Original author: Peter Schroeder

No innovation has captured the imagination and potential of the technology and financial worlds like stablecoins.

Designed to maintain a stable value relative to a reference asset (in most cases a fiat currency like the dollar), these digital currencies have become a bridge between the traditional financial system and blockchain technology.

This week's news of Stripe's acquisition of Bridge sent ripples through the tech world and made people realize the potential of stablecoins to pave new monetary highways.

Let's dive into what stablecoins mean for the future of money.

The Rapid Rise of Stablecoins

There is a saying that the ultimate complexity manifests itself in simplicity.

Despite the complexity that cryptocurrencies sometimes bring, in principle stablecoins are the simplest form - they are digital currencies that combine the advantages of cryptocurrencies with the stability of traditional finance.

Everything will become obvious in hindsight, but we are at a turning point for money.

Stablecoins are not just an improvement on the existing system; they are laying the foundation for an entirely new internet-based financial system.

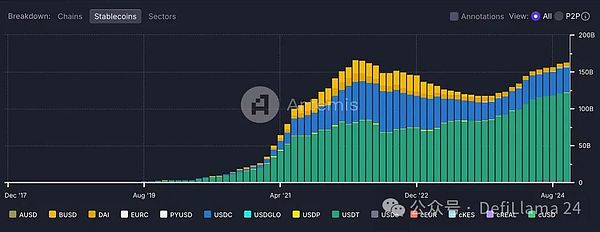

As a result, the market capitalization of fiat-backed stablecoins has swelled from the conceptual stage in 2018 to over $164 billion in October 2024.

To put this into perspective, this is more than the GDP of more than 100 countries.

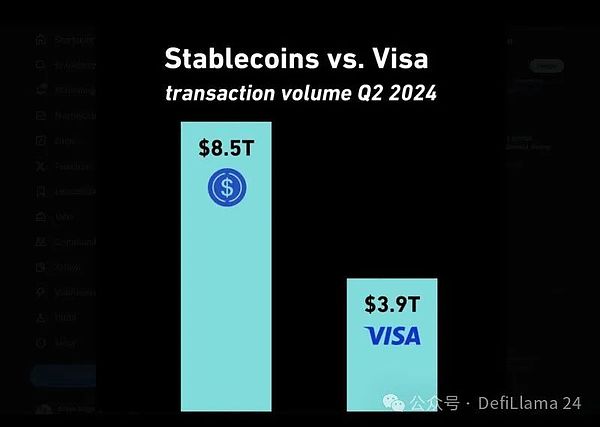

And these stablecoins are not sitting idle. In the second quarter alone, stablecoins processed nearly twice as many transactions as Visa, with monthly transactions regularly exceeding trillions of dollars.

For a technology that was invented only 6 years ago, this level of growth is amazing.

The Business of Stablecoins

Why are stablecoins a good business and how do they make money?

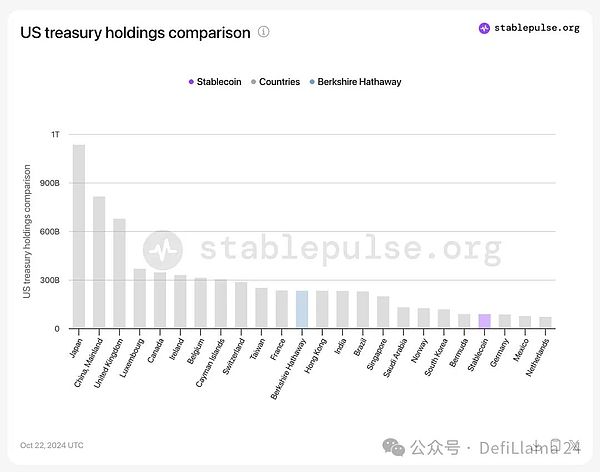

Stablecoins generate income by investing their reserves 1:1 in interest-bearing assets, such as treasury bills and other short-term investment instruments. The interest earned on these investments provides a source of income for stablecoin issuers.

This innovative investment strategy has made stablecoin issuers, in aggregate, one of the largest holders of U.S. Treasuries, with holdings exceeding those of countries like Germany, Mexico, and the Netherlands.

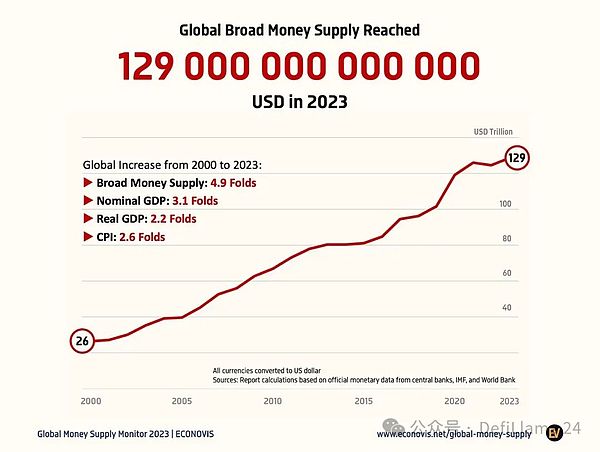

But stablecoins are only beginning to realize their potential. Consider this: Global money supply (M2) is estimated to be around $129 trillion.

We are only just beginning to update the financial system through stablecoins.

Besides M2 money supply, here are some other market sizes that stablecoins are expected to improve:

Foreign Exchange (Forex): $8 trillion moves between different currencies every day. This is the largest market in the world. It is about 30 times the global daily GDP.

Once we have deep liquidity of stablecoins backed by more currencies around the world, digital FX trading through stablecoin swaps will quickly begin to change the way currencies move between each other today.

Global Remittances: In 2023, the value of global remittances is estimated to reach $883 billion, and is expected to reach $913 billion by 2025.

Stablecoins make cross-border payments as easy as sending a text message or email, providing faster, cheaper, and more seamless transactions.

Payments: As of 2023, the global payments market is worth $2.64 trillion and is expected to grow to $4.78 trillion by 2029. Credit card processing fees vary by region, payment method, and transaction type, but generally range from 1.5% to 3.5% of the transaction amount. The average fee for global credit card transaction processing in 2024 was approximately 2.4% of the transaction value.

Stablecoins have the technical ability to simplify the payment process, making it more efficient.

If stablecoins can capture even a small fraction of these outdated markets, trillions of dollars will flow into digital currencies, radically improving the financial system.

The Miracle of Money

Why is Internet-based money so important?

Similar to water, money permeates our society and nourishes economic activity.

It seeks the path of least resistance, just like water flows downwards. Just as water is essential to life, money is the lifeblood of commerce, facilitating transactions and storing value.

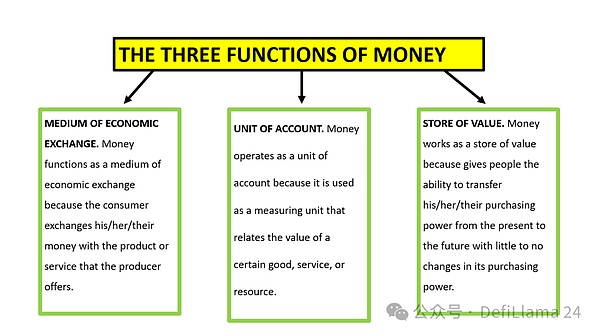

Understanding the basic functions of money itself is important to understanding the value of stablecoins.

Money essentially exists to solve a fundamental problem: how to efficiently exchange value in a complex society. Economists have long recognized three main functions that define money:

1. Store of value

2. Medium of exchange

3. Unit of account

These functions form the foundation of any monetary system, enabling individuals and societies to save, trade, and measure economic value over time.

By design, stablecoins are intended to achieve these same core functions, but in the digital realm, they offer improvements over traditional forms of fiat currency.

Store of Value

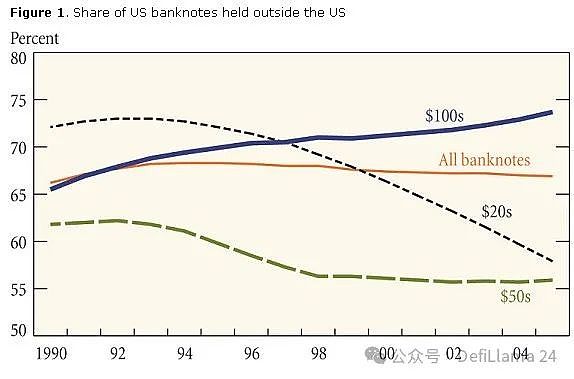

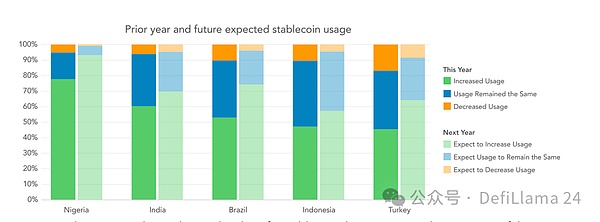

One of the most immediate and obvious use cases for stablecoins is as a store of value, especially in countries with unstable currencies or limited access to the global financial system. For people living in countries with high inflation or strict capital controls, holding stablecoins pegged to the U.S. dollar or euro can be a lifeline to protect their hard-earned capital.

Nearly 75% of physical $100 bills are held overseas, worth more than $1.5 trillion. Now, people can access any amount of dollars or other currencies in digital form 24/7/365 through stablecoins.

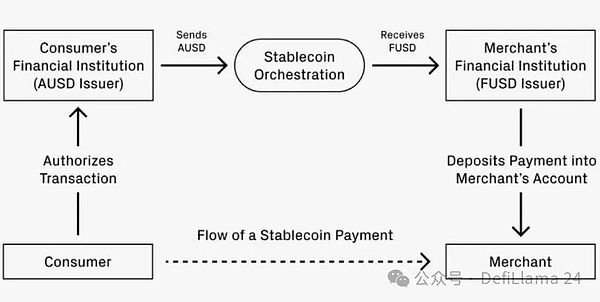

Medium of Exchange

As a medium of exchange, stablecoins have the opportunity to replace existing processes through their efficiency and programmability. In every workflow where there are middlemen facilitating and participating in transactions, stablecoins have the opportunity to abstract and simplify the payment process.

According to McKinsey research, the global payments industry processed 3.4 trillion transactions in 2023, worth $1.8 quadrillion, with a revenue pool of $2.4 trillion. By simplifying these payments, stablecoins are cannibalizing this $2.4 trillion global payment tax, making payments more efficient for everyone.

Stablecoins have already surpassed the trading volume of most cryptocurrencies and will soon dominate other industries as well.

Unit of Account

While stablecoins are already useful as a store of value and medium of exchange, their potential as a unit of account remains largely untapped. As more businesses and individuals become comfortable with stablecoins, we may see them used to price goods and services, especially in an international context.

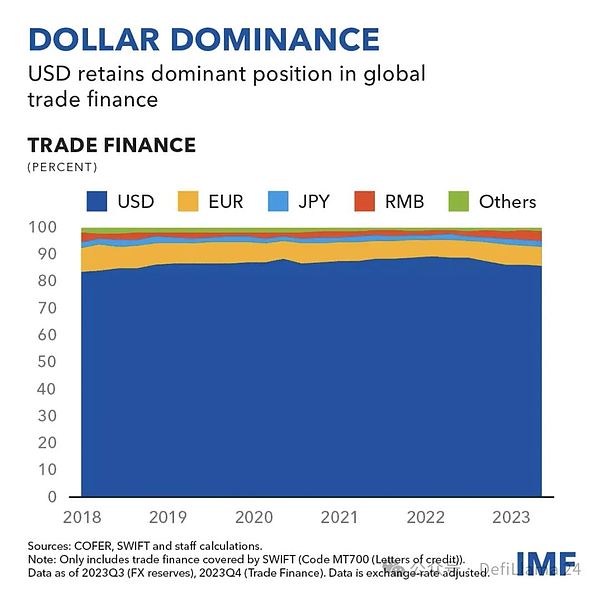

As most goods trade continues to be denominated and settled in dollars, the U.S. dollar accounts for more than 80% of trade finance, according to SWIFT.

The global trade finance market size is valued at $10.5 trillion in 2023 and is expected to reach $13.6 trillion by the end of 2032. The CAGR between 2024 and 2032 is close to 2.94%, which provides a huge opportunity for stablecoin settlement.

In short, stablecoins are still in their early stages.

Better Internet Money

Apps like Venmo and Cash App have revolutionized peer-to-peer payments within the United States, making it simple to split a dinner bill or pay rent.

However, these solutions are largely limited to the country. There is currently no "global Venmo" that enables fast, easy, low-cost international money transfers.

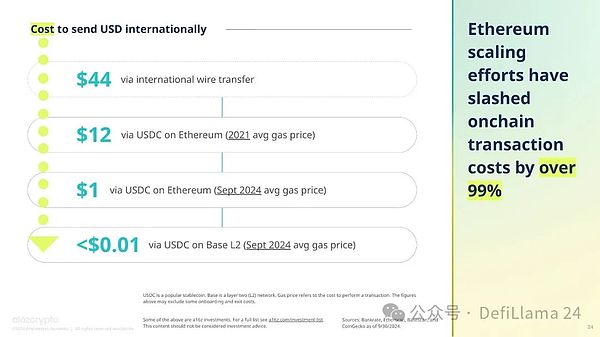

This is where stablecoins shine. They offer an inherently global solution that operates 24/7, unrestricted by national borders or banking hours. With a stablecoin like USDC, sending money anywhere in the world becomes as easy as sending a text message, and the cost is often a fraction of a traditional international wire.

After the Ethereum Dencun upgrade in March, the average transaction cost on L2 networks like Base has dropped to less than $0.01. It's nearly instant and available anywhere in the world.

Coinbase CEO Brian Armstrong recently said at a conference hosted by Goldman Sachs:

I'm happy to report that we have now reduced transaction times to less than one second anywhere in the world and fees to $0.01.

This makes cryptocurrency the best payment channel in the world by far. There are also payment channels in the traditional financial system. Some payment channels are very fast, such as credit cards, but they are expensive and charge 2% fees. Some payment channels are very cheap, such as ACH, but they are very slow.

Two to three business days. Right? Some payment methods are very fast and cheap, such as WeChat Pay, but they are only used in one country, and that is China. Cryptocurrencies, crypto payment rails on layer two networks like Base, are the only ones I know of right now that meet all three of those criteria. They're fast, they're cheap, and they're global.

That's part of why I think we're seeing 200% to 300% year-over-year growth in stablecoin volume. That's really powerful. It's not just unlocking payments, it's actually starting to unlock another class of applications.

So, for example, if you have fast, cheap, and global payments, what might that allow people to do? Maybe, sometimes on social media, people click the like button or give a thumbs up to something. You know, why can't that be a microtransaction? Right? Today in the United States, people get paid every two weeks. Why can't you get paid every hour?

Maybe, the whole concept of payday loans might go away. Right? Or minute-by-minute changes. So if the world had a fast, cheap, global financial system that was decentralized and not controlled by any one country, I think a lot of friction in the economy would be removed and you would see a ton of growth. Even if you remove a small amount of friction, you would see a huge increase in adoption. For example, text messages used to cost $0.25.

At the peak of text messaging, there were about 25 billion text messages a year. Today, with free apps like WhatsApp, iMessage, etc., there are hundreds of billions of messages sent a day. So just by removing a small amount of friction, you can increase activity by an order of magnitude. This has happened in messaging, and now it's going to happen in payments.

To put it more bluntly, stablecoins like USDC on layer 2 networks have become the most efficient payment rails in the world.

Think about this..

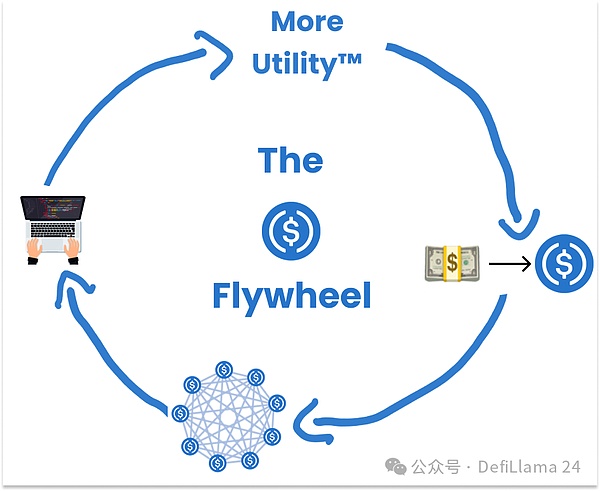

As more applications integrate stablecoin functionality, we may see network effects. Each new application that adopts a stablecoin increases the utility of the entire ecosystem, incentivizing further adoption and innovation.

A network effect is when a product or service increases in value when more people use it. Think of social networks like Facebook or messengers like WhatsApp - their value grows exponentially with each new user that joins.

Stablecoins have the potential to generate extremely powerful network effects.

As more people start using stablecoins, more businesses will accept them, and as more businesses accept them, more people will want to use them.

This virtuous cycle can lead to rapid, widespread adoption that grows at a rapid pace.

The old doesn’t go, the new doesn’t come

When we look at the stablecoin landscape, people often compare it to the early days of the internet. At the time, it was difficult for many people to understand how transformative this technology would be. We are now at a similar stage with stablecoins.

On "The Money Movement" with Jeremy Allaire, Chris Dixon said:

All new technologies generally do two things. They tend to do old things better, and do something new that couldn't be done before. Blockchain is really a new way to build internet services, architected in such a way that there are no gatekeepers or fee collectors.

Stablecoins are a huge opportunity for entrepreneurs, developers, and innovators. The companies and protocols that successfully navigate this space could become the financial giants of the future.

Here is a partial list of companies currently innovating in the stablecoin ecosystem:

The potential is huge. Stablecoins have the power to reshape the financial system in a more open, efficient, and inclusive way.

They could be the key to unlocking global financial inclusion, enabling new business models, and creating a more connected global economy.

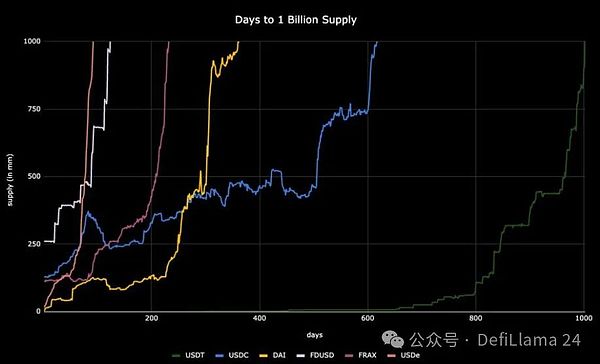

Don’t blink, because this growth is happening fast, with several stablecoins growing to over $1 billion in supply in less than a year.

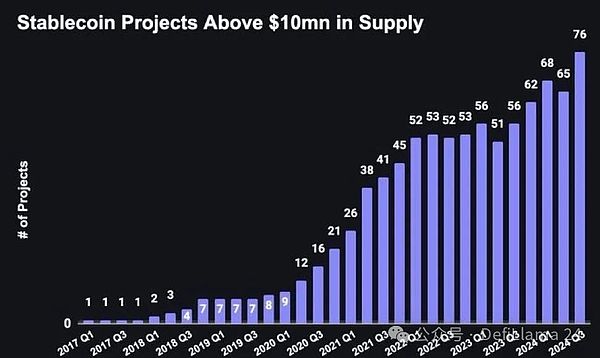

There are now more than 76 stablecoin projects with over $10 million in supply.

The potential for growth isn’t just huge; it’s transformative on a global economic scale. And we are just getting started.

We are standing on the threshold of a new era of finance. The stablecoin revolution has just begun, and I personally can’t wait to see where it takes us.

Until our next adventure.

JinseFinance

JinseFinance