Elon Musk Forecasts AI to Surpass Smartest Human by 2025

Elon Musk has made a bold prediction, foreseeing that advancements in AI will surpass the capabilities of even the most intelligent humans by 2025.

Catherine

Catherine

Analyst: Manuel|Grant|Corey Compiler: Matt|Peter

If there is a track that can become a key force in promoting financial innovation and blockchain applications like DeFi, and shape the new financial landscape of the future, then 5Mind DAO will vote for PayFi.

Concept of PayFi

PayFi (Payment Finance) is a relatively new concept that combines payment and decentralized finance (DeFi). It was first proposed by Lily Liu, chairman of the Solana Foundation, and defined as a new financial market built around the time value of money.

To understand PayFi, you first need to clarify the "time value of money". "Time value of money" means that the value of money changes over time. Usually (taking into account inflation and investment income issues, etc.), the current value of the same amount of money is higher than the future value of the same amount of money (100 yuan this year > 100 yuan next year); if people want to get money now, rather than in the future, then they should pay extra for these funds, that is, interest.

Let's take an example to make it simple: suppose you can get 1,000 yuan now, and if you deposit it in a bank, the annual interest rate is 5%. After one year, you will get 1,050 yuan (1,000 yuan principal + 50 yuan interest). In this case, the value of 1,000 yuan today is higher than 1,000 yuan a year later, because you have the opportunity to get interest returns through investment. If the inflation rate is 5%, then the purchasing power of 1,000 yuan a year later is: 1,000*(1-0.05)=950, which is equal to 950 yuan today.

In addition, since payment itself is rooted in real-world life scenarios, in order to effectively capture the time value of money in real-world payment scenarios, real-world assets (such as real estate, equity, bonds, etc.) must be introduced into the blockchain through tokenization (RWA), and payment and business processes must also be moved to the blockchain to form the logic of Web3 payment.

From this, we can make a more detailed supplement to PayFi. PayFi refers to the innovative financial field that improves and optimizes the payment system based on the payment settlement scenario and the time value of money through blockchain technology, smart contracts and tokenization.

Traditional payment and Web3 payment

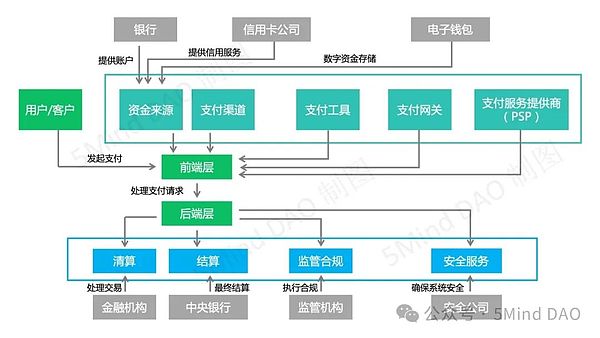

We know that payment is the act of transferring funds to ensure the completion of transactions and the realization of value exchange. However, traditional payments usually rely on centralized payment networks and intermediaries (such as banks, credit card companies, payment gateways, etc.) to complete the transaction process. This multi-party participation method greatly increases transaction time and fees. Especially in the context of globalization, cross-border payments involve domestic clearing systems in various countries (such as Fedwire of the US central bank and CNAPS of the Chinese central bank), cross-border payment and clearing systems for settlement currencies (such as CIPS of the cross-China RMB clearing system and CHIPS of the New York Clearing House), international funds clearing systems (such as SWIFT, the Society for Worldwide Interbank Financial Telecommunication), and various banks participating in these systems. The complexity is obvious.

*Note: Traditional payment structure

On the other hand, Web3 payment based on blockchain technology and decentralized concepts effectively takes advantage of the characteristics of blockchain: near-instant settlement, 24/7 availability, low transaction costs, and the programmability, interoperability, and unlimited possibilities of the composability of digital currency itself with DeFi.

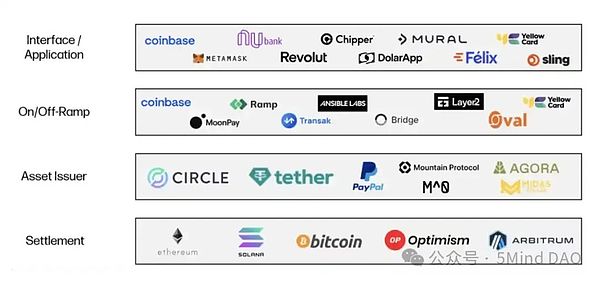

So, how does Web3 payment achieve value transfer? From the perspective of the technology stack, Web3 payment is mainly divided into four layers: Settlement layer (blockchain), asset issuer, currency acceptance (legal currency channel) and front-end application.

*Source: Galaxy Ventures

Settlement layer: The underlying blockchain infrastructure for settlement transactions, equivalent to the "settlement agency" or "clearing system" in the traditional financial system, is responsible for ensuring that all transaction information is recorded and confirmed on the blockchain and cannot be tampered with. Layer1 such as Bitcoin, Ethereum, Solana and general Layer2 such as Optimism and Arbitrum provide different settlement solutions to the market by selling their block space (users pay gas fees to use the storage and processing resources of the blockchain, record their transactions or data on the blockchain, and complete transaction confirmation and settlement). These chains have their own advantages in speed, cost, scalability, security and distribution channels.

Asset issuer: An institution or entity that creates and issues digital assets (such as stablecoins, tokens, etc.) on the blockchain, responsible for establishing, maintaining and redeeming financial transactions and payment media. For example, the well-known asset issuer Tether created the stablecoin USDT pegged to the US dollar (USDT is pegged to the US dollar at a 1:1 ratio), allowing users to use USDT on the blockchain for payment and value exchange without worrying about the value fluctuations of the token. This is also one of the most widely used digital assets in the cryptocurrency market.

Currency acceptance:It is an important channel that connects digital currencies on the blockchain with fiat currencies in traditional bank accounts. Currency acceptance providers play a key role in increasing the availability and adoption of stablecoins as the main mechanism for financial transactions. Their business model is often traffic-driven and they take a small commission from the funds flowing through their platform.

Front-end application:The final manifestation of the front-end application is customer-facing software that provides a user interface for crypto payments and leverages other parts of the stack to enable such transactions. Their business models vary, but they are often some combination of platform fees plus traffic-driven fees generated through front-end transaction volume.

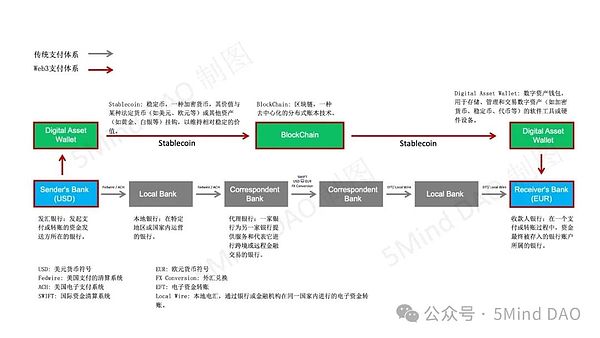

To help users further understand the difference between traditional payments and Web3 payments, we use the structure of a cross-border payment transaction as an example.

*Click to enlarge

Different countries and financial institutions may have different regulatory requirements, payment systems and information transmission standards. In addition, due to limited banking hours and reliance on many intermediaries, cross-border payments under the traditional payment system often incur high costs (transaction fees, exchange rate markups, intermediary fees, etc.), and take up to 5 working days to settle. In addition, the opacity of the entire cross-border payment process may also cause problems such as difficulty for users to track and verify payments.

The cross-border payment solution under Web3 payment can settle transactions instantly on a global scale simply through stablecoins built on the blockchain. Web3 payments can provide lower costs compared to traditional payments due to the elimination of various intermediaries and their infrastructure; coupled with the open and transparent nature of blockchain, users also gain greater visibility and convenience in tracking fund flows and reducing reconciliation management costs.

It is not difficult to see that Web3 payments, a new payment method that does not rely on traditional financial institutions but directly transfers value between users through a decentralized network, can greatly simplify the payment and settlement process, making payments fast, cheap and easy to access, and is the only choice to meet the public's current payment needs.

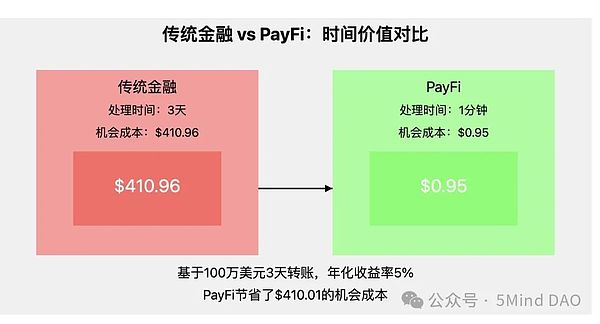

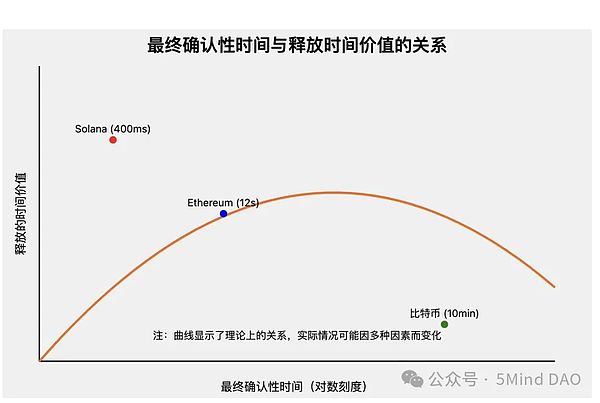

If Web3 payments are mainly used to trade with the money we have now, then PayFi allows us to trade with tomorrow's money.Let's use a simple mathematical model to illustrate the time value of money captured by PayFi in this process:

Assume that there is a sum of $1 million in funds, which takes 3 days to complete a cross-border transfer in the traditional banking system. With an annualized rate of return of 5%, the opportunity cost of these three days is: 1 million * (5% / 365) * 3 = $410.96. Now, suppose PayFi shortens this process to 1 minute: 1 million * (5% / 525600) * 1 = $0.95.

*Source: @0xNing0x

It is worth noting that the time value of the currency released is nonlinearly related to the final confirmation time. Therefore, it is extremely important to find a balance between speed, security and decentralization when designing the PayFi system.

*Source: @0xNing0x

PayFi's Market Size

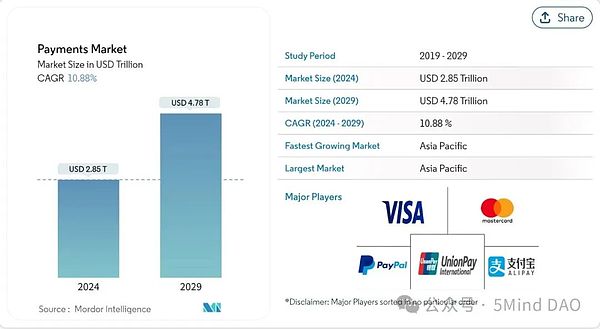

From the perspective of the overall macro market, according to the "Cryptocurrency Market Report" released by Mordor Intelligence, the cryptocurrency market size is expected to be US$44.29 billion in 2024 and will reach US$64.41 billion by 2029, with a compound annual growth rate of 7.77% during the forecast period (2024-2029). Thanks to the adoption of digitalization, the global payment system is rapidly shifting from cash to digital payments, and crypto payments, as a newly emerging innovative payment method, are gradually becoming an important force in digital payments.

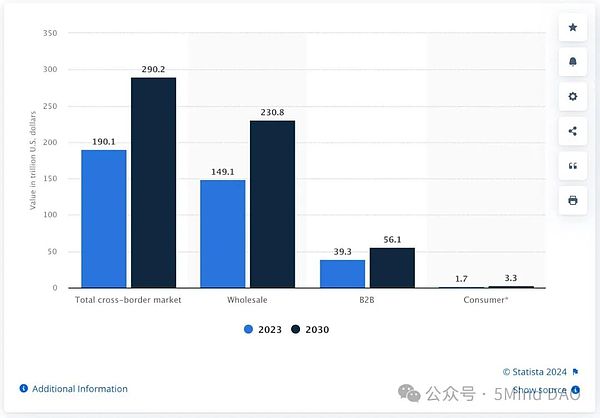

The report predicts that the increasing use of cryptocurrencies for cross-border remittances will expand the market by reducing consumer fees and exchange costs. Data compiled by Statista show that the total value of cross-border payments will be $190.1 trillion in 2023. This figure is expected to reach $290.2 trillion by 2030, with most of the growth coming from the expansion of cross-border payments initiated by consumers.

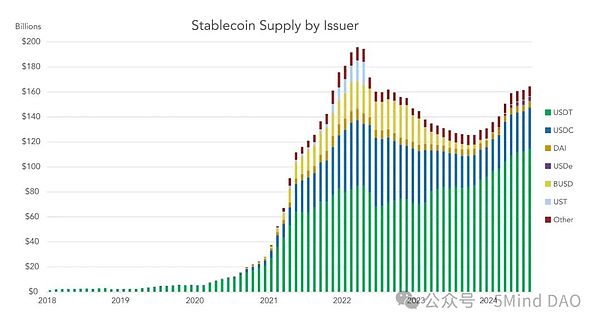

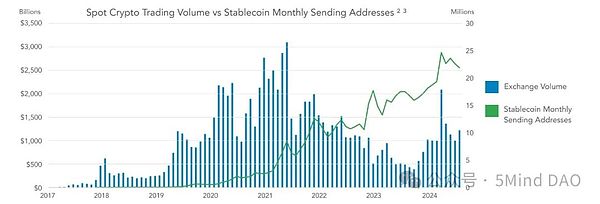

On the other hand, stablecoins are anchored to fiat currencies, avoiding the volatility of cryptocurrencies and becoming an important financial tool and transaction medium in the Web3 field. Since 2020, the global supply of stablecoins has continued to rise, especially stablecoins pegged to the US dollar (such as USDT and USDC). According to the latest research from institutions such as Visa and Castle Island Ventures, the total circulating supply of stablecoins will exceed US$160 billion by 2024, while in 2020, this figure was only a few billion US dollars. This substantial increase not only reflects the strong market demand for stablecoins, but also highlights its huge potential in solving cross-border payments, savings protection and currency conversion.

*Stablecoin supply divided by issuer

According to the latest research estimates released by institutions such as Visa and Castle Island Ventures, the total settlement amount of global stablecoins in 2023 is conservatively estimated to reach US$3.7 trillion, and the settlement amount in the first half of 2024 will reach US$2.62 trillion (the same period, the data in the 2024 Cryptocurrency Status Report released by a16z was US$8.5 trillion). On an annualized basis, this figure is expected to rise to US$5.28 trillion for the whole year. Another interesting phenomenon is that although the cryptocurrency market experienced greater volatility and a downward cycle from 2022 to 2023, the trading volume and usage frequency of stablecoins were not significantly affected. This shows that stablecoins are no longer limited to the cryptocurrency market, and their application scenarios are rapidly expanding to the real economy.

*Comparison of spot trading volume of cryptocurrencies and the number of monthly active sending addresses of stablecoins

PayFi's innovation needs

From the market demand side, on the one hand, the old (SWIFT was established in 1973), complex and inefficient traditional payment and settlement system has given rise to an urgent need for the adoption of Web3 payments. Coupled with today's increasingly complex geopolitical environment and financial oligarch effects, its neutrality is even more questionable (in 2022, against the backdrop of the intensified conflict between Russia and Ukraine, Russia was removed from the SWIFT system, a move that almost stagnated Russia's cross-border payments and import and export settlements, bringing great pressure to its economy).

On the other hand, in the context of insufficient innovation and lack of liquidity (the ability to quickly buy or sell assets/markets at close to market prices) in the current crypto market, PayFi, which combines payment and DeFi, shows great potential, especially in improving currency turnover efficiency and increasing market liquidity. By connecting real assets with on-chain financial activities through stablecoins, RWA and other means, PayFi can increase the real demand of the market, reduce speculative behavior, and make the liquidity of the entire crypto market more solid and stable. At the same time, it can also attract more users who are interested in blockchain applications, especially traditional financial users who want to enter the crypto market but have not found a suitable entry point. In addition, unlike the short-term high-yield incentives in DeFi, PayFi emphasizes long-term use value and actual payment scenarios. The more frequently users use PayFi, the stronger their stickiness, and the liquidity of the market will also increase accordingly.

To sum up, PayFi's market demand comes from the demand for payment efficiency, cost, cross-border payment, transparency, security and the integration of real-world assets and on-chain assets, which has irreplaceable advantages and broad market prospects. With the rapid development of Web3 and decentralized finance, PayFi is expected to become a key infrastructure in the future digital economy, meeting the multi-level needs of digital payment, financial innovation and global users.

PayFi's business model

Unlike DeFi, PayFi does not focus on lending and high-yield investment, but emphasizes the smoothness, security and wide practicality of payment. From the perspective of business model, PayFi can currently be divided into four categories:

A. Move traditional payment logic to the blockchain, aiming to build a comprehensive Web3 payment framework.Representative projects: stablecoins (USDT, USDC, PYUSD, etc.).

Stablecoins, as one of the key components to move traditional payment logic to the blockchain, not only provide the foundation for the Web3 payment framework, but are also the most successful PayFi application at present. In addition to tokenizing real assets, the integration of stablecoins and DeFi fully demonstrates its advantages of interoperability, programmability and composability, and maximizes the capture of the time value of money (similar to interest and compound interest in traditional finance).

This capture of time value not only encourages users to hold and use stablecoins, but also enhances the attractiveness of cryptocurrencies and blockchains in daily payments and financial management. For example, before payment or during the payment waiting period, deposit stablecoins into the liquidity pool to obtain transaction fee income provided by the platform. In this process, the payment can not only capture the time value, but also provide liquidity for on-chain transactions.

B. Payment Tokens, such as tokens representing the time value of tokenized U.S. Treasury bonds or stablecoins that generate income. Representative Project: Ondo Finance.

Ondo Finance

Ondo Finance is a decentralized institutional-level financial protocol. Its main business is to introduce zero/low-risk, stable interest-bearing, scalable fund products (such as US Treasury bonds, money market funds, etc.) into the blockchain (tokenization) within the compliance framework for investors on the chain to invest, lower the threshold for ordinary investors to enter financial products, and enable holders to obtain income from their assets.

The tokenized financial products currently launched by Ondo Finance mainly include the interest-bearing stablecoin Ondo US Dollar Yield Token ($USDY) and the tokenized US Treasury fund Short-Term US Government Treasuries ($OUSG). KYC certification is required to purchase the above products.

USDY is a tokenized note secured by short-term U.S. Treasuries and demand bank deposits, available for purchase by non-U.S. individuals and institutional investors. Investors receive a token certificate after making a contribution and receive USDY in 40–50 days, which they can transfer on-chain for free. In addition to being a payment medium, USDY can also provide additional capital efficiency utility and composability in DeFi scenarios, such as using USDY as collateral when borrowing.

Compared to stablecoins, USDY's innovation is that it provides investors with an investment tool that can store dollar-denominated value and generate dollar returns without permission. The token price of USDY is calculated based on the token price on the first business day of the month and the token yield for that month.

For example: If the price of USDY on June 1 is 100.00000000 USD and the APY in June is 4.000000000%, the price of USDY on June 3 will be: 100.00000000 × ( 1 + [( 1 + 0.04 )1365–1 ])2 = 100.02149311 (keep eight decimal places). As of November 10, 2024, the price of USDY is 1.0665 USD.

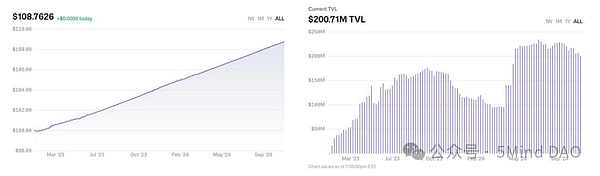

It is reported that the annualized rate of return (APY) provided by USDY is adjusted by Ondo every month according to actual conditions. As of November 10, 2024, USDY's APY is 4.90%, and the total locked value (TVL) is approximately US$451.87 million. The collateral value is approximately US$451.69 million, the over-collateral amount is US$14.06 million, and the over-collateral rate is 3.11%. (USDY is a senior debt secured by bank demand deposits and short-term U.S. Treasury bonds. Ondo overcollateralizes it and provides a 3% first loss position to absorb short-term fluctuations in U.S. Treasury prices. That is, for every $100 worth of USDY issued, there are at least $103 worth of bank deposits and U.S. Treasury bonds as collateral.) Another tokenized U.S. Treasury fund, OUSG, is mainly aimed at institutional investors, with a minimum investment amount of 100,000 USDC, with the aim of providing a liquidity exposure to short-term U.S. Treasury bond ETFs. Since its issuance in February 2023, as the proceeds are realized, the price of its token has continued to rise. As of November 10, 2024, the price of 1 OUSG is $108.7626, with an annualized yield of 4.71%, and a total locked value of approximately $200.71 million.

C. Provide financing for real-world assets (RWA) through DeFi lending and realize on-chain income in real-world payment scenarios. Representative project: Huma Finance.

Huma Finance

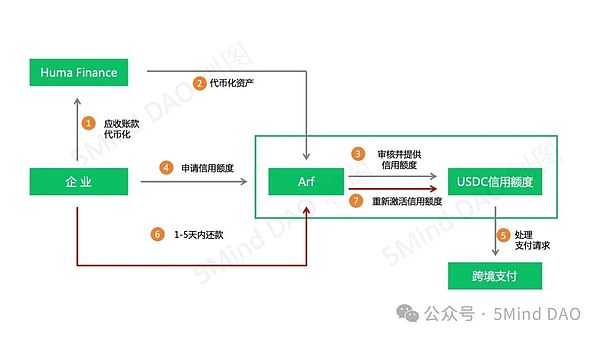

Huma Finance is an income-based lending protocol that allows borrowers to pledge [future income] for lending by matching with global on-chain investors, and provides the function of accounts receivable acquisition (accounts receivable are customer bonds generated by the sale of goods or provision of services during the operation of an enterprise, representing the future cash flow income of the enterprise). In April this year, Huma acquired Arf, a liquidity and settlement platform. Huma's RWA tokenization technology combined with Arf's liquidity solution has created a completely transparent and traceable cross-border payment system on the blockchain.

Through Huma's technology, companies can tokenize assets such as accounts receivable. These tokens can not only circulate on the platform to improve asset liquidity, but can also be used as collateral to apply for a USDC credit line from Arf. When a company receives a cross-border payment request, it can use the USDC credit line provided by Arf for instant payment without locking funds in advance. After completing the payment, the company must repay the used credit line and related fees within 1 to 5 days. Once the repayment is completed, the credit line will be reactivated, enabling the company to continue to process future cross-border payment requests.

According to Richard Liu, founder of Huma Finance, Arf mainly provides short-term loans to licensed financial institutions around the world. Currently, Arf's bad debt rate is 0, and its institutional lending can generate an annualized return of 20%, while the cost of obtaining funds is about 12% to 13%. Therefore, Arf can provide investors with a low-risk return of more than 10%, which is about 7% higher than the return of US bonds. At the same time, Arf itself can maintain a gross profit of 8% to 10%. After merging with Arf, Huma is responsible for the user's deposit part, and Arf is responsible for lending to the Web2 world + collecting interest, forming a sustainable cycle.

In September this year, Huma announced that it had received $38 million in investment to expand its RWA-based PayFi platform. According to data disclosed by the media, Huma Finance's payment financing transaction volume has exceeded $2 billion, with a monthly growth rate of 10%, and has achieved zero credit defaults, with about $500 million in new demand waiting to be met each month.

D. New Web3 payment innovation business that seamlessly integrates with the DeFi protocol. Here are mainly listed the income reflow payment incentives represented by SOEX and DePlan, which introduces economic efficiency into subscription payments.

SOEX

SOEX is a cryptocurrency trading aggregation tool that combines social functions with professional trading, allowing users to tokenize their trading behaviors (mainly spot trading) in various exchanges (currently mainly CEX) to obtain incentives and support the value capture and redistribution of the Web3 social ecosystem.

Generally speaking, trading behaviors in Web3 mainly occur in centralized exchanges (such as Binance, OKX) and decentralized exchanges (such as Uniswap). In this process, the exchange will charge a certain transaction fee, which is also one of the main ways for the exchange to make a profit. In a decentralized exchange (DEX), users can get a certain transaction fee in return by providing liquidity (such as USDT/USDC). However, in centralized exchanges (CEX), users cannot directly provide liquidity to earn transaction fees like in DEX (in CEX, the role and profit-making methods of liquidity providers are usually controlled and managed by the exchange, which is significantly different from the mechanism of DEX).

In order to attract users to participate in transactions, increase trading volume or provide liquidity, CEX usually provides different types of incentives to attract users, but this usually requires high trading volume or institutional users, and most retail investors have little chance to participate. SOEX aggregates small trading behaviors of multiple users in a social way, obtains and optimizes the exchange's rebates, and then distributes these rebates to users based on their contribution (percentage of total transaction volume).

DePlan

DePlan is a consumer application based on the Solana blockchain that allows users to monetize unused subscription time. DePlan enables users to earn income from subscriptions by renting out unused subscriptions to others, and provides flexible pay-as-you-go options for users who need to use the service temporarily.

Under the traditional subscription system, consumers need to pay a monthly fee to use the subscription content, but in reality, there are often cases where users rarely use or even do not use the subscription after subscribing, resulting in a waste of resources. DePlan introduces a new way. By tracking the user's screen usage time, DePlan can determine the unused time of each app subscription and tokenize it on the blockchain (each token represents 1 hour of unused app time). Users can put these tokens on the DePlan market for other users to rent. At the same time, users who need temporary access to the application only need to pay for the length of time they use, without having to commit to a full subscription.

It is understood that DePlan's hourly price is obtained by dividing the ideal subscription fee by the total number of hours of monthly use of the smartphone to ensure that the price paid by the user is proportional to their actual usage. At the same time, the actual price will be adjusted dynamically according to the supply and demand relationship to ensure that both buyers and sellers enjoy a fair market price.

PayFi's Future Vision

PayFi brings greater imagination space to Web3 payments, which includes Web3 payment innovations that integrate DeFi, and Web3 transformations of traditional financial systems, payment systems, and payment business logic, and we have only seen the tip of the iceberg.

Pull your eyes to the entire market. At present, Web3 payments mainly rely on instant fund exchange, that is, the "one hand for money and one hand for goods" model. Although on-chain lending is relatively mature, considering the user's ability to pay, it also adopts an over-collateralized model. In the traditional centralized financial system, in addition to the most common cash transactions, there are also various credit-based payment methods such as credit cards, credit loans, and installment payments. In the future, whether there will be an on-chain credit system to further promote the development of PayFi, we don't know, but now there are projects such as PolyFlow that have begun to explore these areas.

Previously, Lily Liu also mentioned Buy Now Pay Later in her sharing, which can be transformed into Buy Now Pay Never through PayFi. Its core is to use DeFi's income to cover the payment fees, such as Ether.Fi's Cash business.

Ether.Fi is an innovative project in the DeFi ecosystem that focuses on Ethereum staking (locking assets in a specific protocol and obtaining certain income) and liquidity re-staking (reusing already pledged assets for other protocols or networks to enhance their capital efficiency or increase additional rewards), enabling users to earn staking income while maintaining asset liquidity. The Cash business of Ether.Fi is essentially the most common Crypto Payment Card business. That is, users use cryptocurrency to pay, connect with traditional payment channels through currency acceptors, and realize legal currency settlement with merchants. The Cash business of Ether.Fi can be directly combined with its pledge/pledge business to form the characteristics of PayFi, using Ether.Fi's assets as collateral in exchange for USDC for consumption, and repaying with the income from pledge (Stake) and liquidity pledge (Liquid).

After deep integration with DeFi, PayFi will no longer be limited to the payment function itself. In the future, users can enjoy financial product services such as lending, investment, and insurance while making payments, or combine with AI to recommend the most suitable financial products and payment methods for users, which will gradually become a reality.

PayFi's development path

This picture intuitively reflects the significance of PayFi's existence and its relationship with relevant participants. It can be seen that Compared with DeFi, PayFi has a wider range of inclusiveness. It is not only a financial tool, but also a payment bridge connecting traditional finance and the Web3 world. Because of this, there is a big difference between the development path of PayFi and DeFi, especially in the early construction, PayFi's development depends more on the improvement of infrastructure and the leading role of industry institutions. In other words, DeFi's innovation has laid the foundation for PayFi.

From the development context of DeFi. Attracted by the high returns of DeFi, most of the participants in the first wave of DeFi were individuals trying to master the power of this new technology (the iconic innovation of DeFi 1.0 is that individual users participate in liquidity provision through the automated market maker (AMM) model to obtain rewards). However, this way of relying on external liquidity providers is not stable, especially since users are mainly attracted by high returns. When the rewards end or are transferred to other more attractive projects, liquidity will quickly drain away, affecting the development of the entire project. In order to deal with this problem, DeFi 2.0 began to transfer the control of liquidity providers from retail investors to project parties, that is, led by enterprises or institutions, and achieved ecological stability through centralized liquidity control. The emergence of DeFi 3.0 is to allow more ordinary users, especially retail investors who lack knowledge of DeFi, to have the opportunity to easily participate in DeFi without having to deeply understand complex operations or technologies. Since then, DeFi has entered a stage of parallel development for individuals, enterprises, and institutions, with both project parties leading and innovative models that simplify operations, making DeFi more popular.

However, the development of PayFi is quite different. Due to its reliance on infrastructure (such as payment networks, compliance systems, basic chains, etc.), PayFi's early construction needs to rely on large enterprises, financial institutions or infrastructure providers to build technical frameworks and solutions. Individual users cannot directly participate in it. The operation of the entire ecosystem needs to be led by institutions with technology and resources in the industry. As the infrastructure gradually improves, more and more enterprises and institutions will begin to participate, using existing systems and technologies for integration and providing more diversified services. The participation of various enterprises and institutions makes the ecosystem more complete, but it is still dominated by enterprises and institutions, and the participation of ordinary users is relatively low. After the infrastructure matures, individual users can begin to access and participate in the PayFi ecosystem, and drive more people into payment and financial innovation scenarios. In this process, how to maintain decentralization and compliance of the payment system, and ensure security and privacy protection will become one of the key factors affecting the development of PayFi.

Challenges facing PayFi

Broad prospects and numerous challenges, this is the true portrayal of PayFi at present. As an emerging payment technology, PayFi faces a series of challenges and risks in its development, especially in terms of regulatory compliance, user acceptance, technological development and network effects.

1. Regulatory and compliance issues

Due to the involvement of cryptocurrency and blockchain technology, it is currently still in the gray area of existing regulations. In addition, the regulatory policies of various countries on cryptocurrency vary greatly, and the regulatory framework is not yet fully mature. These factors pose major challenges to the widespread application of PayFi.

Global regulatory differences:Different countries have very different regulatory attitudes towards crypto assets and Web3 payments. For example, in some countries (such as the United States and the European Union), cryptocurrencies and DeFi may face strict compliance requirements, while other countries (such as China, India, etc.) may implement comprehensive bans or strict regulatory measures. This uncertainty poses a great risk to PayFi's cross-border payments and global expansion.

Anti-Money Laundering (AML) and Customer Identity Verification (KYC) Requirements:In order to comply with the anti-money laundering regulations and customer identity verification requirements of various countries, the PayFi platform must conduct strict identity verification and transaction monitoring. This not only increases operating costs, but may also affect users' privacy protection and usage experience, especially in decentralized systems, where privacy protection should be a priority.

Tax compliance issues:PayFi's transactions span traditional financial systems and crypto systems, and may face complex tax treatment issues, especially how to define the tax status of crypto assets and transaction tax rules. For example, some countries have unclear regulations on income tax for crypto transactions, which poses a considerable compliance risk to the PayFi platform and its users.

2. User Acceptance and Education

The popularity of PayFi depends on user acceptance, especially for users with non-technical backgrounds, it may be a long process to understand and accept PayFi, an emerging payment technology. User education is crucial to achieve broad market penetration.

Cognitive bias towards cryptocurrency:Many users still have doubts about cryptocurrency and blockchain technology, especially about technical security, volatility, privacy protection and other issues. As a decentralized payment technology, PayFi has a relatively high threshold for understanding, and ordinary users may not understand or trust its potential and advantages.

Complex operation process:For ordinary consumers, PayFi's operation process may be complicated. Users need to understand how to use a crypto wallet, how to conduct transactions, how to handle private keys, etc. This threshold may lead to the loss of potential users, especially in payment scenarios, where users prefer simple and intuitive payment tools.

Education and training costs:Promoting PayFi is not just a matter of marketing, but also requires large-scale user education. To change users' payment habits and cognition, the PayFi project needs to invest a lot of resources in education and training, such as online tutorials, training videos, community interactions, etc., which will directly affect the promotion cost.

3. Technology and network effects

As a blockchain-based payment technology, PayFi faces many challenges such as technical scalability, network effects, and compatibility with the existing financial system. Without sufficient technical support and network effects, PayFi may not be able to attract enough users and merchants, resulting in slow market penetration.

Scalability issues of blockchain technology:Currently, many blockchain networks (such as Bitcoin and Ethereum) still have bottlenecks in transaction speed and processing power, and cannot meet large-scale, high-frequency payment needs. Even more efficient blockchain platforms like Solana and Polygon face the risk of performance degradation when faced with extremely large transaction volumes.

Lack of network effects: PayFi's development cannot be separated from the participation of a wide range of users and merchants, but in the early stages of the market, there may be a "chicken and egg" problem: without enough merchants and users, the platform's attractiveness will be limited, and merchants will hesitate to join due to the lack of a sufficient user base. This vicious cycle may lead to the lack of network effects, which in turn limits PayFi's market penetration.

Compatibility issues with traditional financial systems: PayFi's compatibility with existing payment systems (such as credit cards, bank transfers, etc.) is also a challenge. Many merchants and consumers are accustomed to traditional payment methods, and the widespread use of PayFi requires seamless integration with existing payment systems, which requires not only technical support but also cooperation with traditional financial institutions.

4. Security issues

In the field of PayFi, security issues are particularly important, involving the security of users' funds, transaction privacy and the technical stability of the platform. Hacker attacks (so far, hacker attacks are still a major security risk in the field of blockchain and cryptocurrency), protocol vulnerabilities (security flaws in the underlying blockchain protocol or payment protocol, which usually stem from errors in system design, development implementation or operation, and may lead to theft of funds, leakage of user data or malicious use of the protocol) and other security risks are one of the main risks it faces.

Therefore, PayFi projects usually need to ensure the security of the platform and user funds through multiple security strategies, technical audits and compliance measures. Although it is almost impossible to completely eliminate all security risks, through technical optimization and continuous strengthening of security protection, PayFi can reduce risks while improving its market competitiveness.

PayFi's potential investment opportunities and growth points

The investment opportunities in the PayFi track are mainly concentrated in improving payment efficiency, reducing costs, promoting financial inclusion, exploring new business models and enhancing the diversity of payment scenarios.You can focus on the following key areas:

First, payment infrastructure projects, especially cross-border payment and clearing layer innovations, which will improve the efficiency of payment settlement, such as stablecoin issuers and Web3 payment platforms.

Second, the application of Layer 2 expansion solutions in high-frequency payment scenarios can solve the limitations of existing Layer 1 blockchains in the payment field.

In addition, the combination of decentralized finance DeFi and payment applications, especially innovations in credit lending, stablecoins and payment circulation, also brings new investment opportunities. As a derivative scenario of DeFi, PayFi may provide automated payment solutions through smart contracts, which is worth further exploration.

Payment intermediaries and cross-border payment solutions are also evolving, providing more convenient settlement channels and innovative payment methods. With the rise of the PayFi sector, compliance issues are becoming increasingly important, so the development of compliant contract platforms, KYC/AML solutions, and compliant stablecoins are also key investment opportunities.

Finally, as Web3 payment applications continue to gain popularity, paying attention to the platform's user growth, market share, and community activity can help identify potential projects. At the same time, monitoring market demand changes and technology trends, especially in encrypted payments, tokenized assets, and cross-chain interoperability, can also help discover projects that can solve the pain points of existing payment systems.

Conclusion

This article systematically analyzes the concept and market potential of the emerging field of PayFi. Through practical cases, PayFi's typical application scenarios, market demand and development path are demonstrated. At the same time, its challenges in regulatory compliance, user acceptance, technical scalability and security are analyzed. Investment opportunities in payment infrastructure construction and innovative business models are proposed, and its potential to become a key infrastructure for the future digital economy is envisioned.

Elon Musk has made a bold prediction, foreseeing that advancements in AI will surpass the capabilities of even the most intelligent humans by 2025.

CatherineThe Philippines SEC's ban on Binance raises concerns among investors, highlighting compliance issues and the SEC's commitment to protecting investors.

Miyuki

MiyukiUbisoft unveils its groundbreaking Web3 game, Champions Tactics, amidst growing anticipation. Despite delays in the scheduled mint for The Warlords of Champions Tactics NFT collection, recent developments, including sneak peeks and strategic partnerships, signal a promising future for the game

Alex

AlexThe issuance of a Wells Notice by the SEC to Uniswap Labs has sparked a unified response from the crypto community, rallying in defense of DeFi innovation and decentralised principles.

CatherineIn light of the ongoing congestion on the Solana network, more than 75% of on-chain transactions have been experiencing failures, prompting users to migrate to Ethereum for smoother transfers.

Kikyo

KikyoIn a recent court ruling in Taiwan, it was decided that the assets belonging to David Pan, the founder of Ace Exchange, along with others implicated in the case, will be confiscated.

CatherineGameCene raises $1.4M in seed funding, plans to expand its Web3 gaming platform, offering a diverse game library and empowering developers with its Omni-chain Game SDK.

AlexGameCene 筹集了 140 万美元种子资金,计划扩展其 Web3 游戏平台,提供多样化的游戏库,并通过其 Omni-chain Game SDK 为开发者提供支持。

AlexDisabling automatic media downloads on Telegram Desktop can potentially mitigate the reported vulnerability, although Telegram itself has categorised the threat as likely to be a hoax.

KikyoBinance sees its $4.3 billion settlement with the U.S. as a positive step towards embracing regulation, which the company believes will bring clarity and comfort to users. The exchange is transitioning to a more mature operation under new CEO Richard Teng.

Miyuki