Source: Web3 Lawyer

Recently, Binance Research released a research report on Web3 payment, which well sorted out the current status of traditional payment and blockchain Web3 payment, and looked forward to the future of Web3 payment by combining the advantages brought by blockchain. The research report system is complete and the arguments are sufficient, which is worth learning from.

What inspired me most was that the author Joshua Wong, based on his background as a macro analyst, was able to place Web3 payment more in the entire huge traditional financial payment system in a data-driven way, rather than falling into the obsession of purely pursuing on-chain technology.

Therefore, this article compiled the research report of Binance Research and read its index articles in depth. Only by comparing cold data can we more clearly define our own positioning and gaps, as well as the direction of the future path forward.

Below, Enjoy:

Blockchain Payments:

A Fresh Start

I. Core Views of the Report

Although the payment industry is one of the largest and fastest growing industries in the world, it still mainly relies on outdated, 50-year-old banking infrastructure. Modern payment financial technology and card organization networks such as Stripe, Mastercard and Visa have brought more convenient end-user experience to consumers and merchants. However, the traditional costs of involving up to six intermediaries in each transaction (such as card organizations, issuers, processors, POS systems, payment aggregation, digital wallets) still exist. Blockchain technology provides a new global infrastructure track for payments, which is a new beginning.

Blockchain and the range of innovative applications it supports have the potential to significantly reduce the cost and improve the efficiency of cross-border payments. This has been achieved at the institutional level, and participants such as Visa are running pilots to achieve settlement of institutional-level global payments on public blockchains. Adoption is also happening at the individual level, with products like Binance Pay being used for faster and cheaper peer-to-peer payments and cross-border transfers, as well as spending cryptocurrencies directly at merchants, without paying gas fees, automatically adjusting currency conversions and real-time settlements.

The sheer size of the payments industry means that adoption of revolutionary technologies such as blockchain can be slow and cautious. This also gives the blockchain industry itself the necessary time to grow and build the necessary payment tools and payment infrastructure.

2. Background

The use of cash for face-to-face payments gives money a unique air of freedom. Unfortunately, modern digital payment systems simply cannot provide this ability to trade directly from point to point without the intervention of a third party. This is mainly because we need a third party to hold our funds for us, unlike blockchain technology, which enables self-custody of funds.

To make matters worse, the modern global payment infrastructure stack still relies on banks and other intermediaries to process any transaction. Today's payment technology stack is in desperate need of a fresh start, and blockchain technology can achieve this.

When Bitcoin was launched in 2009 by the pseudonymous Satoshi Nakamoto, it was envisioned as a revolutionary form of peer-to-peer electronic cash payments. The goal was to create a decentralized currency that could offer the same freedoms as face-to-face cash transactions, but for digital payments. It did this by facilitating direct transactions between individuals, without the need for financial intermediaries such as banks. This vision promised to usher in a new era of financial freedom, transparency, and reduced transaction costs.

Since its inception in 2009, the modern crypto industry has undergone significant changes. The emergence of stablecoins introduced a stable value scale that can be used as a medium of value exchange and payment, while leveraging the benefits of blockchain technology to eliminate the problem of asset volatility. In addition, the development of Layer 1 and Layer 2 solutions has increased transaction speeds and reduced costs, effectively reducing the bottlenecks that previously hindered the adoption of distributed ledgers as a means of processing large-scale payment transactions.

This report will provide an overview of the current traditional payments landscape and the key issues it faces. It will then discuss how blockchain technology can address these issues, the current state of blockchain-based payments, and how the payments industry can make progress with blockchain.

III. Current Status of Traditional Payment Industry

When global payment systems such as SWIFT were first created in the 1970s, enabling global remittances was a groundbreaking achievement and a major milestone in the financial sector.

However, today's global payment infrastructure can only be described as outdated, analog, and fragmented. It is a costly and inefficient system that operates within limited banking hours and relies on numerous intermediaries. The modern financial system relies on numerous banks around the world, each of which maintains its own ledger. The lack of unified global standards among these banks hinders seamless international transactions and complicates the establishment of consistent cooperation.

The flaws of the modern payment system make cross-border interbank transactions costly and inefficient, as a single transaction may need to go through multiple correspondent banks to reach its intended destination. Sometimes, it is more like a black box, where senders and receivers cannot track the flow of funds and can only wait in the dark.

According to the World Bank, cross-border remittances typically take up to five business days to settle, with an average fee of 6.25% of the transaction amount. Despite these apparent challenges, the business-to-business (“B2B”) cross-border payments market is huge and continues to expand. The total market size for B2B cross-border payments is $39 trillion in 2023 and is expected to grow 43% to $53 trillion by 2030.

3.1 Current Traditional Payment Industry Landscape

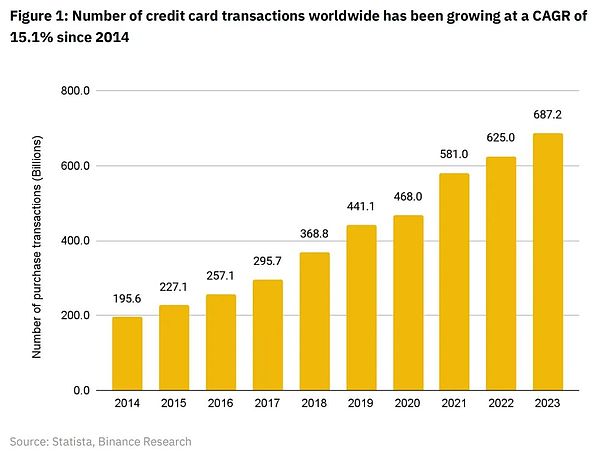

The payments industry appears to have not suffered from inefficiencies, but has grown into one of the largest industries in the world, with revenues currently estimated to reach $2.83 trillion by 2024. It is also one of the fastest growing industries, expected to reach $4.7 trillion by 2029, with a compound annual growth rate (CAGR) of 10.8%. The global payment funds reached approximately $150 trillion in 2022, an increase of 13% from 2021.

A similar picture emerges from the growth in the number of purchase transactions for global card scheme brands (American Express, Discover, JCB, Mastercard, Visa and UnionPay) over the past nine years. Purchase transactions have been growing steadily since 2014, with a CAGR of approximately 15.1%.

Despite being one of the largest and fastest growing industries in the world, much of the payments industry is still operating on 50-year-old technology tracks. The global payments landscape has evolved into a rent-collecting intermediary cartel filled with numerous middlemen who stand between merchants and consumers and collect rent from every transaction.

Innovations in the payment fintech space over the past five years have done wonders for the merchant and consumer experience. However, this has not shielded them from the high costs caused by the inefficiencies of the legacy systems that even the most advanced fintech solutions still rely on.

Broadly speaking, there are two types of payment systems in the modern payment industry: open loop payment systems and closed loop payment systems.

3.2 Open Loop Payments

Card organizations like Visa and Mastercard support the global open payment infrastructure. They enable numerous acquiring banks and issuing banks from all over the world to access the card organization network, and allow funds to flow from one bank to another through the clearing and settlement of the card organization network.

The card organization network is a priceless innovation that enables banks around the world to communicate quickly. This is an extremely consumer-friendly system that allows a single Visa/Mastercard to be used to pay for goods and services around the world. As a result, they have become the main means of digital payment in today's world. Visa and Mastercard are two of the most valuable public companies in the world today, ranking 18th and 20th respectively.

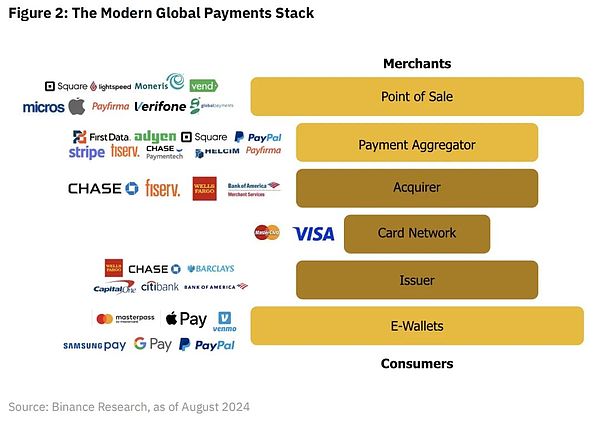

In a typical open loop payment system supported by card organization networks such as Visa and Mastercard, there are up to 6 middlemen between merchants and consumers.

1. POS service, which is a physical or digital terminal that initiates a transaction. It captures the payment details and sends them for processing. For example, Square, one of the most prominent POS service providers, charges merchants 2.6% + $0.10 per transaction. This fee is then shared among the remaining 4 intermediaries in the payment stack who collect rent (e-wallets such as Apple Pay and Google Pay currently do not charge any per-transaction fees).

2. Payment Aggregators, which consolidate transactions from multiple merchants, simplify the process of receiving payments. They provide a single integration point for a variety of payment methods. Most payment aggregators, such as Stripe, also screen transactions to detect fraud to protect their merchant customers.

3. Acquirers are financial institutions that process credit or debit card payments on behalf of merchants. It ensures that the transaction is authorized and transfers the funds from the card issuer to the merchant's account.

4. Card Networks facilitate the transmission of transaction information between acquirers and card issuers. They set the rules and standards for card transactions.

5. Card Issuers are banks or financial institutions that provide credit or debit cards to cardholders. It authorizes transactions and debits the cardholder's account. Card networks such as Visa and Mastercard also monitor transactions to detect fraud, thereby protecting their bank customers.

6. E-Wallets are digital wallets that store payment information and facilitate online and in-store transactions. They provide users with a convenient way to pay without directly using a credit card.

In short, blockchain can serve as an alternative, global, decentralized payment network - a new type of open system that is not bound by the current global payment system full of middlemen and the slow and expensive traditional banking system.

3.3 Closed Loop Payments

Closed loop payments are a growing trend in the payments industry, popularized by companies such as PayPal and Starbucks.

In a closed payment loop, consumers only interact with the PayPal app, as various merchants are included by PayPal and are able to accept payments through the PayPal network. In the case of Starbucks, customers can only use funds stored in the Starbucks digital wallet in stores. More and more merchants are beginning to follow Starbucks' lead and implement their own closed payment loops. The main purpose of doing so is to deepen customer stickiness by running their own loyalty programs and bypass the high fees imposed by existing open payment stacks.

However, the closed payment loops that exist today are highly fragmented systems that are still closely connected to the slow and expensive traditional banking system. To transfer funds in and out of the Starbucks closed loop, users still need a bank account. In addition, many merchant-specific closed loop systems (such as Starbucks) do not allow transfers between customers and are not seamlessly available in many countries around the world. Blockchain technology offers an alternative for future payment fintechs, giving them the option to completely sidestep the traditional, fragmented banking system, ultimately reducing fees for merchants and consumers.

Binance Pay is an example of such a payment fintech. It enables instant, low-fee peer-to-peer transfers and direct merchant payments within a closed-loop payment system. As a closed-loop model, the latest generation of fintechs like Binance Pay are able to provide merchants and consumers with a familiar, sophisticated, and customizable fintech experience, facilitating the transition from traditional banking rails to blockchain rails.

3.4 A New Option for Cross-Border Payments

When it comes to cross-border transactions and remittances, the costs increase exponentially. According to the International Monetary Fund, worker or migrant remittances are “part of the income sent back home by migrants in the form of cash or goods to support their families”. This is a specific area of cross-border payments that blockchain technology can have a direct impact on.

Global remittances are estimated to grow by 1.6% from $843 billion in 2022 to $857 billion in 2023. Growth is expected to reach 3% in 2024. In 2023, the top five low- and middle-income countries receiving remittance inflows in current dollars are India ($120 billion), Mexico ($66 billion), China ($50 billion), the Philippines ($39 billion), and Pakistan ($27 billion). According to World Bank data as of the first quarter of 2024, the average cost of sending $200 globally remains at 6.35% of the transfer amount, with fees totaling $54 billion per year.

Due to the extremely high costs, cross-border remittances are a key area of the payments industry where blockchain can really make a big impact.

Cross-border remittances involve sending money across borders through a series of banks located in different countries, a process that can take several days, making it slow and costly.

1) The process begins when a remitter initiates a money transfer at a local bank or remittance service, providing the recipient's details and the amount to be sent.

2) Since the remitter and recipient's banks may not have a direct relationship, an intermediary bank, known as a correspondent bank, facilitates the transaction. The remitter's bank sends the funds to its correspondent bank, which may then pass the funds on to other correspondent banks, each of which charges a fee. The SWIFT network is often used to send such payment instructions during this process.

3) If different currencies are involved, the funds are usually exchanged at one of the correspondent banks, usually at a lower exchange rate.

4) Each bank must comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations, verifying identities and ensuring the legitimacy of the transaction. Transactions are also screened against international sanctions lists.

5) Once processed and compliance checks are completed, the funds are transferred to the recipient's bank, which credits the funds to the recipient's account. The sender receives confirmation that the transaction is complete.

The traditional payment systems described above are not only costly and inefficient, but they currently fail to cover a significant portion of the world's population.

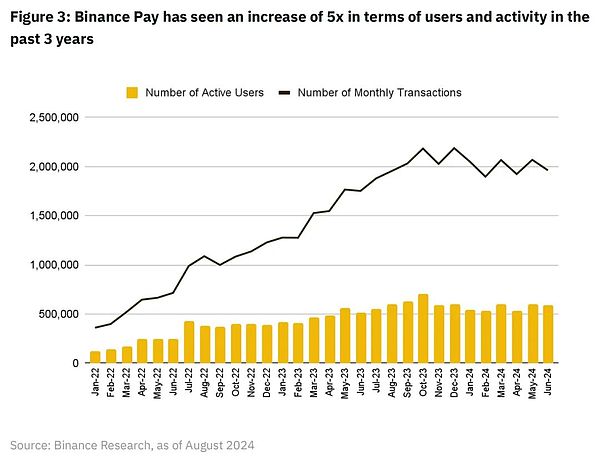

Today, as many as 1.4 billion adults worldwide do not have a bank account. For these reasons, we have seen users around the world turn to blockchain solutions such as Binance Pay as a cheaper and faster way to transfer money across borders. Since 2022, Binance Pay has seen nearly 5x growth in both monthly active users and monthly transactions, with approximately 13.5 million users worldwide and approximately 1.96 million monthly transactions.

Blockchain and distributed ledger technology (DLT) has the potential to disrupt many existing players in the payments industry by providing a unified, global, transparent payment environment that can be accessed with just a smartphone and an internet connection. This means that there will be more direct communication channels between merchants and consumers, driven by distributed ledgers and eliminating the need for agency banks. Liberating future fintech from the traditional banking system could be the key to achieving cheaper and faster payments around the world. Jason Clinton, head of sales for JPMorgan Chase's European Financial Institutions Group, said: "Ultimately, we want to be able to settle any payment instantly in any currency, anywhere, at any time, and this may require the use of blockchain technology."

Fourth, Current Status of Blockchain-Based Payments

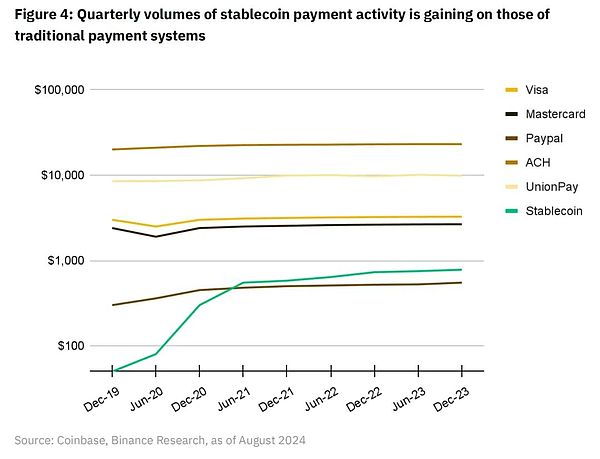

Due to their high cash equivalence, stablecoins have become a key component of blockchain payments. In 2023, stablecoins processed more than $10.8 trillion in transactions, excluding activities such as machine or automatic transactions, the figure was $2.3 trillion.

Comparing stablecoin payments with traditional payments, we can see that they have been catching up with traditional payments in terms of quarterly transaction volume.

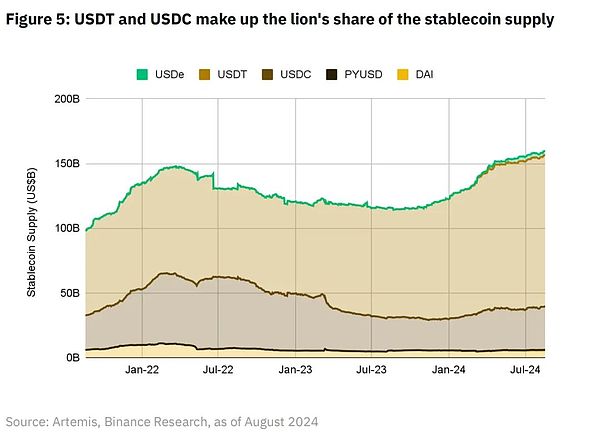

The total supply of stablecoins has also been increasing since mid-2023, indicating a steady increase in demand. The total market capitalization of major stablecoins exceeds $160 billion, with USDT and USDC accounting for the largest share, with market shares of 73% and 21%, respectively.

Leveraging the low volatility provided by stablecoins, the blockchain payment ecosystem and its related infrastructure have made great progress since 2009.

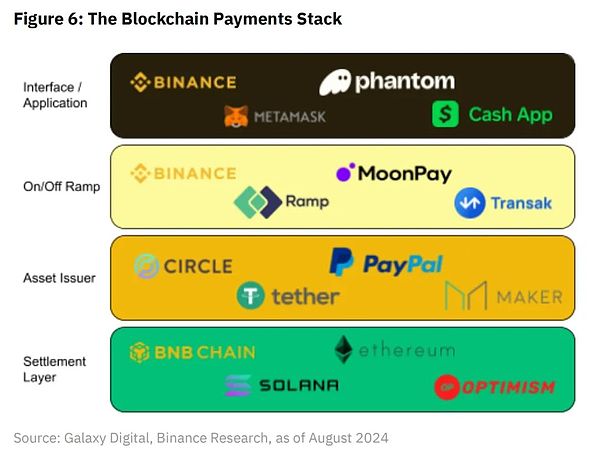

4.1 Blockchain-based Payment Infrastructure

Settlement Layer

Sponsored Business Content

Blockchain infrastructure responsible for transaction settlement, such as Bitcoin, Ethereum, and Solana, are all Layer1 blockchains, and versatile Layer2 solutions such as Optimism and Arbitrum are essentially selling block space.

These platforms compete on speed, cost, scalability, security, and distribution. Over time, the payments use case is likely to become a significant consumer of blockchain space.

We can think of the settlement layer as the network of banks that make up the current traditional payment system. Instead of having to store funds in a centrally managed bank account, consumers and merchants can store assets in an on-chain externally owned account (EOA) or smart contract account.

It is worth noting that in the modern payment stack, authorization and settlement are handled separately. Card organizations such as Visa and Mastercard provide payment authorization services; issuing banks and acquiring banks are responsible for handling the actual payment settlement. For blockchains, authorization and settlement can theoretically be synchronized. A consumer can send a transaction of 100 USDT directly from their EOA to the merchant's EOA by signing a transaction authorization, and the validator will process and settle this transaction immutably on the blockchain.

It is worth noting, however, that relying solely on blockchain for the settlement and authorization of P2P payment transactions could mean bypassing the systems of clearing, transaction monitoring, and fraud detection services employed by payment aggregators such as Stripe and credit card networks such as Visa.

Visa itself has been a frontrunner in piloting blockchain for payment use cases over the past few years, with the company envisioning a future where “Visa’s network involves not only multiple currencies and bank settlement corridors, but also multiple blockchain networks, stablecoins, and CBDCs or tokenized deposits.”

Asset Issuer LayerAsset Issuers

Asset issuers are the organizations responsible for creating, managing, and redeeming stablecoins — a crypto asset that is designed to maintain a stable value relative to a reference asset or basket of assets, most commonly the U.S. dollar. These issuers typically adopt a balance sheet-driven business model similar to that of banks. They accept customer deposits, invest those funds in higher-yielding assets such as U.S. Treasuries, and issue stablecoins as liabilities, profiting from the interest rate spread or net interest margin.

Asset issuers are a new type of “intermediary” that exists in the crypto payment stack and has no direct equivalent in the traditional payment stack. Perhaps the closest equivalent is the government that issues the fiat currency used to conduct transactions.

Unlike intermediaries in traditional payments, asset issuers do not collect fees from every transaction using their stablecoin. Once a stablecoin is issued on-chain, it can be self-custodied and transferred without any additional fees to the asset issuer.

On/Off Ramp Layer

On/Off Ramp Layers are critical to increasing the usability and adoption of stablecoins in financial transactions. Fundamentally, they act as a technical bridge connecting stablecoins on the blockchain with the fiat system and bank accounts. Their business model is typically traffic-driven and only accounts for a small portion of the total USD volume that passes through their platform.

Currently, the on/off ramp layer is often the most expensive part of the crypto payment stack. Service providers such as Moonpay charge up to 1.5% to transfer assets from the blockchain to a bank account.

Transactions from fiat currency held in a consumer’s bank to an on-chain stablecoin to fiat currency held in a merchant’s bank can cost up to 3%. This aspect is perhaps the biggest barrier to widespread adoption of blockchain payments in terms of cost, especially for merchants and consumers who may still need fiat currency in their bank accounts for day-to-day transactions. To address this, products such as Binance Pay are building their own merchant networks where users can spend cryptocurrencies directly, without the user incurring costs.

Interface/Application Layer

Front-end applications are the customer-facing software in the crypto payments ecosystem that provide a user interface for crypto-enabled transactions and leverage other components of the stack to facilitate these payments. Their business models typically include platform fees and transaction-based fees, earning revenue based on the volume of transactions processed through their interface.

4.2 Leveraging the Advantages of Blockchain-Based Payments

Near-Instant Settlement

When using a Visa or Mastercard card to make a transaction, consumers experience the convenience of near-instant payment authorization. However, the actual settlement of the transaction, where funds are transferred from the customer’s bank account (issuing bank) to the merchant’s bank account (acquiring bank), typically does not occur until at least a day later. While the card schemes allow consumers to make digital payments in seconds, merchants typically do not receive funds for that purchase until the next day or later. Settlement times are longer when funds need to be transferred across borders, as this requires communication between banks in different countries.

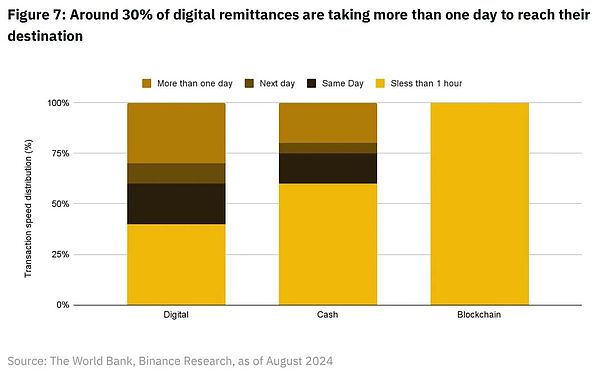

The inefficiencies of the cross-border interbank communication system are evident when looking at remittance transaction times. Somewhat counterintuitively, approximately 30% of remittances take more than a day to reach their destination; this is higher than the 20% of cash remittances that take the same amount of time.

The World Bank attributes this to two reasons:

(1) Remittances cover traditional banking services, i.e. bank account to bank account services, which are slow.

(2) Most non-bank remittance service providers are likely to pre-fund transactions, providing fast services to end users who use cash.

For example, of the three payment media (digital, cash, and blockchain), blockchain is the clear leader in terms of speed, with 100% of transactions completed in less than an hour.

In 2021, Visa conducted a pilot with Crypto.com, using USDC and the Ethereum blockchain to process payments for cross-border transactions made by Crypto.com on Australia's real-time card program. Currently, Crypto.com uses USDC to fulfill its Visa card settlement obligations in Australia and plans to expand this capability to other markets.

Prior to this pilot, settlement of cross-border purchases using the Crypto.com Visa card involved a lengthy currency conversion process and costly international wires.

Now, Crypto.com can send USDC directly across borders to a Circle-managed Visa financial account via the Ethereum blockchain, significantly reducing the time and complexity associated with international wires.

At the individual user level, services like Binance Pay allow users to instantly transfer crypto across borders.

Reduced Costs

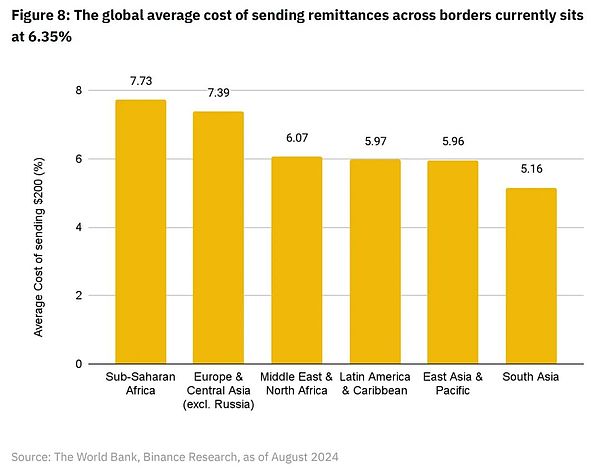

According to the World Bank, the average cost of sending remittances across borders has dropped from 6.39% in the fourth quarter of 2023 to 6.35% in the first quarter of 2024. According to their breakdown of average costs by region around the world, Sub-Saharan Africa is the most expensive region to send remittances, with an average cost of 7.73%.

For comparison, the average cost of sending $200 worth of stablecoins (or any amount of stablecoins, as most blockchains charge a fixed gas fee regardless of the transfer amount) through a high-performance blockchain like Solana is about $0.00025. Products like Binance Pay allow users to make borderless peer-to-peer stablecoin transfers at a relatively much lower fee, as long as the transfer amount is less than 140,000 USDT. For values above that amount, a fee of $1 is charged.

It is worth noting that currently, the on- and off-currency conversion is the most expensive part of any transaction involving on-chain assets. CryptoConvert, which Binance is partnering with in Q4 2023, provides a service that allows South African consumers to purchase goods using their digital assets. This eliminates the need for on- and off-currency conversions and is the beginning of incorporating a network of merchants into a crypto-native closed payment loop.

Transparent and trustless network

In an era where traditional payment systems such as SWIFT are being used for geopolitical purposes, blockchain technology offers a revolutionary alternative. With its inherent transparency, every transaction on a blockchain is recorded on an immutable ledger visible to all network participants. This openness fosters trust and consensus, discouraging fraud and manipulation.

Decentralization is another key advantage. Unlike centralized systems, blockchain spreads control across a vast network, reducing the risk of single points of failure and abuse of power. No single entity can impose sanctions or restrictions, ensuring that the global payment system is neutral and accessible. The decentralized nature of blockchain enhances its security, making it resilient to attacks. Hacking a blockchain network requires enormous computing power, far more than traditional systems.

In addition, blockchain simplifies transactions by enabling peer-to-peer payments, reducing intermediaries and lowering fees. Cross-border payments that once took days can now be completed in minutes, facilitating real-time global trade. Blockchain provides a viable, globally unified alternative to the existing decentralized banking system for storing and transferring digital value.

V. Current Dilemma of Blockchain-Based Payments

Scalability andPerformance

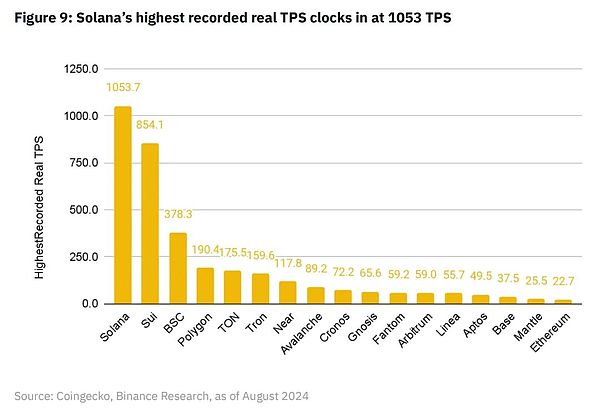

A globally accessible payment network must be able to support cheap, fast transactions and operate around the clock. Because payment networks are required to be able to process thousands of transactions per second, even a momentary delay can have a significant impact on global business operations. For example, Visa can process more than 65,000 transactions per second.

Solana is the blockchain with the highest number of user-generated transactions per second (TPS) recorded to date, with a daily average TPS of just over 1,000. Sui is reportedly close behind, with an actual maximum TPS of over 850. BNB Chain ranks third on this metric, at 378.3 TPS.

In 2023, Visa processed about 720 million transactions per day, which means an average daily TPS of about 8,300 in 2023.

This is still nearly 8 times the maximum user-generated TPS recorded by Solana.

In addition to TPS issues, Solana has also exhibited performance issues. Since the mainnet launch in 2020, Solana has experienced 7 major outages that brought block production to a standstill, with the most recent occurring in February 2024. Such serious incidents have caused institutions to be cautious about relying on blockchains for critical business operations, such as payments.

However, despite these issues, Solana has been adopted by many pioneering institutions. Visa describes it as a "viable test and pilot payment use case" due to its "high demonstrated throughput levels."

PayPal also chose Solana as the second chain to launch its PYUSD stablecoin after Ethereum. At the time of writing, the PYUSD supply on Solana ($377 million) has surpassed the supply on Ethereum ($356 million), despite launching nearly a year later.

On-Chain Complexity

Blockchains are complex in large part due to their decentralized nature, making them more inconvenient for consumers and merchants to adopt than centralized systems. Requirements for end users, such as private key management, paying gas fees, and the lack of a unified front end make adopting blockchain technology a major challenge for the average consumer and merchant.

Meanwhile, over the past 5 years, payment fintechs such as Square and Stripe have taken the payment experience for merchants and consumers to a very high level. In general, it does this by abstracting all the underlying complexities of middlemen, correspondent banks, and other third parties. So, in terms of the traditional global payment stack, what we have today is a highly sophisticated system that constitutes the traditional payment system at a cost of up to 3% per transaction, both from a consumer and merchant perspective.

Fortunately, with the rise of faster and cheaper blockchain infrastructure, there have also been many improvements in the UI/UX of blockchain applications. Binance Pay offers users a familiar centralized fintech experience while being untethered to the traditional banking system. This gives users the freedom to send cryptocurrencies to each other globally with low fees, while also having the option to easily withdraw crypto assets into self-custody if they choose to do so.

Regulatory Uncertainty

The current regulatory environment for cryptocurrencies and blockchain technology is still evolving, creating uncertainty for businesses and consumers. Regulations vary widely from country to country, complicating global operations and cross-border transactions.

Countries such as Switzerland and Singapore are developing clear regulatory frameworks to provide guidance and promote innovation in the blockchain space. The EU’s Markets in Crypto-Assets (MiCA) regulation is another example of an effort to create a coordinated regulatory environment. The blockchain industry is also developing compliance solutions to help businesses navigate the regulatory landscape. Providing individuals and businesses with the necessary tools to monitor and ensure compliance with anti-money laundering (AML) and know your customer (KYC) regulations is key to adoption.

VI. Future blockchain-based payments

Blockchain provides a unified technology infrastructure that simplifies the payments landscape and transcends the fragmented nature of the modern banking system. As a global decentralized ledger, blockchain eliminates the inefficiencies inherent in traditional banks that rely on maintaining and synchronizing multiple centrally managed bank accounts. Blockchain therefore provides a new medium that has the potential to reduce costs and increase the speed of global payments.

As mentioned earlier in this report, payments giant Visa is experimenting with using blockchain as a cheaper and faster way for its institutional clients to settle global payments. Today, one of Visa's clients, Crypto.com, can send USDC across borders directly to a Circle account managed by Visa Finance via the Ethereum blockchain. This reduces the time and complexity of international wire transfers, which previously took days to process. As companies become more familiar with blockchain technology, many may choose to use on-chain stablecoins for transactions rather than the slower and more costly fiat banking system.

On a smaller peer-to-peer scale, blockchain is likely to have a faster and more significant impact on the global payments industry, particularly in the area of cross-border remittances. Many recipients of remittances are unbanked or underbanked. Blockchain technology offers the possibility of “leapfrogging” the traditional banking system so that anyone with an internet connection and a smartphone can quickly begin receiving payments from anywhere in the world.

Blockchain essentially provides a new, decentralized medium through which payments can be made more seamlessly around the world. As the modern payments industry continues to experiment with this new technology and integrate it into parts of the global payments system, the ultimate goal that we should always keep in mind is a world of free money that is cheaper, faster, and more efficient for everyone.

Weiliang

Weiliang