ENS incorporates PayPal and Venmo into payment system

PayPal and Venmo's integration with Ethereum Name Service aims to simplify crypto transactions, making them more accessible to users by replacing long wallet addresses with ENS usernames.

Sanya

Sanya

With its stock price down 80% from its pandemic peak and its share of online payments continuing to decline, the fintech pioneer and its newly appointed CEO Alex Chriss are in desperate need of a win.

PayPal is one of Silicon Valley’s oldest and largest fintech companies, and a legendary enterprise whose founders and early employees include Silicon Valley bigwigs such as Elon Musk, Max Levchin, Peter Thiel and Reid Hoffman.

But the past three years have been a difficult time for PayPal: In July 2021, the company hit a record high market value of $360 billion, and its stock price has since fallen, wiping out 80% of its market value, and global e-commerce sales through its PayPal payment buttons have also only fallen instead of rising. In addition, the company’s recent series of attempts to boost its product line have not been taken seriously by analysts.

PayPal CEO Alex Chris.

Image source: PAYPAL

In late January, PayPal held an "Innovation Day" conference, and the new CEO Alex Chris promised to "bring a little shock to the world." Yet a research note from FT Partners captured the reaction: It called the event a “No Innovation Day” and said the so-called “innovation” consisted mostly of bland, repetitive advertising, such as ads in PayPal receipts and Venmo’s social feeds, and a reorganization of PayPal’s in-app cash back offers.

The cynicism from Wall Street is likely to be a harsh reality check for Chris, 46, who became PayPal’s CEO last fall after 19 years at Intuit, where he served as executive vice president of the company’s QuickBooks business. For Chris, being asked to help the 26-year-old San Jose-based company return to its peak doesn’t seem easy.

PayPal declined to make Chris available for an interview with Forbes, but former CEO Dan Schulman did.

Nearly a decade after it was spun off from eBay (which bought PayPal in 2002), PayPal remains profitable, with net income of more than $4 billion in 2023, and its digital financial network of 220 million monthly active users is one of the largest in the world, behind only Apple Pay and Alipay.

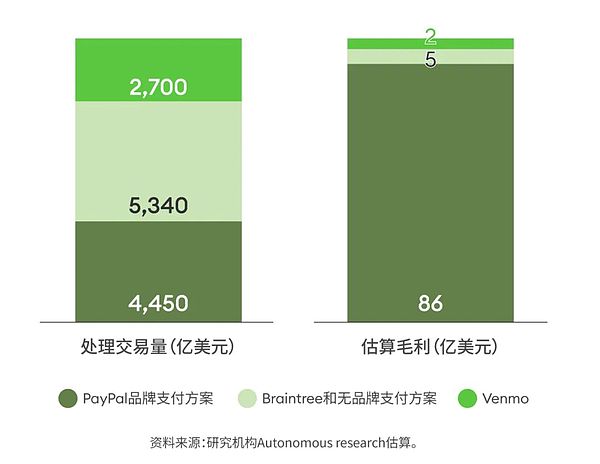

Despite dozens of acquisitions and new business lines, PayPal still makes more than 60% of its $14 billion in gross profits from the PayPal payment button, which people click to pay for items, whether they’re buying baubles on eBay or Etsy or diapers from Target, according to Autonomous Research. Most users still consider PayPal a safer way to pay than to trust a website or person they don’t know. But the pace of transaction growth at the PayPal payment button is slowing—last year, it grew just 7% in dollar terms, while overall e-commerce transactions grew 9%.

With PayPal paying Chris $42 million in compensation through 2023 (part of which is contingent on future performance), he is working to roll out new strategies, including a product called Fastlane that aims to speed customers through checkout. But some analysts are skeptical that the plan can drive profitability and think it may take longer to work than investors expect.

Before Alex Chris took over PayPal, American Express had 1.3 million shares, according to FactSet. Dan Schulman, a former executive at PayPal and former head of PayPal, nearly tripled PayPal's annual revenue to $30 billion during his tenure, and earnings per share rose from less than $1 to $3.85. However, looking back today, some Wall Street analysts point out that Schulman has bitten off more than he can chew. They point out that some acquisitions do not seem to have been effective, such as PayPal's acquisition of Swedish POS checkout equipment company iZettle for $2.2 billion in 2018 and Hyperwallet, which provides payment technology for e-commerce platforms, for $400 million in the same year. In 2020, PayPal acquired a platform called Honey for a high price of $4 billion, designed to help website visitors automatically find coupon codes and cash back offers. Schulman, 66, who owns $40 million worth of PayPal shares, told Forbes that some acquisitions have worked "very well," but others haven't. He added that sometimes acquisitions take a long time to create value, noting that a new ad technology product PayPal recently announced was built on Honey.

Dan Schulman was CEO of PayPal from 2014 to the end of 2023.

IMAGE CREDIT: CHRISTIE HEMM KLOK FOR FORBES

When asked if he had stretched himself too thin in the past, Schulman responded: "Every year we look at what we want to do and try to reduce the amount of tasks rather than increase them. But it's not easy to do that." He added: "Alex Chris has been a standout since he came in. A big part of the reason I left was that I had been there for nearly a decade. You want to have new blood coming in, thinking boldly in different ways, and see if you can add to the original results."

In June 2023, at his last investor conference, Schulman revealed the difficulties PayPal faced in integrating its fragmented payment infrastructure while answering questions from FT Partners' Craig Maurer.

Schulman said he had been working on this problem since he joined PayPal in 2014. But PayPal alone has four different payment stacks, while Venmo and Braintree have their own independent payment platforms. He said: "Eight years ago, we set this goal, which is to integrate all the independent payment platforms into one modern payment platform. But it's like running a marathon and doing a craniotomy at the same time, because what needs to be integrated is our payment processing stack, which cannot be down for a moment."

In Schulman's words, different systems make it difficult to scale efficiently, and a large number of engineers have to focus on solving this problem. “Honestly, it’s been a long, hard process, but we’ve done it,” he added, noting that now that PayPal, Venmo, and Braintree finally have a unified payments platform, the company can “start doing a lot of things that we couldn’t do before with our legacy infrastructure, including interoperability between Venmo and PayPal.”

Essentially, it took PayPal eight years to merge its two systems, and during that time it couldn’t do it on its own technology alone — it still needed a product from Visa called Visa+ to help with the process. “It’s amazing to admit that,” Maurer said. Schulman countered in an interview, saying, “It was a very complex, detailed migration that required building and stress testing every part of the architecture… PayPal wouldn’t have been able to innovate on top of a modern technology stack without all of that hard work that had to be done perfectly.”

PayPal stopped reporting Venmo’s revenue after 2021, when it was about $900 million, which may also suggest that its growth is slowing. Beyond Venmo, integration challenges may help explain why PayPal has struggled to get the most out of more acquisitions.

Meanwhile, PayPal has built a fast-growing business by helping businesses accept online payments with its Braintree technology, competing with fintechs including Stripe and Adyen.

PayPal’s non-branded payment processing unit, much of which is powered by Braintree, completed $534 billion in transactions in 2023 (compared to Stripe’s $1 trillion), up from $299 billion in 2021.

PayPal is in such trouble partly because it has adopted a risky strategy - price war.

Analysts point out that PayPal only charges 0.2% of each transaction as a service fee for non-branded payment transactions (that is, the payment process does not prominently display the PayPal logo, but the payment processing is done in the background, and the checkout process remains on the merchant's website), while in branded transactions (that is, the transaction process will prominently display the PayPal logo and brand), this ratio is as high as 1.5% to 2%. Darrin Peller, managing director of Wolfe Research, said that under the leadership of Alex Chris, PayPal has become less aggressive in pricing. Today, investors are mainly concerned about profitability, which is not Braintree's strong point.

Autonomous Research analyst Ken Suchoski believes Schulman didn’t innovate enough on branded transaction buttons during his tenure. Not surprisingly, Schulman disagrees. He says PayPal has achieved remarkable results in terms of payment speed, transaction clicks, number of features offered and fraud prevention during his tenure as CEO. He also points out that when he took over PayPal’s technology system, it was “ancient” and he oversaw PayPal’s code overhaul, taking it from 200 software updates per year to tens of thousands per year.

Suchoski said PayPal’s share of the $6 trillion global e-commerce market has fallen from a peak of 8% in 2021 to 7% in 2023. Apple Pay, the native payment method on the iPhone, has soared from 0.5% to 3% market share in just five years and may have become the fastest and easiest payment method used by Americans today. Suchowski also said that Shop Pay, the payment app of Canadian e-commerce software Shopify, is well integrated into the former's e-commerce ecosystem and has reached a market share of 1% in the same period.

In earnings calls and interviews, Alex Chris has been calling 2024 a "transition year." "We have a plan to get the company back on track," he said in April. Wall Street analysts have described him as more focused than Schulman.

This is a new product developed under Schulman's leadership that aims to make non-member checkout (that is, checkout on websites where buyers are not registered) faster. The product allows customers who don't use the PayPal button to save their shipping and credit card information so that when they shop again, they only need to enter their email and a verification code sent to their mobile phone to pay.

Chris said 60% of e-commerce transactions are non-member payments, but nearly 50% of these transactions are canceled. But PayPal found that in early cases using Fastlane, 80% of customers who used non-member checkout continued to make purchases.

These statistics sound promising, especially considering that the total addressable market for non-member checkout is in the trillions of dollars. But because the product is a non-branded service for PayPal, it is still unknown how much Chris can charge merchants and how much real profit it will bring. "As we move forward with Fastlane in 2024, we may be very aggressive in pricing because we want to promote this product," Chris said in April. Later, he gave an ambiguous promise about the profitability of the product: "Rest assured, we will price it based on value to ensure that we can get a reasonable return."

Analysts expect PayPal to charge large customers about the same price as Braintree at the beginning, about 0.2% of the transaction amount. Then, it will need to sign up small businesses to charge higher fees on each transaction. Because this feature is not yet popular, and the industry structure is shifting toward larger merchants, analysts at Autonomous and FT Partners believe that Fastlane will take several years to accumulate before it can bring meaningful changes. Maurer said: "I think if they expect Fastlane to have a substantial impact on the holiday sales season in 2024, this idea may be too radical... It will take until the second half of 2025 before we can fully understand whether Fastlane has the energy." Others are more optimistic about this move. For example, Japan's Mizuho Financial Group recently adjusted PayPal's stock rating from "neutral" to "buy". Senior analyst Dan Dolev estimates that PayPal will eventually charge 0.7% of each transaction from Fastlane, and in the next 18 months or so, PayPal will be able to earn an additional $1 billion to $1.5 billion on top of its $14 billion in annual net profit.

Dolev also said he was pleased that the loss of market share for the PayPal button has leveled off, based on Mizuho's study of online transaction volumes at top retailers. "You don't want it to be an ice cube melting in the oven, but the evidence suggests it's more like an ice cube melting in the freezer. That's a more acceptable scenario," he said. In a recent research note, he commented on the apparent plateau: "This probably means that PayPal has survived the worst of the loss of market share to Apple Pay and others, which we can see in the stock price."

More optimistic analysts, including Dolev, estimate that PayPal's gross profit will grow 6% to 7% in 2025 and 2026. Ken Suchowski and others have a different view - they believe that PayPal's gross profit will only grow more slowly, around 3% to 4% over the next two years. Of the 45 analysts covering PayPal, Ken Suchowski is the only one with an "underperform" rating on the stock, according to Bloomberg. (Twenty of the analysts have more neutral ratings on PayPal, such as "neutral," "hold," and "market perform.") Having just one negative analyst may be encouraging, but PayPal's stock performance is no laughing matter—it's down about twice as much as the average publicly traded fintech stock over the past 12 months. Suchowski argues that people who buy shares of payment software companies could get better returns by buying shares of companies like Fiserv and FIS. Both companies trade at similar valuation multiples as PayPal, he says, but don't face the same competitive pressures and are growing revenues by as much as 8% annually. "Basically, you can buy another business for the same price, but their revenue is still growing, and you don't have to face the situation of turning losses into profits like you did with PayPal."

Since earlier this year, Alex Chris seems to have become more conservative - he no longer preaches that PayPal will surprise people. Darin Peller of Wolfe Research said: "He wants to set the bar lower at the beginning and then slowly and steadily raise the bar. This is a better way to increase its stock price."

PayPal and Venmo's integration with Ethereum Name Service aims to simplify crypto transactions, making them more accessible to users by replacing long wallet addresses with ENS usernames.

Sanya JinseFinance

JinseFinanceDiscover how to exchange Bitcoin to PayPal safely using third-party services or peer-to-peer transactions. Learn about popular platforms like Paxful, LocalBitcoins, and CoinPal, each with its features and fees. Explore the advantages and risks of both methods, and get valuable tips to ensure a secure exchange, from researching service providers to using escrow services. Make informed decisions to safeguard your Bitcoin assets when converting to PayPal.

Xu Lin

Xu LinChanges in the regulatory landscape seem to have stalled the project.

CryptoSlate

CryptoSlateCrypto firm ConsenSys is announcing a new partnership with payments giant PayPal to create a convenient way for investors to purchase Ethereum (ETH).

dailyhodl

dailyhodlAccording to a report published by Europol, crypto is one of the main tools used by individuals linked to terrorism financing.

Bitcoinist

BitcoinistThe move comes nearly two years after PayPal allowed users to buy and sell cryptocurrencies on its platform.

Cointelegraph

CointelegraphThe tech giant has hired a PayPal veteran to help with Google Pay's expansion as it looks to the future, including plans to explore cryptocurrencies.

CointelegraphA spokesperson reportedly suggested that the office closures were being made to assess the company's "global office footprint."

CointelegraphA spokesperson reportedly hinted the closure was aimed at the company evaluating its “global office footprint.”

Cointelegraph