1. With the launch of Babylon and the opening of Lorenzo staking, let’s talk about the recent development of the BTC ecosystem

Since Ordi brought the BTC ecosystem to the forefront, BTC has actually quickly compressed the route that ETH has taken - first the on-chain assets (ERC20) - then the expansion plan (Rollup) - and then Staking/Restaking. But because there is no stabilizing force like ETHFoundation and Vitalik Buterin to set the direction, BTC is basically a situation of a hundred flowers blooming at once

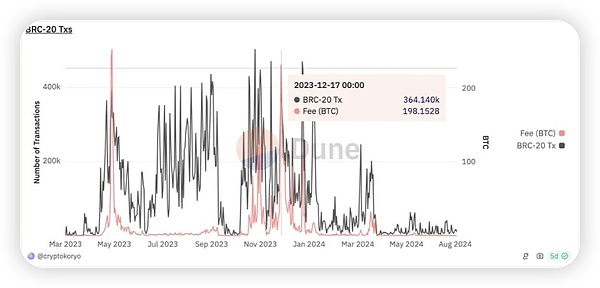

Ordinal was popular on the asset side first, and then Brc20, Arc20, Src20, Orc20 and other XX20s, which poured out like crazy. Many people were delighted last year that the BTC security model was likely to be solved (after another 20 to 30 years and four or five halvings, the block reward can be so small that it can be ignored. There must be enough TX on the chain to pay the miners for the handling fees). Last year, when Weimingwen was crazy about new listings, the handling fee did exceed the block reward. You can see it from this picture. At most, the handling fee was 300BTC a day

After ETH’s ICO in 2017, the next expansion plan was represented by Merlin, which first took ETH’s EVM ready-made technology stack + a multi-signature side chain to run (Polygon-which was called Matic at the time also did the same)

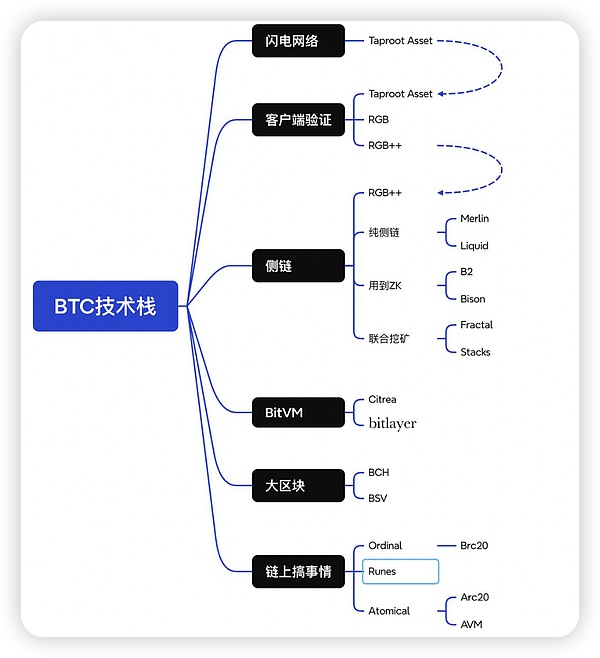

Then the expansion plan, compared with the official Rollup on the ETH side, BTC has much more

A simple diagram, basically like this (on-chain assets are also included as a technical branch)

Currently Taproot Asset can only be used for transfer. The most BTCNative (that is, starting from the UTXO feature) is definitely RGB (will the September mainnet be delayed again?), RGB++&UTXOStack, and Unisat's Fractal (which has been very popular recently)

The picture actually misses a route, which is the 1.5-layer contract virtual machine extension. The representative is undoubtedly ArchNetwork. The recently discussed OP_NET is also one of them, but Arch uses ZKVM and OP_NET uses WASM

The expansion solution has a very complicated technology stack, even more complicated than assets, so it is hard to say which one will come out on top in the end. We can only say that each has its own advantages and disadvantages. Leave it to time and the market. This is a pessimistic view. Maybe it is not impossible to disprove all of it in the end. After all, BTC’s current main narrative of “electronic gold” does not need to be expanded. Expansion is more for the service of “on-chain assets”. If the on-chain asset route does not take off, expansion will naturally lose its meaning.

Second, let’s talk about the third stage (Staking/Restaking)

This route is more solid than the previous two routes, because it does not conflict with the electronic gold narrative at all, and it is even a perfect supplement - releasing the liquidity of gold and turning gold into an interest-bearing asset!

The most important project at this stage is undoubtedly Babylon, because BTC does not have the natural POS Yield of ETH. Under the premise of the existence of Lido, EigenLayer’s Restaking narrative is more like a Booster for ETH itself, or icing on the cake. Babylon is a timely help for BTC. By restoring BTC through Trustless and generating Yield, BTC is no longer an interest-free "gold" asset.

The other two worth mentioning in this route are Solv and DLC.Link. The former gives BTC interest + SolVBTC liquidity in the form of Cefi+Defi (one of the entrances to Babylon), while the latter uses DLC technology to mint dlcBTC in the current environment of WBTC suffering from a trust crisis, "Trustless Bridge" BTC to ETH, Solana and other chains to participate in the Defi ecosystem. It is easy to understand and can be simply regarded as a decentralized and secure version of WBTC.

left;">Let's get back to the topic, back to Babylon and Lorenzo. Babylon is undoubtedly targeting the ecological niche of EigenLayer, so there will naturally be an asset entrance, that is, the ecological niche of LST/LRT is also extremely important. Eigenlayer has Etherfi, Renz0, Puffer, etc., and Babylon also has Solv, Lombard, Lorenzo competing for the entrance.

The differentiation of each company is greater than that of several leading projects on Eigen's LRT side. For example, Solv, in addition to Babylon, also has income on Cefi, Defi, and cooperation income with various BTC/ETH-related projects and the second layer with Ethena, Merlin, Arb, etc.

Lombard has advantages in capital and circle resources. At the same time, the LBTC it issued is also the most secure one. The CubeSigner (a professional non-custodial key management platform) + Consortium (a quasi-alliance chain node network composed of industry leader nodes) used is the most balanced solution I have seen in terms of security and flexibility.

Lorenzo directly integrates the principal and interest separation function of Pendle into it, with the liquidity pledge token stBTC for the BTC principal part (the same for each pledge project) and the liquidity pledge token YAT for the interest part (different for each pledge project). Lorenzo is also the only project on the market that provides users with the dual incentive system LST of YAT and points. The current total limit is 250BTC (to ensure user benefits), and there is a capacity of about dozens of BTC, which is expected to be full soon. First come first served

Finally, compared with the two directions of issuing assets and expanding the capacity on the BTC chain, the interest generation/liquidity release of BTC is a more visible and tangible direction, which can be seen from Binance's layout in this direction, especially the asset entrance. Among the projects mentioned above, Binance has invested in Renzo, Puffer, Babylon, Solv, and Lorenzo, so you know, this track needs to be taken seriously!

JinseFinance

JinseFinance