume suggests that traders are discovering the value of interacting with Raydium’s native interface and liquidity pools as users seek the most efficient and comprehensive DeFi experience without having to go through an aggregator. Ultimately, this trend highlights Raydium’s capabilities as a liquidity provider in the Solana ecosystem.

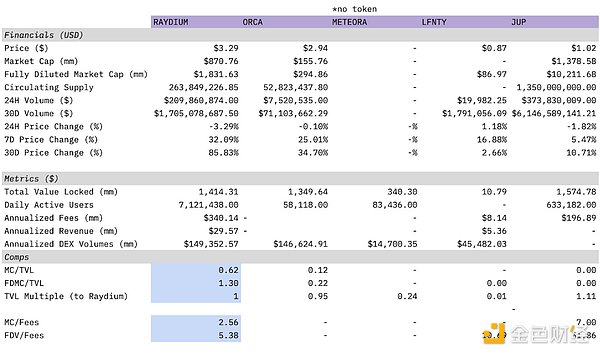

Finally, below is a comparison table built for Raydium using the Artemis plugin, comparing other DEXs on Solana, including aggregators.

Figure 14: Raydium and Solana DEX

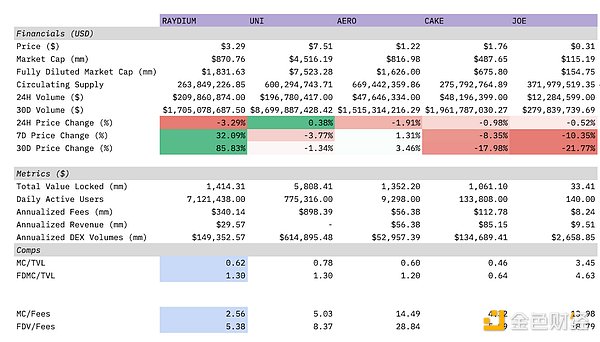

Figure 15: Raydium and Popular DEXIn Figure 13 In Figure 14, Raydium is compared to other more traditional DEXs on other chains. Raydium has more than double the annualized DEX volume of Aerodrome, but has a lower MC/Earnings ratio.

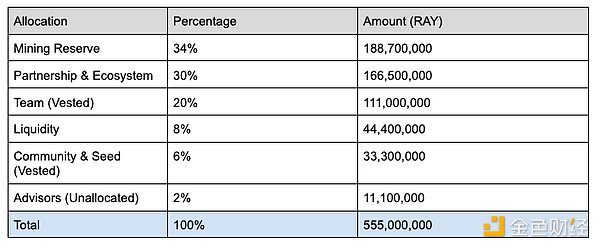

The token economics of Raydium are as follows:

Note: Team and Seed (25.9% of the total) are fully locked in the first 12 months after TGE and unlocked linearly every day in months 13 - 36. Vesting ends on February 21, 2024.

Raydium tokens have multiple use cases: $RAY owners can stake tokens to earn additional $RAY. Most importantly, $RAY is a mining reward used to attract liquidity providers to join Raydium, thereby increasing the depth of the liquidity pool. While Raydium tokens are not governance tokens, governance methods are being developed.

While issuing tokens has fallen out of favor after the DeFi summer, Raydium has an extremely low annual inflation rate and its annualized buyback is one of the best tokens in DeFi. Annualized issuance is currently around 1.9 million RAY, of which RAY staking accounts for 1.65 million of the total issuance, which is negligible compared to the issuance of other popular DEXs at their peak. At current prices, RAY issues about $5.1 million worth of RAY per year. This is very low compared to Uniswap, which has an issuance of $1.45 million per day before full unlocking, or $529.25 million per year.

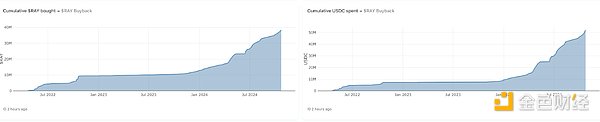

A small transaction fee is charged for each swap in each pool on Raydium. As stated in the documentation, "Depending on the specific fees of a given pool, this fee is divided into incentives for liquidity providers, RAY buybacks, and the treasury. In summary, 12% of all transaction fees are used to buy back RAY, regardless of the fee tier of a given pool."

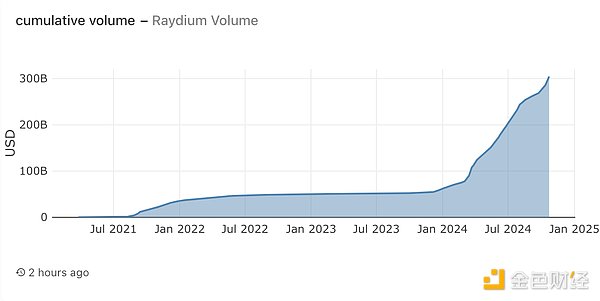

Figure 16: Raydium Cumulative Transaction Volume

Figure 17: Raydium Repurchase DataThe Case for Raydium

In summary, Raydium is essentially ahead of all DEXs on Solana and is well positioned to succeed as Solana continues to grow. Raydium has experienced growth over the past year and it doesn't seem to be stopping anytime soon as the memecoin craze continues, with the latest memecoin craze centered around artificial intelligence (such as $GOAT).

As a major liquidity provider and AMM on Solana, Raydium's unique position gives it a strategic advantage in gaining market share from emerging trends. On top of that, Raydium's commitment to innovation and ecosystem growth is reflected in its frequent upgrades, incentives for liquidity providers, and active engagement with the community. These factors indicate that Raydium is not only ready to adapt to the changing DeFi environment, but also ready to lead DeFi.

Satflow is a new DEX for professional traders built on the Bitcoin network.

JinseFinanceJupiter expands its DEX services by acquiring Coinhall and SolanaFM, enhancing multi-chain trading and data capabilities, and launching new products like Jupiter Mobile and Ape.Pro.

Edmund

EdmundGolden Finance launches the 2402nd issue of "Golden Morning 8:00", a morning report on the cryptocurrency and blockchain industry, to provide you with the latest and fastest news on the digital currency and blockchain industry.

JinseFinanceMacaron offers Macaron DeFi points worth up to $200K.

JinseFinanceTON’s DEX needs to learn from Ethereum and Solana.

JinseFinanceIn the past 24 hours, many new hot currencies and topics have appeared in the market, and it is very likely that they will be the next opportunity to make money.

JinseFinanceSolana (SOL) beats Ethereum (ETH) in 24-hour DEX volume, led by Orca (ORCA) with a 50% weekly surge. Daily victory at $1.461 billion signals changing DeFi dynamics, potential gains for SOL and ORCA tokens challenging Ethereum.

Huang Bo

Huang BoSolana's Jupiter DEX achieves a record $520 million daily trading volume, surpassing Uniswap v3's Ethereum market. Solana's native cryptocurrency (SOL) experiences a resurgence, reaching $100, while Jupiter prepares for the launch of its native JUP token.

EdmundSolana's DEXs withstand a 32% DeFi volume drop, showing only a 4% dip. Despite challenges, Solana's dominance in the market grows, marking significant yearly growth. Analysts warn of a potential price decline, emphasizing the need for cautious market navigation.

Sanya

SanyaThe Dfinity Foundation's Internet Computer blockchain welcomed its first decentralized exchange, Sonic.

Cointelegraph

Cointelegraph