Technical Interpretation of ZetaChain: One-stop multi-chain DAPP underlying facilities

ZetaChain is a POS public chain based on Cosmos SDK. Its blocks record cross-chain messages and data initiated on the "external chain".

JinseFinance

JinseFinance

Author: Bai Ding & Vicent Zhao, Geekweb3

Camus once said in The Plague: "To know a city, one must look at how people work, how they love, and how they die". If one wants to examine the ecology of a public chain, the first thing people look at must be how many DeFi protocols there are, how high the TVL is, and how many application scenarios there are. It can be said that Defi data directly reflects the rise and fall of public chains. Although this set of evaluation criteria has many shortcomings like GDP, it is still regarded as the primary reference framework by observers today.

In terms of business model, modern DeFi is inseparable from the four most basic packages: DEX, lending, stablecoins, and oracles. On this basis, there are also LST, derivatives, etc. These things are commonplace in the EVM ecology, but they are extremely scarce in the BTC ecology. For this reason, countless project parties have emerged under the banner of BTCFi and BTC Layer 2.

But today,BTCFi and BTC Layer 2 have many flaws exposed. Most projects have only built an EVM Chain in the Bitcoin ecosystem, and DAPPs are basically migrated from Ethereum, which seems to have the flavor of using Bitcoin as an Ethereum colony.These EVM Chains are homogenized and involuted, but there is basically nothing refreshing, and no interesting stories to tell.

In comparison, UTXO public chains such as CKB and Cardano may be more attractive than EVM Chain. Previously, Cipher, the founder of RGB++ Layer, proposed the "isomorphic binding" and "Leap bridgeless cross-chain" solutions based on the characteristics of the UTXO model, which once attracted the attention of countless people; the UTXOSwap that combines Intent and is friendly to order books, the ccBTC based on equal collateral, and the JoyID wallet that adapts to multi-chain support Passkey technology are obviously also remarkable.

However, for CKB and RGB++ Layer ecology, a major focus is on its stablecoin system. As the hub in various Defi scenarios, whether there is a robust and reliable stablecoin issuance protocol will directly affect the ecological structure. In addition, whether a suitable circulation environment can be provided for stablecoins is also very important. For example, USDT was first issued with the help of Bitcoin's Omni Layer protocol, but due to the poor smart contract environment provided by Omni Layer, USDT eventually abandoned Omni Layer, which shows that stablecoins are only most suitable for circulation in a perfect smart contract environment.

(Image source: Wikipedia)

In this regard, the RGB++ Layer based on CKB, with its Turing-complete smart contract environment and peripheral facilities such as native AA, can create an excellent circulation environment for the stablecoins of the BTCFi ecosystem. In addition, since many large users are accustomed to holding BTC for a long time rather than interacting with it frequently, if stablecoins can be issued using BTC as collateral while ensuring security, it can leverage the enthusiasm of large users to interact with BTCFi, improve the capital utilization rate of BTC, and reduce people's dependence on centralized stablecoins.

In the following, we will explain the stablecoin protocol Stable++ in the RGB++ Layer ecosystem. The protocol uses BTC and CKB as collateral to generate RUSD stablecoins. Combined with the Stability Pool insurance pool and bad debt redistribution mechanism, it can provide a reliable stablecoin minting scenario for BTC and CKB holders. Combined with CKB's unique issuance method, Stable++ can build an underdamped system in the RGB++ ecosystem, which plays a moderate buffering role when the market fluctuates violently.

Stable++ product function and mechanism design

From the working principle point of view, there are basically four common stablecoins:

Purely centralized stablecoins represented by USDT/USDC;

Stablecoins that require collateral, represented by MakerDAO, Undo, etc. (both purely centralized and decentralized, but with similar mechanisms);

CeDefi stablecoins represented by USDe (value is anchored through derivative contracts in CEX);

(Source: The Block)

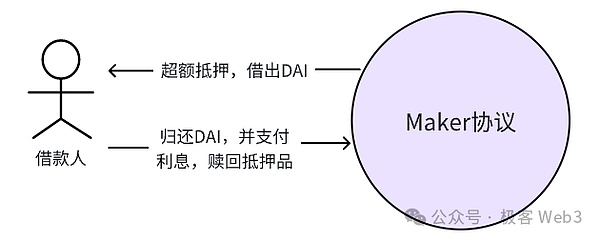

MakerDAO is the representative of the CDP model stablecoin protocol. The so-called CDP is a debt-collateralized position, that is, over-collateralizing blue-chip assets such as ETH and BTC to mint stablecoins. Since the consensus of blue-chip assets is strong and the price volatility is relatively low, the stablecoins issued based on them are more resistant to risks. The lending protocol under the CDP model is similar to the "peer-to-pool" of AMM, and all user actions interact with the capital pool.

Here we take MakerDAO as an example. The borrower first opens a position on Maker, specifies the amount of DAI he wants to generate from the CDP, and then overcollateralizes and borrows DAI. When the borrower repays the loan, he returns the borrowed DAI to the Maker platform, redeems the collateral, and pays interest based on the amount and time of the DAI he borrowed. The interest on the loan here can only be paid with MKR, which is one of the sources of income for MakerDAO.

(CDP peer-to-pool lending diagram)

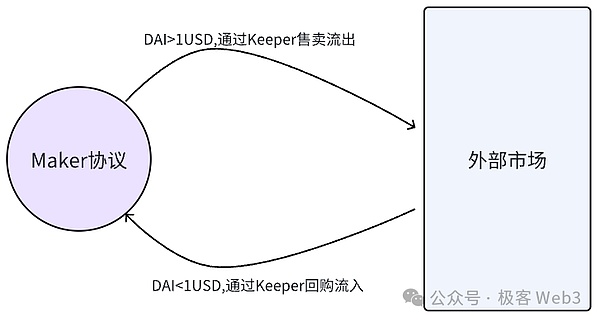

The price anchoring mechanism of DAI relies on "Keeper". We can simply regard the total amount of DAI as constant and composed of two parts: DAI in the MakerDAO fund pool and DAI circulating in the market outside the platform. Keeper will arbitrage between the two fund pools mentioned above to maintain the stability of DAI price. As shown in the figure below:

(DAI anchoring mechanism diagram)

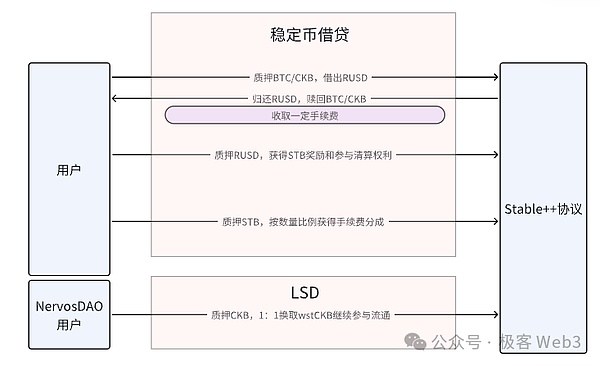

The protagonist of this article, Stable++, also uses CDP in mechanism design, and inherits the security of Bitcoin by borrowing the technology of RGB++ isomorphic binding. From the perspective of product functions, the functions of Stable++ can be divided into several parts:

1. In Stable++, users can borrow stablecoin RUSD by over-collateralizing BTC or CKB, and redeem their own BTC or CKB with RUSD. Fees will be charged for collateral and redemption operations;

2. Users can pledge the borrowed RUSD back to Stable++ to obtain Stable++'s governance token STB as a reward, and at the same time obtain the right to participate in asset liquidation. This is the main deflation scenario of RUSD, and those who have been exposed to Ethena (USDe) must be familiar with this gameplay. In addition, you can also pledge the governance token STB back to Stable++. If you do so, you can get a certain share of the fees from people pledging and redeeming the collateral according to the weight of the pledged STB; 3. RUSD supports homogeneous binding and Leap functions. Through Leap, you can transfer the RUSD controlled by the BTC account to someone else's Cardano account. This does not require the intervention of traditional cross-chain bridges, the security risk is very low and the process is very simple; 4. Stable++ has an LSD section, and NervosDAO users can pledge CKB to Stable++ in exchange for wstCKB. Here is an explanation. NervosDAO is an important part of the CKB ecosystem, which encourages people to pledge CKB for a long time with certain rewards. Now through the combination with Stable++, NervosDAO users can pledge CKB to get rewards, and the liquidity of assets is not lost.

(Stable++ product function diagram)

These functions are easy to understand and need not be elaborated. However, we must know that the key to the success of a CDP stablecoin protocol depends on the following aspects:

The reliability of the collateral

The efficient liquidation mechanism

Whether it can empower the ecosystem

Next, we will focus on the liquidation mechanism and analyze the specific design of Stable++.

Reasonableness and efficiency of the liquidation mechanism

It can be said that the liquidation component is the key gate for the normal operation of the lending protocol. Stable++ has made certain innovations in the design of the liquidation mechanism and avoided the problems in the traditional liquidation mechanism. In the Stable++ system, after the user over-collateralizes the assets to the CDP component to borrow stablecoins, if the value of the collateral decreases and the collateral ratio falls below the threshold, the user will be liquidated if he does not replenish the position in time.

Liquidation aims to ensure that every RUSD in the system has sufficient collateral support to avoid systemic risks.During the liquidation process, the lending platform will withdraw some RUSD from the market, reduce the number of RUSD in circulation, and ultimately ensure that the RUSD issued by the platform has sufficient collateral support.

The liquidation of most lending protocols is carried out in the form of Dutch auctions, and the platform sells the collateral to the highest bidder (ie, the liquidator). For example, assuming that the price of ETH is $4,000 and the collateral ratio of minting DAI is 2:1, the system allows you to mint up to $2,000 of DAI with 1 ETH, but you actually mint 1,000 DAI. After a while, the price of ETH falls below $2,000, and the collateral ratio of the 1,000 DAI you minted is less than 2:1, which will trigger liquidation, and the 1 ETH you mortgaged will be automatically auctioned off.

Dutch auctions start from the highest price and the auction price gradually decreases until there is a buyer willing to take over. Assuming that these collaterals are auctioned at $1,500 and finally handed over to the liquidator for $1,200, the liquidator can obtain the collateral of 1 ETH by delivering 1,200 DAI, and can make a certain profit. After that, the MakerDAO protocol will destroy or lock the 1,200 DAI received, which will reduce the number of DAI in circulation.

The above process can be automatically executed under the control of smart contracts to ensure that the supply of stablecoins in the system is always supported by sufficient collateral and to remove over-leveraged positions. However, in practice, there are two problems with the MakerDAO liquidation mechanism:

1.The auction process takes time. When the market falls sharply, it is possible that bad debts cannot be cleared. The original intention of automatic liquidation is to attract liquidators by selling collateral at a discount and transferring certain benefits. If the value of the collateral continues to fall, the willingness of liquidators will be greatly reduced, and the platform may not be able to find a suitable liquidator.

2. If the network is extremely congested, a large number of operations of individual liquidators are not timely uploaded to the chain, which will also affect the liquidation process.This was verified in the May 19 incident in 2021. At that time, due to the violent market fluctuations and extreme congestion on the chain, many individual liquidators and liquidated persons could not upload their operations to the chain in time.

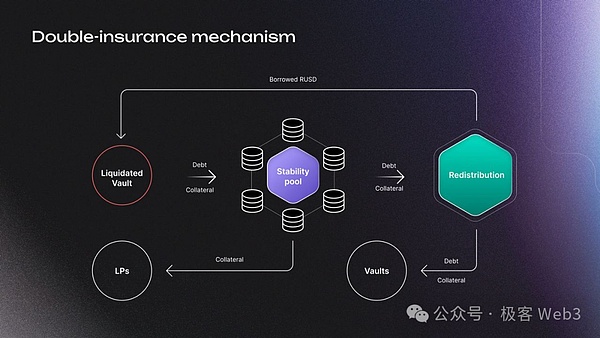

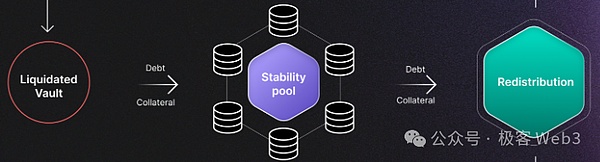

The above problems are reflected in mainstream lending protocols such as MakerDAO and AAVE. They are all due to low liquidation efficiency, which ultimately caused losses to the platform itself and users. In response to this problem, Stable++ tends to ensure the efficiency of the liquidation process as much as possible in the design of the liquidation mechanism, so the double insurance mechanism of "Stability Pool" and "Redistribution" has been added.This is also the biggest highlight of Stable++ in mechanism design.

(Stable++ liquidation mechanism diagram)

In Stable++, users can deposit stablecoins into the Stability Pool (hereinafter referred to as the insurance pool) as a "standing army" ready to liquidate bad positions at any time. When a liquidation event occurs, the first thing the protocol does is to liquidate the bad positions through the insurance pool, and then distribute the collateral to the LP of the insurance pool as a reward. The Stability Pool changes the role of the liquidator from "temporary search" to "standing army", which is equivalent to adding an efficient buffer to the protocol, so there is no need to wait for liquidation to occur and temporarily find a liquidator.

But there are two points to note:

1.The stablecoin currently accepted for injection into the Stability Pool is RUSD itself.Some people may worry: If the reserve assets in the insurance pool are RUSD issued by the platform itself, it seems that there is self-bootstrapping (lifting itself up). Is this reasonable?

On this point, it should be emphasized that RUSD in the insurance pool will be directly destroyed when participating in liquidation.For example: Assuming that the collateral rate of RUSD is 110%, there are 100 RUSD in the Stability Pool from an LP. There is a position with 100 RUSD minted and the collateral value is $109, which has triggered the liquidation condition.

When the position is liquidated, 100 RUSD in the insurance pool are directly destroyed, which means that the LP will lose 100 RUSD, obtain $109 of collateral in the liquidated position, and make a profit of $9. After that, the liquidated person no longer needs to repay the debt of 100 RUSD.

Obviously, 100 RUSD in circulation in the market are destroyed, and the platform also loses $109 of collateral. The bad positions that hit the 110% collateral ratio red line disappear directly, and the collateral ratios of other positions on the platform are still healthy. In this regard, we can summarize the design of Stable++'s insurance pool as follows:

The essence is to let some borrowers lock their RUSD. When a position is liquidated, the platform needs to destroy some RUSD and remove the bad collateral to maintain health. In MakerDAO's liquidation model, the destroyed DAI is provided by random liquidators in the market, while Stable++ directly provides the DAI to be destroyed from the insurance pool. Therefore, for the Stability Pool model, only the stablecoins issued by Stable++ can be used as reserves, without worrying about the bootstrapping problem.

The above example also explains how to calculate the collateral discount rate obtained by the LP of Stability Pool, which is related to the CR set by the system. If we look at the 110% collateral rate in the above case, the LP participating in the liquidation is equivalent to using 100U to obtain 109U of collateral, and the discount rate is about 9%, which is similar to the conventional liquidation discount (this is just a simple example and does not represent the real parameters of Stable++).

However, because Stable++ uses a standing insurance pool, it is much better in liquidation speed and efficiency, and there is no need to temporarily look for liquidators in the market. On the other hand, how to maintain sufficient liquidity in the Stability Pool to deal with liquidation is also an issue that needs to be considered.

2. If the Stability Pool does not have enough stablecoins to participate in the liquidation, then Redistribution will be initiated, and the debt and collateral involved in the liquidated position will be redistributed in proportion among all current positions. For example, when the insurance pool is also unable to handle bad debts, the debt of the bad debt part will become global debt and be distributed to all borrowers. For example:

Now there are 100 borrowers, and a position to be liquidated has 100 RUSD of bad debt. Redistribution will make each borrower bear an additional 1 RUSD of debt, but at the same time, they will also receive a corresponding share of collateral as income. This is different from the redistribution mechanism of old Defi platforms such as Synthetix. Synthetix will only distribute the bad debt to existing borrowers, turning the loan into global debt. Each borrower only bears additional debt without receiving corresponding benefits.

Through the above two insurances, Stable++ ensures that as long as a liquidation event occurs, it can be quickly digested at the first time. This efficient liquidation can effectively solve the bad debt problem in traditional lending agreements. Moreover, this two-pronged and efficient liquidation method means that Stable++ can allow users to borrow at a lower collateral rate (for example, within 110%), greatly improving the utilization rate of funds.

In summary, CDP is essentially a form of lending. Because it is a lending relationship, bad debts will definitely occur, that is, the decline in the value of the collateral leads to the situation of "insolvency", which requires liquidation. In the two liquidation methods discussed below, both parties have their own advantages and disadvantages:

The traditional auction liquidation method, such as MakerDAO and Aave, has been tested for a long time and does not require the maintenance of a huge "insurance mechanism". Usually, large-scale liquidation can be achieved as long as the liquidity of the collateral assets is good enough and the market acceptance is high. However, the disadvantages are the same as mentioned before. It is not efficient in extreme market conditions, and except for a few specific assets such as ETH, the liquidity of other collateral is not high, and there are not enough liquidators to quickly help the protocol return to normal debt levels;

Taking Stable++ and crvUSD as examples, the "liquidation pool" is essentially a protocol-controlled asset pool as a liquidator. By placing reverse orders, liquidation is quickly carried out when liquidation occurs, so that the overall debt level of the protocol reaches a healthy value.It's just that each company has its own advantages in specific practices. What's more interesting is that AAVE's latest Safety module --umbrella also adopts the method of burning instead of selling insurance pool assets to reduce bad debts.

Stabl++ adopts a burning mechanism. The assets in the liquidation pool will be directly destroyed, and the resulting collateral will be directly distributed to the LP of the insurance pool. However, crvUSD is a completely trading idea. During liquidation, crvUSD is used to purchase collateral. After the collateral price rises, these collateral will be sold and crvUSD will be repurchased. The ownership of the entire collateral is in Curve itself.

Can an underdamped system be built within the ecosystem?

First of all, let's discuss what a healthy economic system looks like? One of its necessary conditions is that there must be an "underdamped mechanism" to counter the trend of currency price changes.Underdamping (force) borrows the concept from physics, which refers to a force that "hinders" but is not enough to "stop" the movement trend of an object, which will slow down the trend of the object's change. In token economics, it means that no matter whether the currency price rises or falls, there is a buffer mechanism in the economic system that hinders but cannot prevent its change. Such an economic system can maintain development without over-leveraging, and has the conditions for a soft landing.

Bitcoin's transaction fees and Ethereum's gas fee pricing model will be dynamically adjusted with real-time heat changes. This is a kind of "under-damping mechanism". On the contrary, if an asset rises or falls rapidly, and the system lacks an effective solution to alleviate its changing trend, it is an unhealthy economic system. Such a system will eventually collapse due to over-leveraging. This is also the reason why a number of Ethereum LSD and Restaking projects have been criticized.

Since the collateral supported by Stable++ is mainly BTC and CKB, and it is deployed on the RGB++ Layer, then we have to examine whether the connection between Stable++ and CKB tokens is beneficial to the overall ecology.

In addition to the genesis block, there are two ways to issue CKB. The first is generated by PoW mining, with an upper limit of 33.6 billion. The newly added CKB is halved every four years. The last halving was in 2023, and the annual issuance volume dropped from 4.2 billion to 2.1 billion. This method is called "basic issuance".

In addition, CKB has a unique mechanism, that is, users have to lock some CKB to store data on the chain (you hold assets on the CKB chain, there will be corresponding data to store, and you have to pay a certain storage fee). However, the network does not directly charge storage rent to those who lock CKB, but by issuing CKB, diluting the value of the tokens in the hands of users through inflation, and collecting rent in disguised form, which is called "secondary issuance". The total amount of secondary issuance is fixed at 1.344 billion per year. The distribution of this part of tokens is as follows:

1. Miners:The secondary issuance CKB allocated to miners is proportional to the storage space occupied by users on the chain

2. NervosDAO

3. Treasury:The secondary issuance CKB allocated to the treasury is proportional to the ratio of CKB in circulation to the total issuance, and this part will be directly destroyed

Stable++ allows users to pledge CKB to generate wstCKB, or use CKB to borrow RUSD at a lower collateral rate. When the price of CKB rises, more people will use CKB as collateral to mint RUSD, which can lock up a lot of CKB; and the minted RUSD will increase the activity of the Defi system on the chain. In general, it is equivalent to indirectly reducing the inflation rate of CKB, increasing the activity on the chain, and allowing miners to obtain more benefits, mobilizing their enthusiasm to improve the economic security of the entire network.

So unlike other asset-collateralized stablecoins, Stable++ and CKB's issuance mechanism form a relatively healthy token economic system, which can form an "underdamped mechanism" rather than simply leveraging. With the existing CKB LST, its composability and liquidity will be further improved.

Summary: The necessity of Stable++ from a market perspective

From a market perspective, the BTCfi ecosystem also needs a large-scale decentralized stablecoin to appear.

First, the stablecoins in the current crypto market, USDT and USDC, account for almost 90% of the market value, but their centralization risks are difficult to ignore. As mentioned above, BTCfi users pay the most attention to security. If a decentralized stablecoin that can meet the comprehensive needs of large users for transactions and security appears, it is a necessary condition to leverage these people to participate in BTCFi.

(The top ten stablecoins in current market value)

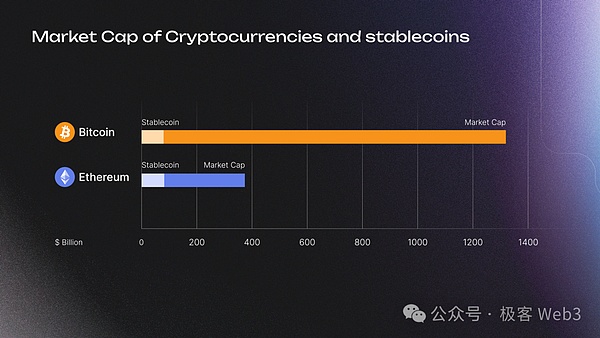

Second, the total market value of stablecoins is about more than 80 billion US dollars, which is only a fraction of the total market value of Bitcoin. From this perspective, there are still many BTCs that can be used as collateral to generate stablecoins, and stablecoins based on BTC still have great development potential.

(Comparison of Bitcoin and Ethereum Market Value)

However, some stablecoins have appeared in the Bitcoin ecosystem before, but they have not caused much response in the market. The reason is that they appeared too early and there was not enough technology to support them at that time. Today, with the growing prosperity of the RGB++ Layer ecosystem and the gradual improvement of projects such as UTXOSwap, Stable++, and JoyID, BTCFi's large infrastructure on CKB has just begun. The stablecoin protocol based on Bitcoin will surely bring new imagination space to the BTCFi ecosystem. CKB, a value depression, will become fertile ground for entrepreneurs, and all visions are expected in the future.

ZetaChain is a POS public chain based on Cosmos SDK. Its blocks record cross-chain messages and data initiated on the "external chain".

JinseFinanceBarkin said he is still not convinced that inflation is in a steady decline and refused to pre-judge the Fed's policy decision in June

Others

Others Coinlive

Coinlive Compute North had filed for Chapter 11 bankruptcy in September.

Crypto Potato

Crypto PotatoLondon -- November 3, 2022 -- Self, the Web3 fraud prevention platform and decentralised trust network, has announced their recent recent beta launch.

Bitcoinist

BitcoinistUnlike most non-fungible tokens, China’s “digital collectibles” are built on closed networks and designed to appease regulators who frown on trading and speculation.

Coindesk

CoindeskWallet manufacturers debated the best ways to store bitcoin private keys safely at the BalticHoneybadger conference in Riga.

Coindesk Beincrypto

BeincryptoUNITBOX protocol, an emerging blockchain startup, introduces its innovative platform where DeFi stakeholders can converge and benefit from the novel ...

BitcoinistMeta’s latest steps into the Metaverse saw the launch of a new marketplace for apps and possibly NFTs which will take a nearly 50% commission on each sale.

Cointelegraph

Cointelegraph