Author: Tanay Ved Source: Coin Metrics Translation: Shan Ouba, Golden Finance

Key Points:

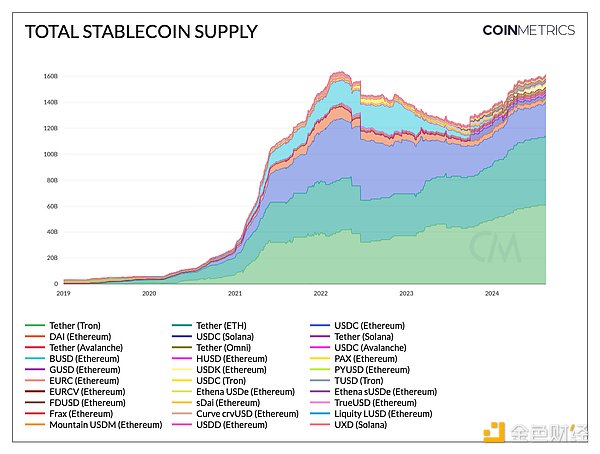

Stablecoin flows have turned positive, with total supply exceeding 160 billion, a record high. This means improved market liquidity and increased capital available for deployment in the crypto ecosystem.

The stablecoin landscape continues to expand in terms of diversity, use cases, and risk profiles, from fiat-collateralized and crypto-backed stablecoins to interest-bearing and protocol-native stablecoins.

As stablecoin collateral increasingly consists of USD equivalents and real-world assets (RWA), changes in the interest rate environment may affect the profitability and attractiveness of various stablecoins.

Introduction

This article explores the diverse stablecoin landscape, focusing on pegging mechanisms, collateral composition methods, and sources of yield in an interest rate environment.

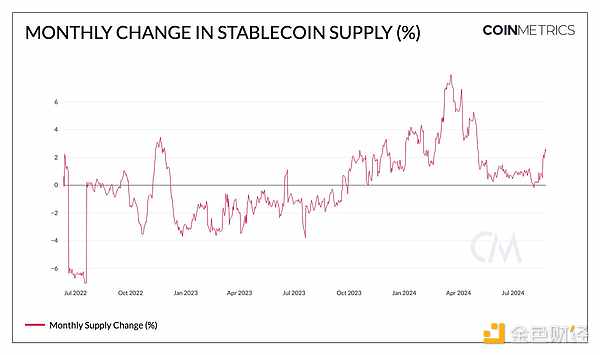

Stablecoin Supply Heading to New Highs

After a period of consolidation in Q2, total stablecoin supply showed a positive growth trend in August, indicating an increase in liquidity and capital inflow potential in the ecosystem. This is reflected in the figure below, which shows the monthly change in stablecoin supply.

Source: Coin Metrics Network Data Pro

Thus, the total supply of stablecoins is close to 1610 USDT on Ethereum (+28%) and Tron (+26%) has grown over the past year, bringing the total supply to $119 billion across networks including Solana and Avalanche. Meanwhile, Circle’s USDC supply has grown to around $34 billion as it surges across Solana and Ethereum Layer 2s like Base. While DAI trended down to $3.1 billion, sDAI (Savings DAI), a tokenized version of Dai deposited with Maker’s Dai Savings Rate, has grown to $1.34 billion.

Newer stablecoin entrants have also gained traction: First Digital USD (FDUSD) on Ethereum grew 56% in August to $3.07 billion, while Ethena’s USDe ($2.96 billion) and sUSDe ($1.16 billion) combined for $4.12 billion. Notably, PayPal’s PYUSD has seen rapid growth on Solana, surpassing its $364 million Ethereum supply to reach a total of $1 billion.

Source: Coin Metrics Network Data Pro

The Battle for Adoption

Diversity of Collateral

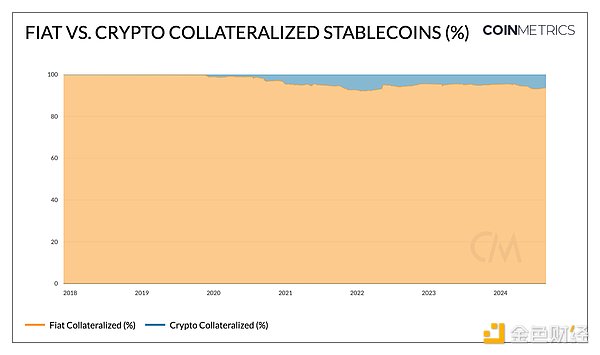

To increase utility as a store of value, a variety of asset compositions, or collateralization methods, have emerged in the stablecoin ecosystem, impacting the risk profile, operational characteristics, and regulatory outlook of these products. More than 90% of outstanding stablecoins are composed of fiat collateral, such as Circle’s USDC, Tether’s USDT, and PayPal’s PYUSD, which are backed by U.S. dollars and cash-equivalent assets, pegging their stability to the traditional financial system.

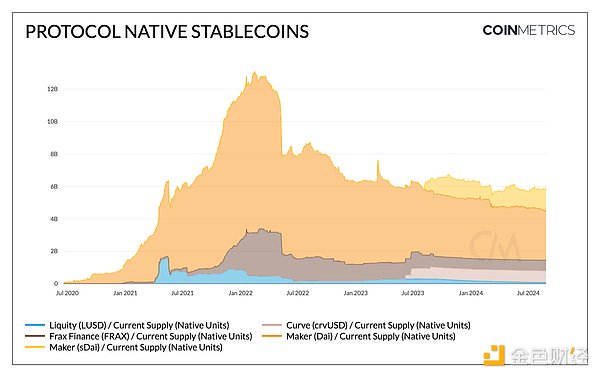

Others, such as MakerDAO’s DAI and sDAI, offer alternatives to traditional units of account, backed by a combination of crypto assets and real-world assets (RWAs), such as private credit loans or Treasury bonds. 45% of Dai is backed by crypto assets, while 40% is collateralized by RWAs.

Source: Coin Metrics Network Data Pro

Alternative Accounting Units

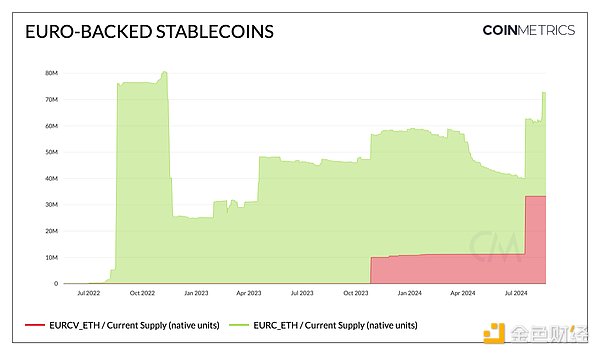

As different jurisdictions develop their own regulatory frameworks for digital assets, stablecoins pegged to local currencies can facilitate transactions for individuals and businesses within and across regional economies while complying with regulatory requirements.

Source: Coin Metrics Network Data Pro

Source: Coin Metrics Network Data Pro

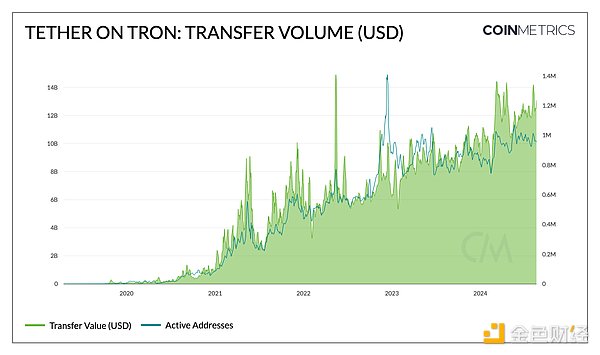

Product Market Fit: Tron Tether on Tron

Tether (USDT) on the Tron network is a prime example of a stablecoin that has established product-market fit. It has demonstrated strong adoption and usage as a medium of exchange and store of value across a range of metrics. Not only does it have the largest supply by far at 118 billion, with ~61 billion on Tron and ~53 billion on Ethereum (in addition to Solana and Avalanche), but it also has the highest transfer volume and volume relative to other stablecoins. Tether’s (adjusted) transfer volume on Tron is approaching a record $14 billion, with nearly 1 million active addresses.

This usage is driven by Tron’s low transaction fees, supporting micropayments and remittances with low median transfer sizes, and USDT’s deep liquidity on exchanges, facilitating trading activity as a quoted asset. As such, it provides the means to protect savings, seek economic stability and democratize access to banking infrastructure, supporting peer-to-peer transactions for a variety of purposes – especially in emerging markets.

Source: Coin Metrics Network Data Pro

Low fees on networks like Solana and Ethereum Layer 2, plus The distribution of businesses like Coinbase and easier onboarding through smart wallets or point-of-sale systems provides stablecoins with an opportunity to build a strong foundation on these networks and around the world.

Stablecoins in a Changing Interest Rate Environment

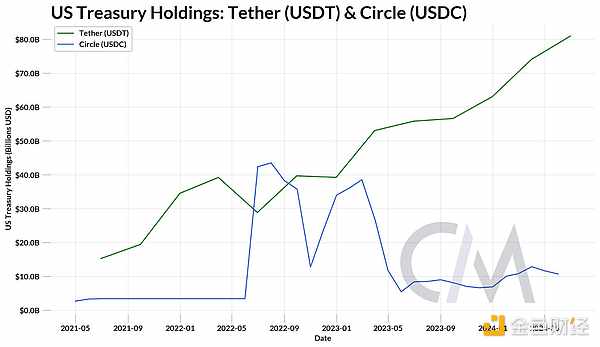

Stablecoins are primarily collateralized by USD or equivalents such as cash or Treasuries. Most traditional stablecoins (e.g. USDT, USDC, PYUSD) retain the interest earned on their collateral rather than passing it on to token holders. Tether’s Q2 proof is an example of this, reporting $5.4 billion in profits, in part from direct and indirect holdings of U.S. Treasuries, which reached a new high of $97.6 billion. This puts their exposure to U.S. Treasuries above Germany, the United Arab Emirates, and Australia — ranking them 18th among countries holding U.S. debt.

Source: Tether & Circle Proof

Where does the income come from?

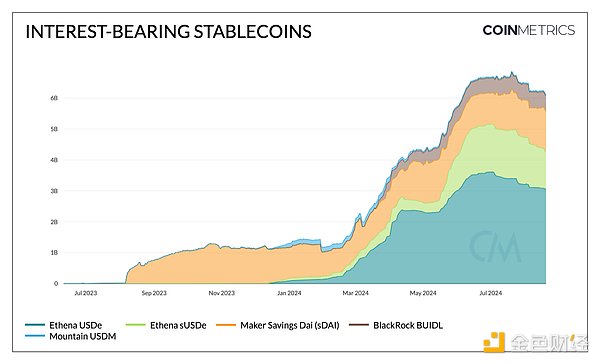

However, the rise in the Fed Funds rate and global interest rates after 2021 has created an opportunity cost for pure USD exposure. This has triggered the emergence of interest-bearing stablecoins that are collateralized by short-term US Treasuries, money market instruments, and other real-world assets (RWAs) and pass the yield to holders.

For example, Mountain Protocol’s USDM’s yield comes from the reserve composition of Treasuries, which generates interest through a rebasing mechanism. Maker Protocol’s Savings DAI (sDAI) takes another approach, accumulating interest on DAI deposited at the DAI Savings Rate (DSR). This yield comes from a basket of real-world assets (RWAs), crypto assets, and excess reserves backing DAI, implemented through the ERC-4626 vault standard. These products essentially act as crypto savings accounts.

RWA's integration with public chains also paves the way for institutional-grade products such as BlackRock's BUIDL, a tokenized money market fund issued by Securitize that uses the USDC redemption fund to provide a 24/7 uninterrupted stablecoin outlet. While tokenized treasury products rely on such off-chain sources of income, others, such as Ethena's USDe, generate income through underlying transactions involving delta-neutral hedging (a long position in ETH or other collateral and a corresponding short position in a perpetual futures contract).

Source: Coin Metrics Network Data Pro

However, Federal Reserve Chairman Jerome Powell said in 2024 The proposed rate cuts at the 2018 Jackson Hole Symposium have raised questions about the relevance of stablecoins in a low-interest rate environment. While fiat-collateralized stablecoin issuers may see reduced profitability due to the interest rate sensitivity of their business models, and yield stablecoins may lose some of their appeal due to diminishing returns, the risk-on environment could bring new capital inflows to the crypto ecosystem. Such inflows, driven by investors seeking to take advantage of lower borrowing costs and higher asset valuations, could offset these effects through increased demand for stablecoins as a medium of exchange.

Conclusion

The recent growth in stablecoin supply and new highs is indicative of increasing liquidity and capital availability in the crypto ecosystem. As the landscape continues to evolve, we have witnessed stablecoins being optimized for different use cases and risk profiles, adopting a variety of collateralization methods from RWAs to crypto assets and innovative approaches such as tokenized base transactions. Looking ahead, navigating regulatory hurdles and a low interest rate environment presents both opportunities and challenges that could reshape the business model, user preferences, and overall competitive landscape of this emerging industry.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

JinseFinance

JinseFinance