Can Farcaster, the leading social protocol, become a new hot spot in the bull market?

To date, Farcaster has earned nearly $1.9 million through registration fees and data storage fees.

JinseFinance

JinseFinance

Four months after the Bitcoin halving, we have witnessed the worst price performance after the halving to date. In this post, we explain why the halving no longer has a fundamental impact on the price of BTC and other digital assets, with the last halving dating back to 2016. As the digital asset market matures, founders and investors should move away from the concept of four-year cycles.

Author: Jasper De Maere @outlierventures

Compiled by: Liam

Summary:

Bitcoin completed its fourth halving in 2024, and experienced the worst price performance 125 days after the halving. The price fell 8%, while the previous halving cycles rose by 22%.

We believe that 2016 was the last halving to have a significant, fundamental impact on Bitcoin. Since then, the size of BTC block rewards for miners has become insignificant against the backdrop of an increasingly mature and diversified crypto market.

The strong performance of BTC and crypto markets after the 2020 halving is purely coincidental, as the 2020 halving occurred during an unprecedented period of global capital injection in the post-pandemic era, with the US money supply (M2) alone increasing by 25.3% that year.

The view that the 4-year cycle is still valid in 2024, but the approval of the BTC ETF in January 2024 brought forward demand, causing BTC to rise strongly before the halving is wrong. The approval of the BTC ETF is a demand-driven catalyst, while the halving is a supply-driven catalyst, so the two are not mutually exclusive.

Bitcoin prices have a significant impact on the broader market and therefore also affect founders' ability to raise funds through equity, SAFTs, and private or public token sales. Given that cryptocurrencies bring liquidity to venture capital, founders must understand the top-down market drivers to better predict funding opportunities and operating cycles. In this post, we will break down the concept of the four-year market cycle to lay the foundation for exploring the true drivers in future work. Breaking down the concept of the four-year cycle does not mean that we are pessimistic about the overall market.

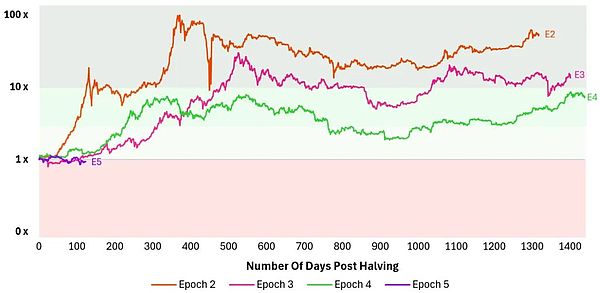

Let's first look at the performance of Bitcoin prices in the past few halving cycles. It is clear that in the fifth cycle after the halving (2024), Bitcoin's performance is the worst since the halving, and it is also the only halving cycle in which Bitcoin prices have fallen.

Chart 1: Bitcoin price performance in various cycles before and after the halving

So why does the halving have an impact on the price? In short, there are two main reasons.

Basic reason: Bitcoin halving reduces new supply, leading to increased scarcity, and when demand exceeds limited supply, the price will rise. This new dynamic will also change the economic situation of miners.

Psychological reason: Bitcoin halving will increase the sense of scarcity, strengthen expectations of price surges based on historical patterns, and attract media attention, thereby increasing demand and pushing up prices.

In this work, we argue that the fundamental drivers behind Bitcoin’s price action have been overstated and have been irrelevant over the past two cycles. We will start with context and demonstrate that the net effect of the halving is not large enough to have a significant impact on Bitcoin’s price or the broader digital asset space.

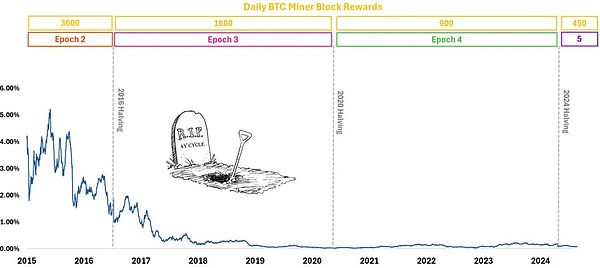

Daily Bitcoin Rewards

If you take away only one thing from this post, let it be this:

The strongest argument for the Bitcoin halving’s impact on the market is that, in addition to reducing Bitcoin inflation, it will affect miners’ economics, leading to changes in their money management.

So, let’s consider the extreme case where all mining rewards are immediately sold on the market. What would the selling pressure be? Below, you can assess this impact by taking the total daily block rewards (in USD) received by all miners and dividing it by the total market volume (in USD).

Until mid-2017, miners had an impact on the market of more than 1%. Today, if miners sold all of their BTC block rewards, they would only account for 0.17% of the total market. While this does not include the share that BTC miners previously accumulated, it shows that as block rewards decrease and the market matures, the impact of BTC block rewards on the market has become negligible.

Figure 2: Impact on the market if all miners sell their daily BTC block rewards

Halving Impact

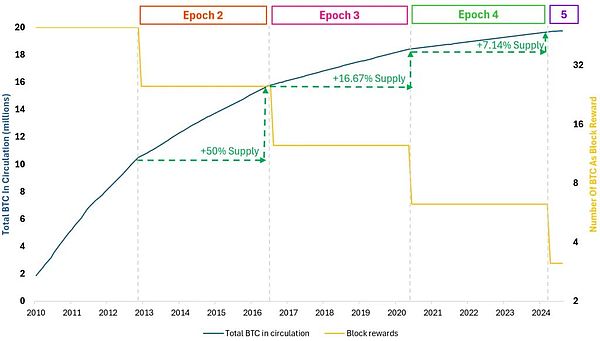

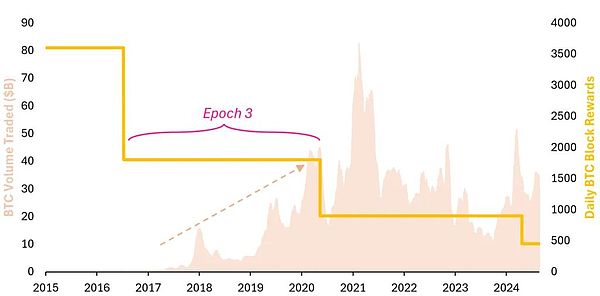

Let's review first. The Bitcoin halving occurs approximately every four years, and miners' block rewards are halved. This reduces the rate at which new BTC are generated, reducing the new supply entering the market.

BTC’s total supply is capped at 21 million, and with each halving, the rate at which the cap is reached slows. The period between each halving is called a “cycle,” and historically, each halving has impacted Bitcoin’s price as supply decreases and scarcity increases. See Figure 3 for details.

Figure 3: Bitcoin Halving Dynamics, Block Rewards, Total Supply, and Cycles

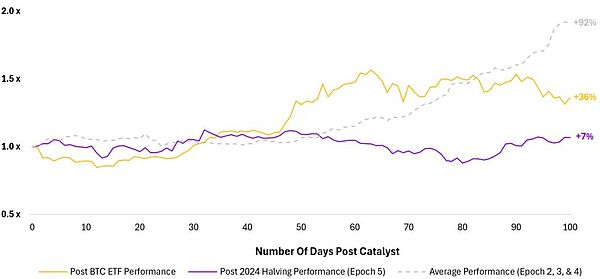

Bitcoin’s Post-Halving Performance

First, in terms of price performance, which is most important to most of us, we see that post-halving performance is the worst since Bitcoin was created. As of today (September 2, 2024), Bitcoin is trading about 8% lower than the opening price of $63,800 on April 20, the day of the halving.

Chart 4: BTC price performance after each halving

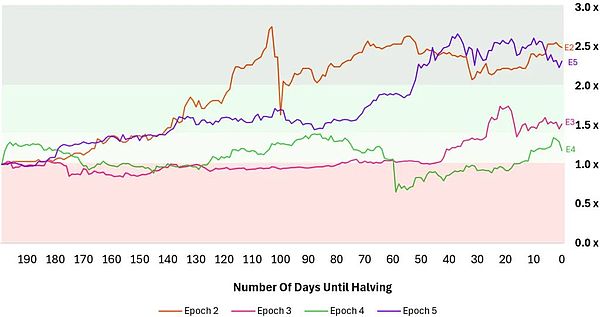

"What was the performance before the halving?" The performance before the halving was indeed very strong. Looking back at the performance 200 days ago, we find that the price of BTC has almost doubled by 2.5 times. This is almost the same as the situation in the second cycle when BTC accounted for 99% of the market value of digital assets. The halving was still significant at the time.

Chart 5: BTC price performance 200 days before each halving cycle

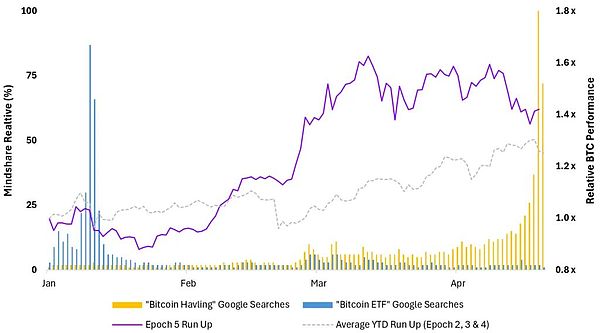

That being said, it is also important to remember what happened during that period. In early 2024, we got the approval of the BTC ETF, and since January 11, 2024, BTC has had a net inflow of 299,000, which has greatly driven the price increase. So, the price increase was not because people were expecting the halving.

Chart 6 shows BTC's performance between the BTC ETF approval and the halving. After the BTC ETF was approved in January 2024, the demand for BTC increased, causing the 100-day increase in the 5th cycle to exceed the average cycle increase by 17%.

Figure 6: 200-day increase in BTC price before halving in each cycle

Figure 7 shows the 100-day performance of Bitcoin ETF approval and halving. Obviously, the approval of Bitcoin ETF and halving have a greater impact on the price, and the price difference between the 100-day performance of the two is about 29%.

Chart 7: Bitcoin Performance 100 Days After Halving and ETF Approval

"So the Bitcoin ETF triggered the demand and price action we normally see at the halving in advance!"

This is a weak argument to defend the 4-year cycle. The reality is that the two catalysts are independent of each other. The ETF is a demand-driven catalyst, while the halving is a supply-driven catalyst. They are not mutually exclusive, and if the halving remains important, we should see significant price moves from the dual catalysts.

2016 Was the Last Halving

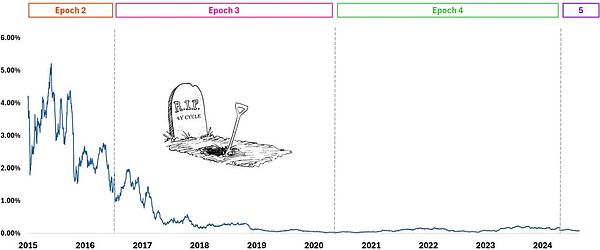

I believe 2016 and entering the 3rd cycle was the last time the halving had a truly meaningful impact on the market. As discussed in Exhibit 2, the chart below shows the impact on the market if all miners sold their block rewards on the day they received them. As you can see, around mid-2017 it dropped below 1%, and today it barely reaches above 0.20%, suggesting that it is of minimal importance.

Figure 8: Possible impact on the market if all miners sold their daily BTC block rewards

To understand the decline in the influence of miners’ financial decisions, let’s take a closer look at the individual variables at play.

Variables:

Total daily BTC block rewards - falling every cycle

Total daily BTC transactions - rising as the market matures

As the block rewards decline over time and the market matures, the relevance of miner influence decreases.

Figure 9 shows the cumulative BTC transaction volume and miners’ BTC block rewards. It is precisely because of the sharp rise in transaction volume that miners’ block rewards have become insignificant.

Figure 9: BTC Miner Daily Rewards and Daily Transaction Volume

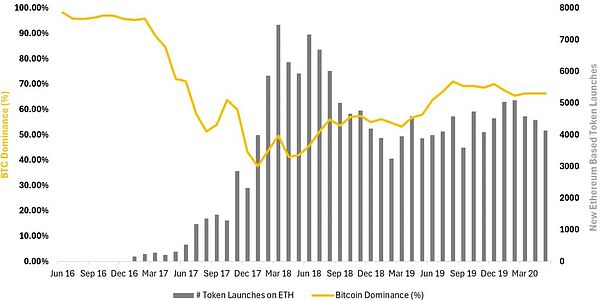

For those who read it at the time, it was obvious what drove the growth in transaction volume during this period. To recap: After Ethereum was launched in 2015 and unlocked smart contract functionality, the ICO boom ensued, leading to the emergence of many new tokens on the Ethereum platform. The surge in new tokens led to a decline in BTC’s dominance. The influx of new assets (i) drove transaction volume in all corners of the digital asset market, including BTC, and (ii) incentivized exchanges to mature faster, enabling them to more easily attract users and handle larger transaction volumes.

Chart 10: ETH New Token Launches and BTC Dominance in Phase 3

But…but what about 2020?

A lot happened in the third cycle, which logically reduced the impact of mining fund management and further reduced the impact of the Bitcoin halving itself as a catalyst. So what about 2020? In the first year after the halving, Bitcoin rose about 6.6 times. This was not due to the halving, but to the unprecedented amount of money printed in response to the COVID-19 pandemic.

While not a fundamental factor, the halving may affect Bitcoin's price trend from a psychological perspective. When the Bitcoin halving made headlines, it provided people with a target to invest their excess funds when there were few other consumption options.

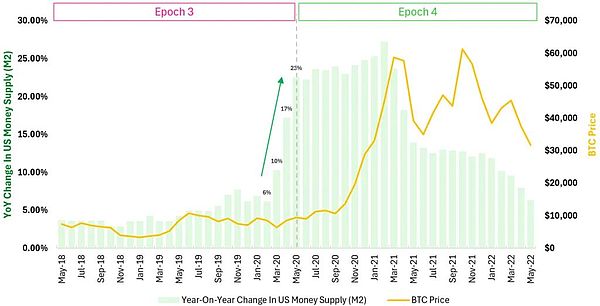

Figure 11 shows the real reason for Bitcoin's rally. Just a few months before the May 2020 halving, the U.S. money supply (M2) surged at a rate unprecedented in modern Western history, driving speculation and inflation across a variety of asset classes including real estate, stocks, private equity, and digital assets.

Figure 11: U.S. money supply (M2) and Bitcoin price before and after the 2020 halving

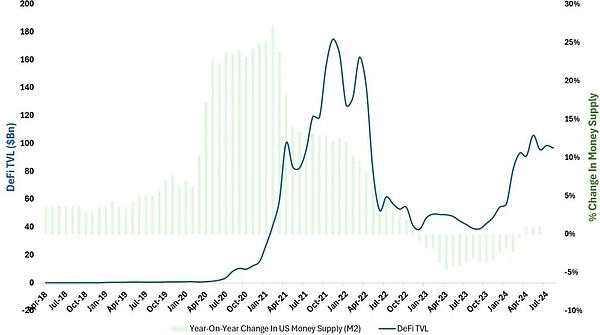

In addition to the funds flowing into BTC, it is important to recognize that money printing occurred after the DeFi Spring, which then led to DeFi entering the DeFi Summer. Many investors were attracted by the attractive yield opportunities on the chain and put their funds into cryptocurrencies and utility tokens to capture value. As there is a strong correlation between all digital assets, BTC naturally benefited from it.

Figure 12: US Money Supply (M2) and DeFi TVL

At the time of the halving, the global helicopter money policy drove a series of factors, triggering the largest cryptocurrency rally to date, and it seems that the change in block rewards has a fundamental impact on price behavior.

Miner Remaining Supply

"What about the remaining BTC supply held by miners in their vaults? This supply was accumulated in previous cycles when the hash rate was low and the block reward was high?"

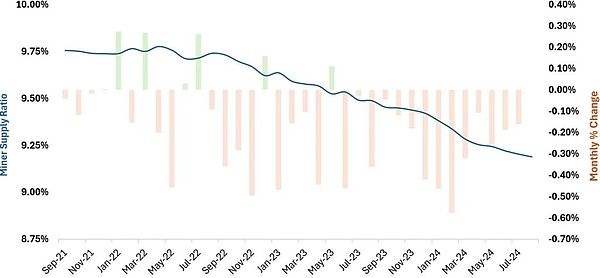

Figure 13 examines the miner supply ratio, which is the total amount of BTC held by miners divided by the total BTC supply, effectively showing how much supply miners control. The impact of miners' inventory decisions on BTC prices depends largely on the block rewards they accumulated in the early days.

As shown in the figure, the proportion of miners' supply has been steadily decreasing and is currently around 9.2%. Recently, there has been an increase in OTC trading activities of miners selling BTC, which may be to avoid having too much impact on the market price. The reasons for this trend may be the reduction in block rewards, the increase in input costs such as hardware and energy, and the lack of a significant increase in BTC prices, forcing miners to sell BTC faster to remain profitable.

We understand the impact of halving on the profitability of the mining industry and their need to adjust fund management to remain profitable. However, the long-term direction of development is clear. The impact of halving on BTC prices will only continue to decrease over time.

Chart 13: Miner Supply Ratio and Month-over-Month Change

Conclusion

While the halving may have some psychological impact, reminding Holders to pay attention to their dusty Bitcoin wallets, it is clear that its fundamental impact has become irrelevant. The last meaningful halving impact occurred in 2016. In 2020, it was not the halving that triggered the bull run, but the response to COVID-19 and the subsequent money printing. It is time for founders and investors trying to time the market to focus on more important macroeconomic drivers rather than relying on four-year cycles. With this in mind, we will explore the real macro drivers behind market cycles in future Token Trend Lines.

To date, Farcaster has earned nearly $1.9 million through registration fees and data storage fees.

JinseFinanceBTC, the top price forecast of BTC in this cycle Golden Finance, the high point of this round is expected to be around $134,000

JinseFinanceBitcoin’s price chart is similar to the one it saw just weeks after the 2016 halving and is currently hovering near a local bottom, according to cryptocurrency traders.

JinseFinanceFloki price jumps 15% to $0.0001968, aided by Revolut listing. Bullish indicators hint at further gains, with $0.00020 as key resistance. Speculation eyes $0.00025 by summer. Slothana among promising meme tokens.

Edmund

EdmundDespite market pullback, Dogecoin (DOGE) aims for $1 milestone. AI forecasts caution, expecting $0.161 by April end, a -16.15% decline. Dogecoin struggles to maintain upward momentum amid support level dip. Co-founder Billy Markus emphasizes market volatility, urging cautious optimism.

Huang Bo

Huang BoAnalysts foresee a potential correction in Solana's price, with varied predictions on specific levels. The current market status reflects a recent decline, emphasizing the need for investors to monitor key support levels.

Bernice

BerniceRenowned author Robert Kiyosaki, famous for his book "Rich Dad Poor Dad," has shared his predictions on the future prices of Bitcoin, gold, and silver, alongside a stern warning concerning the risks associated with holding U.S. dollars, which he termed "fake money."

Jasper

Jasper比特币 BTC 区块链 加密货币

fx168news

fx168news NulltxNulltx

NulltxNulltx