Opportunities of combining AI and Crypto

Chain abstraction, artificial intelligence, opportunities for the combination of AI and Crypto Golden Finance, from a technical perspective, can chain abstraction solve the fragmentation problem?

JinseFinance

JinseFinance

The claim that cryptocurrencies and blockchain technology will change the world is nothing new.

After all, blockchain technology is revolutionary, and the promise of a cryptocurrency not controlled by governments has been touted to provide greater financial freedom from the tyranny of governments and greedy corporations.

Without governments to water down the wine and create inflation, and without greedy corporations that provide nothing while extracting wealth from the masses, there will be a far larger pie for everyone- meaning more wealth distributed more equitably all around.

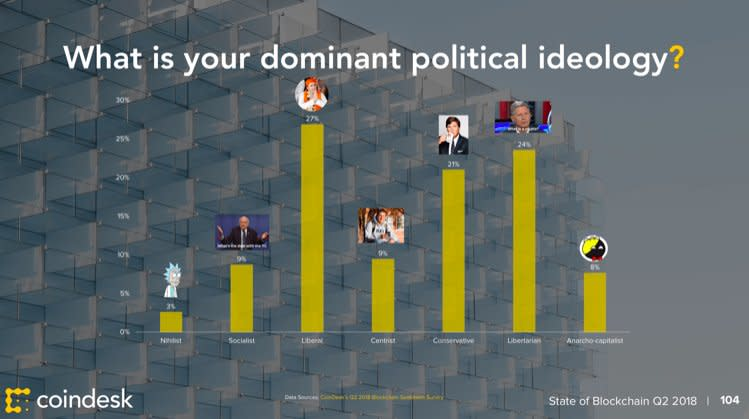

Certainly, such an ideology did play a part in early adoption for crypto, with prominent investors and adopters like Roger Ver openly associating themselves with it and citing it as a reason for their entrance into crypto. In Coindesk’s 2018 survey on the state of blockchain, 21 per cent of cryptocurrency holders identified themselves as conservative, 24 per cent identified themselves as libertarian, and 8 per cent identified themselves as anarcho-capitalist- making them the majority of cryptocurrency holders.

Even today, some of that old right-leaning ideology persists- Texas is among one of a few conservative states to enact pro-cryptocurrency laws, and Republican legislators are seen as pro-crypto, while democrats like Warren are building an anti-crypto army.

But is crypto really up to the task of remaking the world order? The crypto world looks very much like the real world- and perhaps even offers governments and corporations far more control than the real world.

The commercialisation of central bank functions

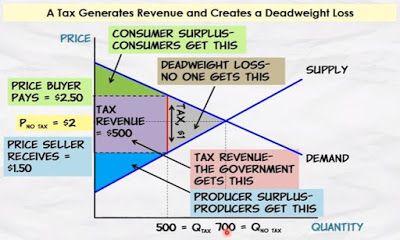

Central banks and governments are perhaps among the most hated institutions within crypto- where the crypto world promises decentralisation, central banks embody centralisation. While the crypto community prioritises free markets, central banks enforce regulation that crypto libertarians argue create deadweight loss.

The crypto space therefore offers a haven for those who abhor central banks and the arbitrary control that they exercise.

But in a world without central banks but with currencies, monetary policy still needs to be crafted, debated, and implemented. After all, someone still needs to decide when to create more of the cryptocurrency, who gets the cryptocurrency, and so on.

The main thrust of the crypto world’s argument thus far has been to democratise the process of making such decisions, with decentralised decision making, where people make decisions based on their interests.

There is some theoretical backing for this idea- and that is the idea that the masses themselves are the best at representing their own interests and that decisions made by the democratic processes of well-reasoned debate and universal suffrage will produce the best decisions.

Yet, voting in the crypto world is a far cry from the one-man, one-vote system found in most democracies. Instead, voting in the Web3 world is far more similar to voting in corporate or business structures, where money can quite literally buy votes.

In the aftermath of the Luna crash, Do Kwon’s Luna Foundation Guard strong-armed the community into voting for the revival of the blockchain, and guaranteed that only a proposal that they supported would pass. They did so by simply controlling around 60 per cent of all the tokens in circulation

I have spoken before about the necessity of non-elected institutions in a democracy. But this episode also shows that perhaps when left to its own devices, a cryptocurrency democracy may also devolve into a plutocracy.

Is tyranny by governments that you choose really that much different than tyranny by plutocrats? Probably not. And if we assume that people act in their self interest, what is there to stop the slide to plutocracy in the crypto world? After all, power begets more power, and powerlessness begets powerlessness.

At least in the real world, governments have a mandate to serve the people in order to remain in office, and wealth redistribution becomes a popular policy to gain support once the gap between the haves and the have-nots becomes too great.

In the crypto world, why would anyone with power redistribute power to the masses, especially when the masses have nothing to offer in return?

Meet the new oligarchs- same as the old oligarchs

At the level of businesses, one of the things that cryptocurrencies promised to bring about was an end to the old rent-seeking oligarchs and a fairer, more equitable distribution of wealth.

The Soviet premier Nikita Krushchev once remarked that ‘economics is a subject that does not greatly respect one's wishes.’ Ignoring the obvious irony of a communist leader commenting on economic policy while his own country’s economy was stagnating, the comment itself has a nugget of truth.

The Web3 world is not exactly known to have a market structure that resembles perfect competition or monopolistic competition. Name any market in the Web3 world, and you will likely be able to find that there remain a few key players with generally established control of the market, while smaller ones fight for scraps of market share.

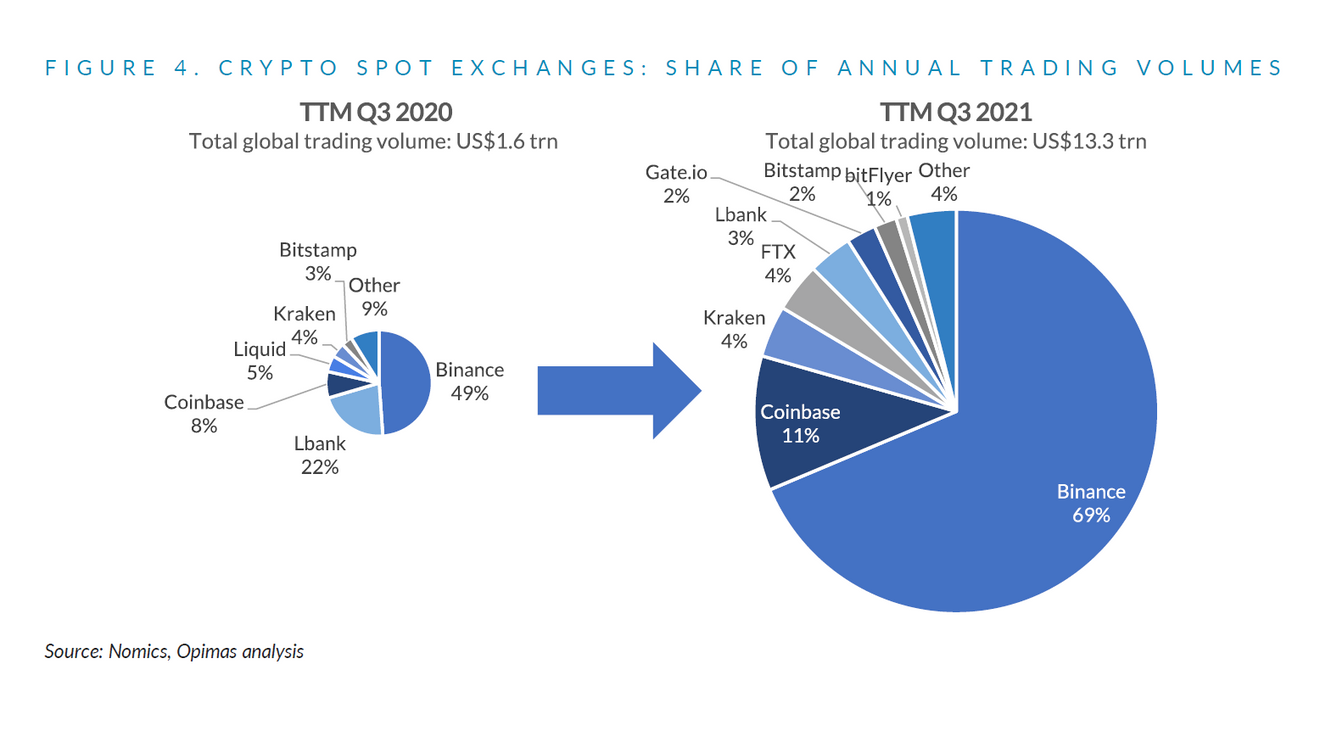

In the crypto exchange space, Binance is the largest player by far.

Its total trading volume dwarfs even that of its next closest competitor, and this leaves Binance in firm control of the space.

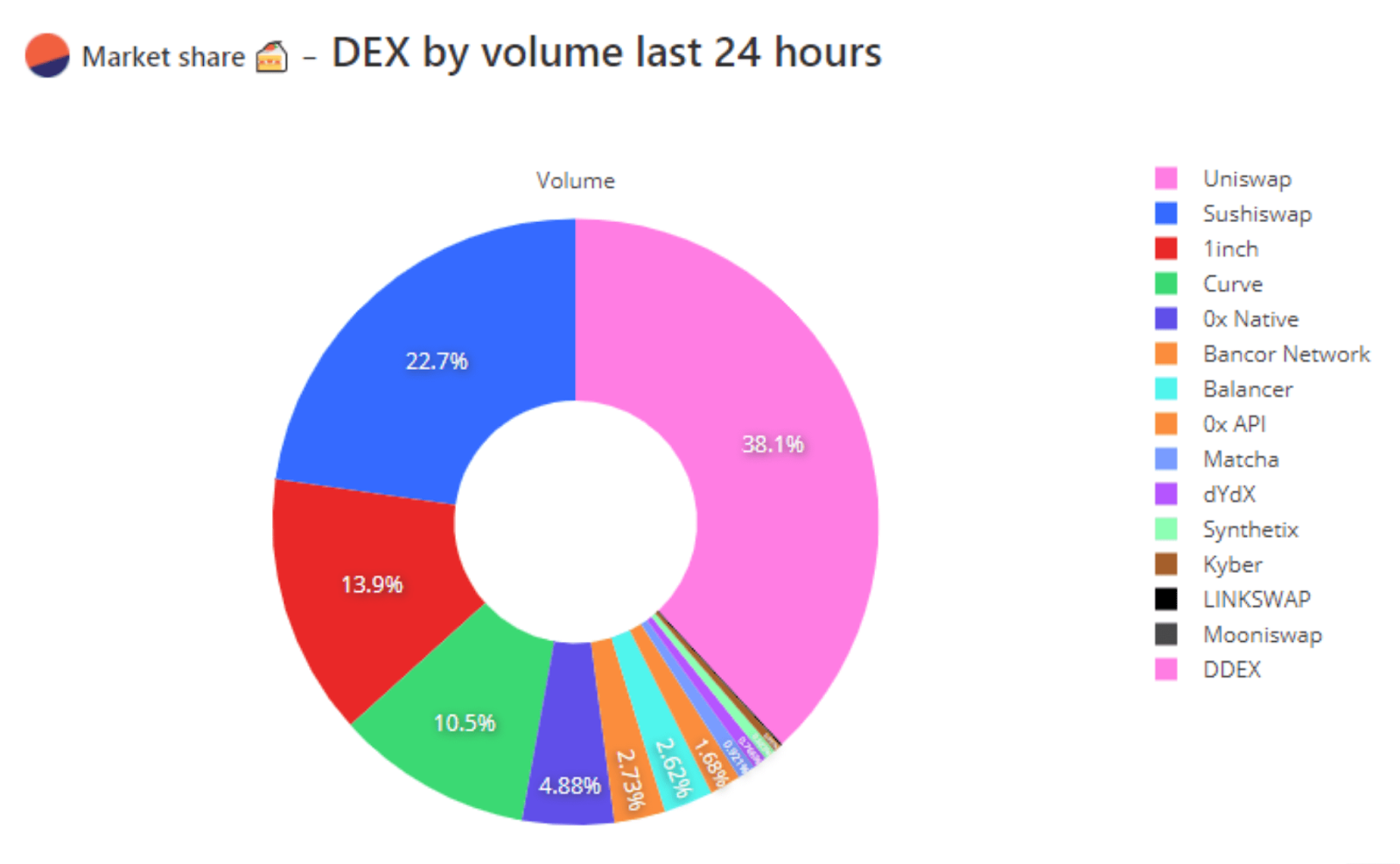

The DeFi space isn’t that much different, with the top four players controlling around 85 per cent of the market.

And now, the NFT marketplace scene is also being fought over between Blur and OpenSea

Evidently, it's not so much that crypto will remake the world order in the sense of eliminating monopolies and oligopolies- it merely creates new ones when new markets emerge.

Is there really a difference between the oligopolies in the real world and the blockchain world? Probably not. Customers choose which company they bring their business to- and the best companies get more customers and obtain a larger slice of the market. In the long term, Oligopolies emerge because users judge this small group of companies to be the best at what they do.

So really, the formation of oligopolies and even monopolies is not something that has been artificially created by governments or demanded by corporations seeking profits at the expense of consumers- it is the natural result of competition between companies for customers, and will exist whether it is the real world or the crypto world.

The professionalisation of crypto crime

In every world order, there will be pariahs- but for a technology that promises to change the world, the pariahs of the crypto world and the pariahs of the real world are surprisingly similar.

And in recent years, Russia and North Korea, both longtime targets of the Western world order, have also emerged as centres for crypto crime, though their brand of crypto crime is slightly different from each other.

Russia, in particular, has been known for money laundering and other financial crimes even before the advent of cryptocurrency. The country is also known for its facilitation of the illicit drug trade.

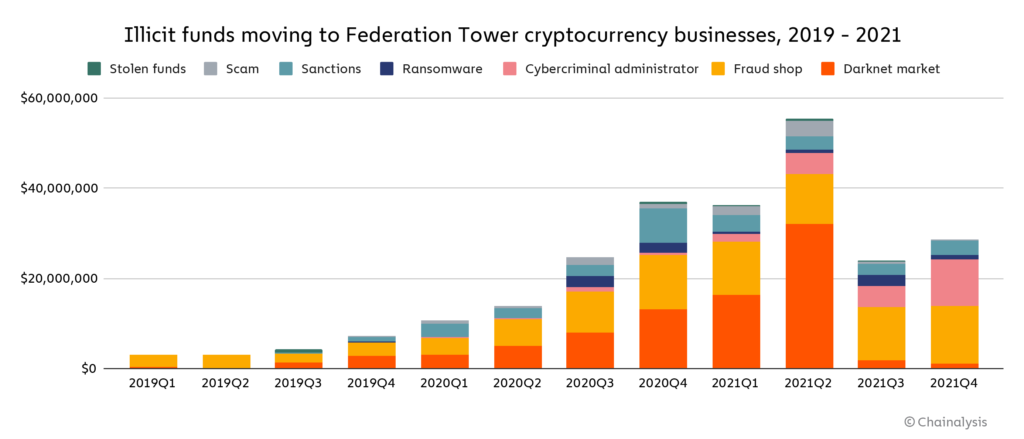

Since the advent of cryptocurrency, Russian criminals have become more advanced, and Chainalysis has even suggested that the Russian government, if not complicit, is at least looking the other way. Revenues from everything from cryptocurrency hacks and ransomware hacks are also increasingly flowing not just to Russia, but one particular location in Russia: Federation Tower in Moscow

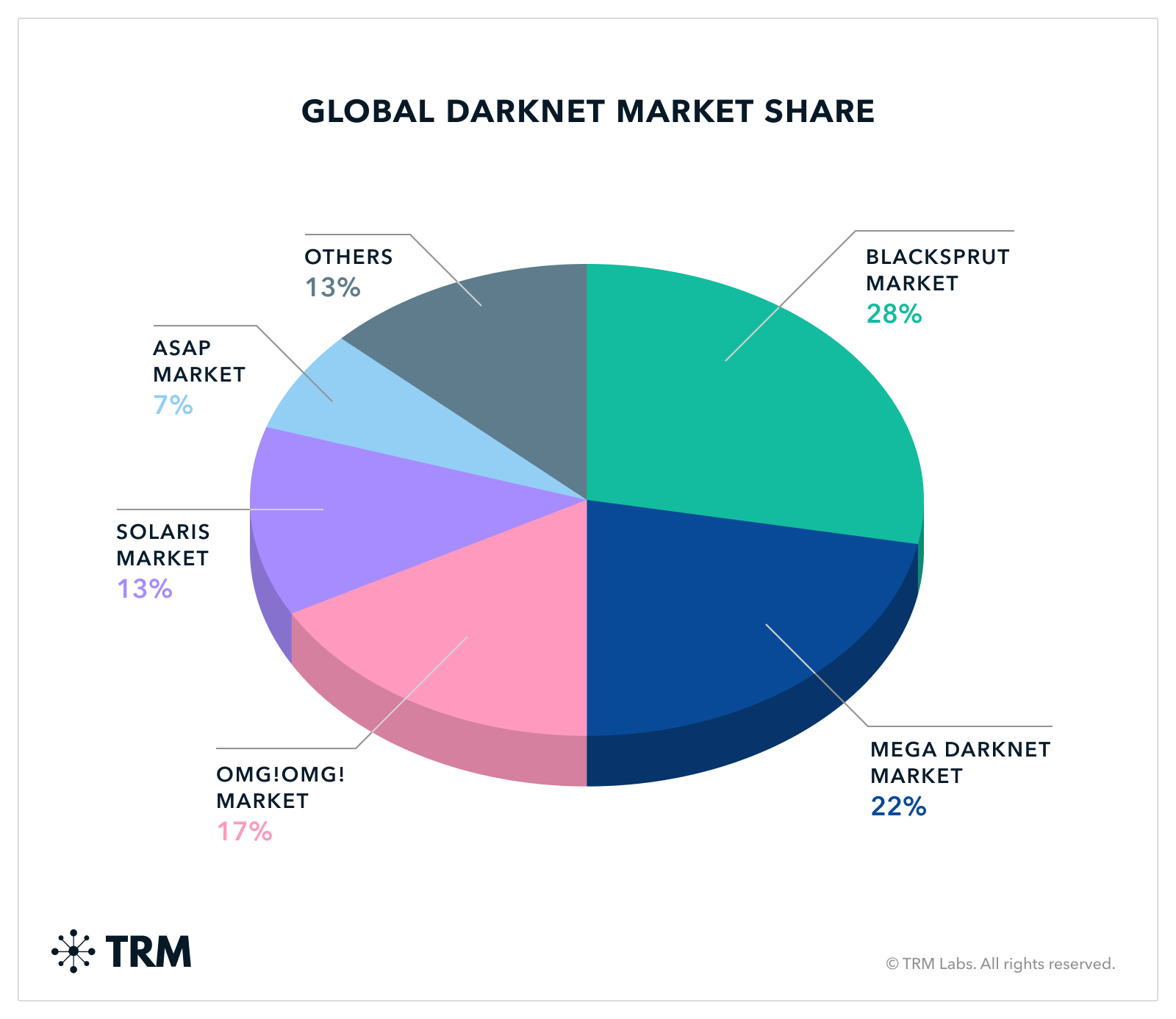

Cryptocurrency and blockchain tech has also changed the game for financial crime in Russia. Until its takedown last year, the darknet marketplace Hydra operated mainly from Russia. Even after the takedown, it remains home to many of the very same criminals and criminal organisations that operated on Hydra, who have now swapped to other darknet marketplaces and exchanges.

But even this pales in comparison with what North Korea has done with the advent of cryptocurrency. While Russia is simply looking the other way and is content with receiving its share of the profits of ransomware, illicit goods trafficking, and money laundering, North Korea has taken it a step further.

Just this week, North Korean hackers stole US$100 million from Atomic Wallet, and are currently trying to launder the funds through Garantex. These attacks are believed to be linked to the infamous Lazarus Group, which is itself believed to be backed by the North Korean government.

And this attack is just the tip of the iceberg. The group is also believed to be behind the Bangladesh Bank cyber heist, netting around US$81 million from the Bangladeshi central bank. Other victims include Banco del Austro in Ecuador, which lost US$12 million, and the Tien Phong Bank in Vietnam, which lost US$1 million.

Looking the other way at criminal activity is one thing- but explicitly setting up a group in order to target foreign financial institutions is another. Yet, this is exactly what North Korea is doing.

Evidently, international relations and the world order have not exactly changed significantly since cryptocurrency and blockchain technology has been created. Threats to individual freedom still exist, and states have appropriated these technologies in much the same way as they always have done whenever new technology comes about.

So does this mean that crypto will not remake the world order? Possibly. Crypto has not yet lived up to its promises of major, global change that will affect everyone. But at the very least, it has made a mark on global finance.

Adoption is rising, and many in trad-fi are starting to take notice. But it is perhaps time to fine-tune some of our assumptions and moderate our expectations. Thus far, crypto has not remade the world order in the sense of creating something completely new. If anything, it has entrenched and recreated the patterns that we see in the real world- both in terms of market structures, international relations, and even individual voting rights.

Chain abstraction, artificial intelligence, opportunities for the combination of AI and Crypto Golden Finance, from a technical perspective, can chain abstraction solve the fragmentation problem?

JinseFinanceThe meme market seems to be facing a collapse, and the market's anxiety is spreading again. What's the reason? The lack of new narratives, the investors are smart, and all went to blue chip NFT.

JinseFinanceLong-termist seems to be a very unpopular word at the moment, because most people in the circle are pursuing "opportunities to get rich quickly" and "immediate wealth feedback."

JinseFinanceArtificial Intelligence, Grayscale, Grayscale: Crypto x AI Project Overview How Crypto Can Achieve Decentralized AI Golden Finance, The AI Era Is Coming, Crypto Can Enable AI to Develop Correctly

JinseFinanceThe core value of Crypto is the value transmission network. In order to realize this core value, it requires a different computer architecture. The computer attribute of Crypto is a tool, and the network attribute is the purpose.

JinseFinanceExplore the various subsections within the Crypto x AI ecosystem: compute, AI agents, coprocessors, and more.

JinseFinanceAs part of this migration, Crypto Unicorns users can expect all transactions associated with the platform to be free, leveraging the already cost-effective gas on the XAI network.

AlexJinseFinance

AlexJinseFinanceHe has not offered any explanation on the matter, and the crypto community has begun speculating.

Beincrypto

BeincryptoThe dramatic bearish movement of digital tokens has brought doubts to the minds of several crypto and Bitcoin investors and ...

Bitcoinist

Bitcoinist