FHE vs ZK vs MPC 3つの暗号化技術の違いは?

多くの友人がいまだにFHEをZKやMPC暗号化技術と混同しているので、この記事ではこれら3つの技術を詳細に比較する。

JinseFinance

JinseFinance

Last week, the US Securities and Exchange Commission (SEC) sued both Binance and Coinbase- charging both with operating an unlicensed securities exchange.

But, Binance also has another outstanding lawsuit against it- one from the Commodities and Futures Trading Commission (CFTC) that alleges that Binance operates an illegal digital asset derivatives exchange.

Yet, for many others in the crypto ecosystem, this debate is an example of regulation gone wild- why does it matter if crypto is a security or a commodity? So what if it is one and not the other? And why can’t it just be considered a currency just like the Euro or the Japanese Yen?

The iffy status of cryptocurrency is certainly not one that affects everyday consumers directly- after all, you don't need to know the difference between all of these in order to trade crypto or transact in crypto.

But as regulators close in on exchanges like Binance and Coinbase, this may soon cease to be the case- after all, lawsuits against two of the largest exchanges, each with millions of clients, will be significant for both clients and partners of these exchanges.

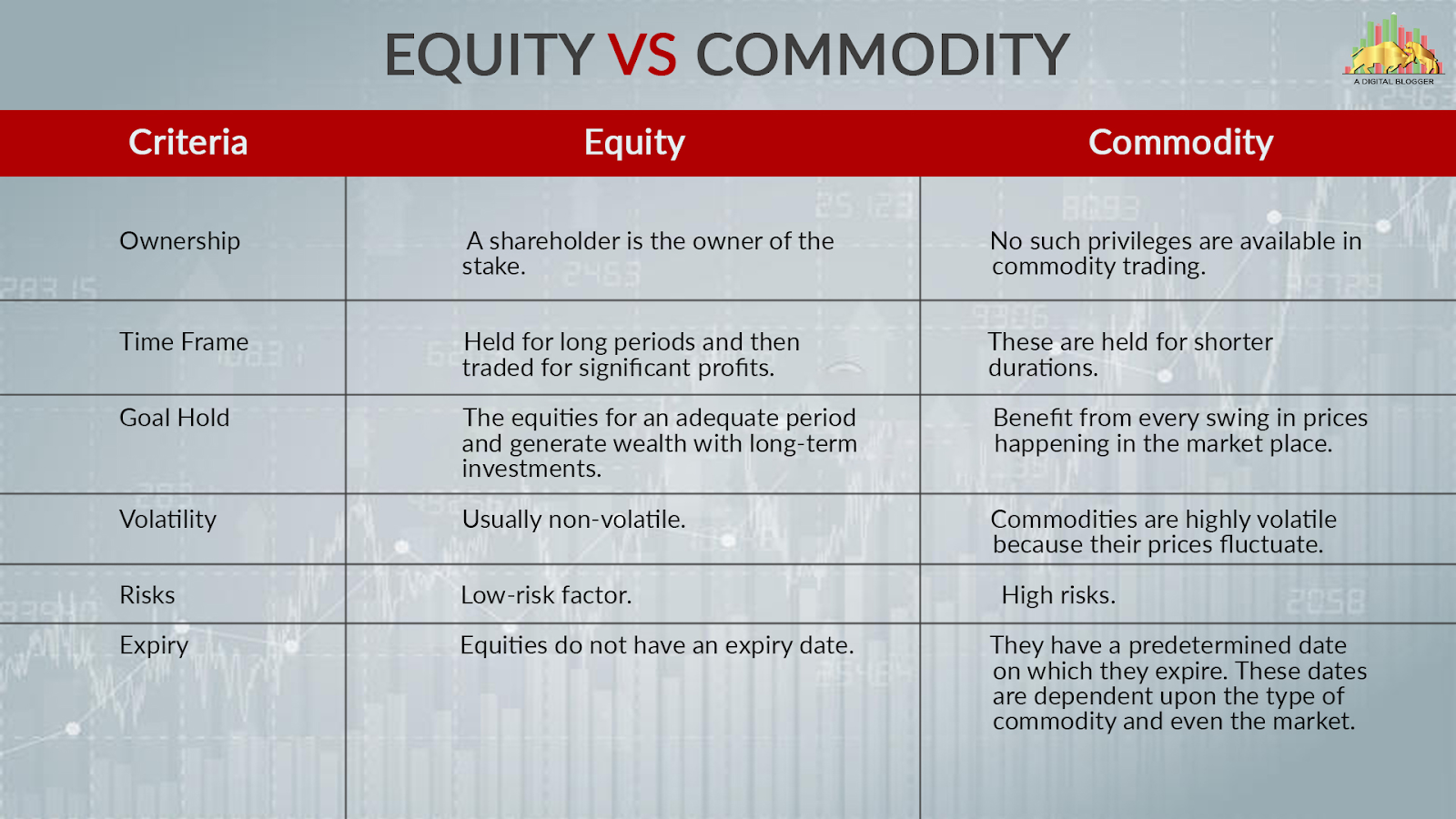

Securities? Commodities? What’s the difference?

While to many of us, these are just some of the things that we invest in, there is a legal distinction between them. To put it simply, securities are financial instruments that represent a claim on the issuer- such as shares in a company. On the contrary, commodities refer to goods that are traded in wholesale quantities.

Someone who buys securities can expect to profit when the company that issues the security does well, so if Ripple does well, the price of its token XRP can be expected to rise. Thus, XRP is considered to be an investment contract, at least according to the SEC- and it is this test, known as the Howey Test, that is used by the SEC to determine if a cryptocurrency is indeed a security and therefore under its purview.

In contrast, someone who buys a commodity is not going to expect dividends from the company that supplies them. Instead, someone who buys commodities expects profits when the price of the commodity itself increases.

If this seems esoteric, you aren’t completely wrong- for everyday consumers and retail investors, you will likely never have to know the difference.

But it matters for the companies like Binance and Coinbase, who have to apply for licenses before they are allowed to list securities or operate an exchange that offers such securities or commodities.

Assets, liabilities, or equity?

Yet, this is not the only issue of classification that crypto faces- there's also the issue of crypto accounting.

Companies, especially public companies, are often obligated to publish financial statements every year- often in the form of their balance sheets, income statements, and cashflow statements.

But how to account for crypto assets is far from clear, as Karthik Rajeswaran from Headquarters noted.

In a keynote speech at Crypto Expo Asia 2023, held last week as well, Rajeswaran outlined the difficulties involved in accounting for crypto assets.

“Firstly, there is the issue of volatility. The price of crypto assets are volatile, and can change drastically. Should we value them at the present market rate? And how should we do so? Different exchanges may see different tokens trade at different points, so which price point should be taken as the accurate one? And should we deal with the cost of acquiring crypto assets, and how should we value crypto subsequently, after the crypto has been obtained?

Then there is also the issue of how complex many crypto assets are. Are NFTs assets? Should we treat crypto that is being staked as part of a Proof-of-Stake consensus mechanism in the same way as crypto that is not being staked?”

-Karthik Rajeswaran, Vice President of Product, Headquarters

Currently, while there are proposed guidelines for how crypto assets should be treated, they are also far from clear.

Under the most recent proposal by the Financial Accounting Standards Board, crypto is to be treated as an indefinite-lived intangible asset. In other words, they do not suffer from amortisation or depreciation, but must be tested for impairment.

But to be perfectly confusing, increases in the value of the tokens itself will not be recognised, but decreases in token values are recognised.

The implications of these rules are immense- on one hand, it would mean that debacles like Luna would be far less likely because companies like Terraform Labs could not simply rely on a perpetually increasing token price to claim profitability and good performance.

But at the same time, it would also mean that financial statements published by companies that hold cryptocurrencies would not necessarily tell the full story on the company’s financial position.

And the question of if cryptocurrencies are securities or commodities would also have further implications here.

Securities are investment contracts- and imply that cryptocurrency issuers must list outstanding cryptocurrency as liabilities on their balance sheets. On the other hand, commodities are assets- which are listed as assets on a balance sheet.

Is there a better way to deal with all this?

Of course, retail investors may simply shrug their shoulders at this and ask ‘who cares?’

And they are not alone. In jurisdictions like Malaysia and Indonesia, the government has simply shrugged their shoulders as well and said that regulation of cryptocurrencies is the responsibility of their securities commission.

If consumer regulation is the goal, then at least having some regulation, no matter how incomplete it is, will likely be better than having no regulation at all. While the SEC and CFTC launch tirades against crypto companies and serve up lawsuits in the name of consumer protection, they are doing surprisingly little to work with each other to determine what regulation can and should look like.

Given that consumers will likely not appreciate the difference between securities and commodities, the present state of events suggests that the CFTC and SEC seem to be more interested in bringing crypto under their jurisdiction, rather than to bring it under regulation.

Hong Kong and Singapore have both been proactive in drafting regulation and asking for feedback from business leaders.

While there might be a case to be made that rushing into regulation may not yield the best regulation, we should also consider if getting sufficient regulation as a stop-gap measure and testing out different regulations and tweaking them later is really such a bad idea.

Cooperation, rather than conflict, should be the way forward- though given the state of US politics and the deadlocks that are often present, this is unlikely to happen.

But solving the question of crypto’s status as a commodity or a security does not necessarily solve the entire problem- there is the question of how accounting standards should treat crypto, and on how fair such regulation is to the different stakeholders in the crypto ecosystem.

Crypto regulation has a long way to go- and indeed it can be a brutal, ugly affair, as evidenced by the US. But it does not have to be the only way to do things, and progress is being made in Asian jurisdictions because of a willingness to cooperate and admit that governments are not omniscient.

At the end of the day, regulation exists for the benefit of consumers and stakeholders. It is not a test of ego and willpower- but an exercise in cooperation and an opportunity for education.

多くの友人がいまだにFHEをZKやMPC暗号化技術と混同しているので、この記事ではこれら3つの技術を詳細に比較する。

JinseFinanceCoinbaseの最高法務責任者であるPaul Grewal氏は、イーサリアムの規制上の地位を擁護し、SECによる証券としての分類に反対しています。Grewal氏は、イーサリアムがコモディティとして認識されていることを強調し、確立された規制の前例と、意思決定における明確性と一貫性の必要性を挙げて、イーサリアムETFの承認を妨げないようSECに要請しています。

Huang Bo

Huang Bo将来的には、コンポーザブル・モジュールの市場競争が激化し、無数の方法でイーサのスケーリングが可能になるのだろうか。

JinseFinanceブルームバーグのアナリスト、ジェームズ・セイファート氏は、イーサリアム先物ETFの承認が示唆するように、SECはイーサリアムをコモディティとして微妙に認識しており、以前の証券分類からの脱却を示唆している可能性があると指摘している。

BerniceJinseFinance

BerniceJinseFinance米国の暗号通貨を証券または商品として分類することは、市場参加者にとって依然として混乱の原因となっています

Beincrypto

Beincrypto2008 年の金融危機から 13 年が経ち、ビットコインと仮想通貨業界は同様の成長痛を呈しています。

BeincryptoDeFi スペースは、さまざまな業界や経済にまたがる破壊的なイノベーションを生み出し続けています。インターネットコミュニティには...

Bitcoinist

Bitcoinist暗号強気市場の利益が枯渇した場合、利益を維持する最善の方法は、レバレッジを使用して開くことです...

Bitcoinist