Author: WOO Network

Background

This round of meme coins is the main theme of the market, and there is little interest in DeFi and related "utility" tokens. The current market's overall DeFi lock-up volume is about 182 billion US dollars, which is still about 40% away from the new high of 300 billion US dollars at the end of 2021. This also indirectly proves that the DeFi field has failed to keep up with the pace of the market as the market continues to hit new highs.

However, in the cryptocurrency market, DeFi is one of the few tracks that can generate real returns and is also the cornerstone of overall market liquidity. Although the price of the currency is not as violent as the rising meme currency, the old DeFi blue chips still play an important role in the market. For example, Aave, MakerDAO and Uniswap are the top seven protocols with the overall locked positions, and they are also the absolute leaders of the track.

How do they stand firm in the constantly iterating crypto market? What are the major updates? Is there still growth potential in the future? WOO X Research will answer this in this article.

Aave

Current situation

Aave started as ETHLend in 2017, changed its name to Aave in 2018, deployed the initial version of smart contracts on Ethereum in 2019 and launched Aave V1, launched Aave V2 at the end of 2020, and launched Aave V3 in March 2022.

Aave V3 supports cross-chain lending, improves capital utilization through efficient models, and supports lending of isolated assets. This version can also set upper limits for borrowing and deposits, update the liquidation mechanism, and provide a variety of reward tokens.

The current TVL is 22 billion, which is the second largest locked-in project in the overall crypto market, second only to Lido, and supports 12 blockchains, providing everyone with a permissionless lending platform. It is also the preferred place for whales to use lending to cycle long/short.

In addition to the lending function, Aave also launched its own stablecoin GHO in July 2023, which is an over-collateralized stablecoin. The stabilization mechanism is:

When the GHO price is higher than the hook, users can mint 1 GHO with $1 worth of collateral, and then sell it at a price higher than $1 to make a profit, causing the GHO price to fall back.

When the GHO price is below the peg, users can buy 1 GHO on the market for less than $1 and then use it to repay $1 of debt, which reduces the supply of GHO and increases the price.

In addition, GHO is minted using Aave V3 assets as collateral on the Ethereum market. In addition, Aave stakers (stkAAVE holders) have the following major benefits compared to the general public:

1. Borrowing rate discount: For every 1 stkAAVE staked: a discount on up to 100 GHO borrowed. The discounted borrowing rate will be lower than the standard rate. For example, the standard borrowing rate is 7.25%, while users who stake AAVE enjoy an interest rate of 5.08%.

2. Rewards plan: Users who participate in staking can receive regular rewards through the Merit plan, and the current reward rate is 3.58%.

The current market value of GHO is 102 million US dollars, which is comparable to the market value of crvUSD.

However, good product performance does not mean good coin price performance. The reason is that the $Aave coin price has little to do with the protocol itself. The token is mainly used for governance, and its performance has lagged behind Ethereum in the past year.

Recent updates

On July 25, Aave's official team's governance representative ACI initiated a proposal for Aave's new economic model, which usually has a high chance of passing.

The main content is:

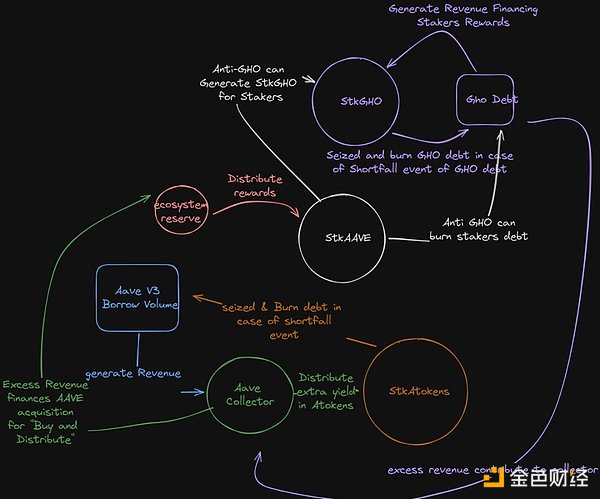

Start Umbrella Atokens security module:

AToken defense mechanism: In the past, Aave's security module was that the pledged assets would be sold to repay debts. Now the approach becomes, adding a new Atoken class to protect assets. In case of shortage, these tokens will be seized to destroy the debt. The collateralized assets will be destroyed instead of sold. This can make the system more efficient.

Incentivizing users to borrow: About 80% of Aave users only deposit funds in the protocol and do not borrow. They are mainly for liquidity benefits and believe that the Aave protocol is safe enough to store assets for a long time. To attract users to borrow, more medium-term rewards are provided to attract these users to participate in the Umbrella security module. The rewards are mainly in their respective aTokens, which are funded by the reserve factor of the relevant assets.

Aave Buyback Program, the operating mechanism is as follows:

Income Generation: Aave V3 lending generates income, which goes to Aave Collector.

Income Distribution: Part of the income is used to purchase AAVE tokens and allocated to the ecosystem reserve. Another part of the income is distributed to StkAtokens holders in the form of Atokens.

Safety: In the event of a shortage of funds, the staked StkAAVE and StkGHO tokens will be seized and destroyed to repay the debt. Anti-GHO provides additional security, generating StkGHO for stakers and destroying the staker's debt when needed.

Reward Distribution: Stakers (such as StkAAVE and StkGHO holders) receive rewards based on their contributions, which are derived from the income generated by the protocol.

This way of operation ensures the stability and security of the Aave protocol while providing users with continuous rewards.

Subsequent impact

The biggest impact is that the performance of the protocol is officially linked to the price of Aave. Whenever a loan occurs, the protocol will automatically purchase Aave in the secondary market, which will undoubtedly inject a shot in the arm for the long-term development of the Aave coin price.

For holders, the launch of the Umbrella Atokens security module and its profit-sharing mechanism can also increase the willingness to pledge and add protection to the security of the protocol.

The current proposal is still in its early stages, and the actual impact on the price of the currency is not immediate. Many adjustments and discussions are still needed, but it is foreseeable that if Tianan passes to make the protocol itself more secure, it will attract more funds into the protocol, and the real income generated will also drive the price of Aave currency.

MakerDAO

Current situation

Created in 2014, the first MakerDAO official white paper was released in December 2017, introducing the original Dai (then Sai) stablecoin system. Given that ETH was the only collateral asset accepted by the system at the time, the generated Dai was called Single Collateral Dai (SCD) or Sai. The white paper also included a plan to upgrade the system to support multiple collateral asset types in addition to ETH. The wish at the time was realized in November 2019.

Currently, Dai is the largest decentralized stablecoin, and the last bear market also introduced U.S. Treasury yields, becoming one of the representative projects of RWA. In terms of internal development, Spark Protocol and Summer.fi were also established, both of which are decentralized lending platforms; the former is a subDAO, and users can use assets such as ETH, stETH, sDAI to obtain DAI loans. The latter is a lending income aggregation platform, where users can amplify the income of existing assets.

It also invested in Multis and Opolis, the former is a Web3 enterprise chain solution, and the latter is a DAO solution.

It can be said that MakerDAO has multiple business tentacles in the currency circle, and it actively seeks opportunities both internally and externally.

MKR, as a governance token, can vote on projects including adjusting the DAI reserve rate, increasing the pool of cryptocurrencies that can be pledged, adjusting risk parameters, etc.

In addition to governance tokens, Maker will also be used to pay stability fees for redeeming assets. When users want to redeem the assets they pledged, they must and can only pay a Maker as a stability fee. The stability fee paid will be used to repurchase Maker on the market and destroyed to maintain scarcity.

In terms of price, due to factors such as the RWA track dividend, the price performance of MKR in the past year is not much different from that of Ethereum.

Recent updates

On May 16, MakerDAO founder Rune Christensen announced on Twitter that a major upgrade of the DAI stablecoin would be carried out because he believed that it was not feasible for DAI to be pegged to the US dollar on a large scale, maintain pure decentralization, and scale up at the same time.

But Rune still hopes for mass adoption and decentralization, and he expects to launch two stablecoins:

NewStable: A stablecoin that meets regulatory requirements

Following the development trajectory of Dai and focusing on practicality and adoption, NewStable is also a decentralized stablecoin that uses decentralization as a means to achieve practical goals by making its governance as resilient and transparent as possible.

NewStable will take over Dai's RWA and tradfi businesses, will continue to be attached to Maker, and will gain Endgame's token economy, growth focus, and governance functions.

Add a freezing function. To ensure that NewStable can safely reach global scale, the freezing function will not be implemented at launch, but the token will be upgradeable so that it can be implemented later through governance voting. As NewStable is adopted by the mass market, this will lead to greater security, stability and reliability of using large-scale RWA collateral.

After an initial transition period after NewStable goes online (currently estimated to be at least 1 year), DSR (DAI deposit rate) will begin to be phased out, gradually reducing the rate over time. Eventually, yield will only be available on NewStable.

PureDai: Fully Decentralized Stablecoin

PureDai will only use purely decentralized collateral, such as ETH and stETH, and will not include more centralized assets such as USDC.

In addition, PureDai has a freely floating benchmark price (not necessarily benchmarked to the US dollar) and is equipped with a maximally decentralized oracle system. This mechanism will never be modified by any organization, including MakerDAO.

In order to minimize the legal compliance risks of PureDai, PureDai will be released in the form of an ultimately immutable contract. Once PureDai is issued, its contract will not need to be further upgraded or changed, and will be completely independent of Maker's control. Once the contract is launched, PureDai will have no relationship with Maker.

Therefore, the contract design of PureDai is very important, and Rune believes that it will take at least a few years to launch.

*NewStable and PureDai can be converted to Dai at any time

(2) On July 17, Rune Christensen, founder of MakerDAO, announced on the social platform that MakerDAO launched the NewGovToken activation function.

When Spark subDAO is launched, NewGovToken holders will be able to activate their NewGovToken to obtain SPK rewards. NewGovToken initiators will receive 15% of all SPK token rewards

NewGovToken can be obtained by converting MKR at a ratio of 1:24,000 and will be launched after Endgame is launched. There is no lock-up period or additional risk for launching NewGovToken, and the activation can be canceled immediately at any time.

(3) On July 13, MakerDAO said on Thursday that it plans to invest $1 billion of its reserves in tokenized U.S. Treasury products. Top players in the field, including BlackRock’s BUIDL, Superstate, and Ondo Finance, have expressed their willingness to actively participate in the plan. MakerDAO’s plan reportedly means a major adjustment to its reserve strategy, in part to support its decentralized stablecoins, which are backed by U.S. government bonds and notes held off-chain by a series of partners.

Subsequent Impact

From the recent development direction of MakerDAO, it can be seen that it is eager to move towards RWA, compliance, and large-scale adoption. The crypto market opened the door to the traditional financial market with the Bitcoin spot ETF at the beginning of the year, but now that the Ethereum ETF has passed, it also proves that crypto assets are increasingly attracting attention and arousing the interest of traditional institutions.

With the upward trend of crypto regulation-friendly, it can be foreseen that the RWA track will still be the key hype track in 2024. MakerDAO, with the RWA narrative dividend and as an old Ethereum project, is still something we can look forward to in terms of currency price performance.

JinseFinance

JinseFinance