Author: Westie; Compiled by: Vernacular Blockchain

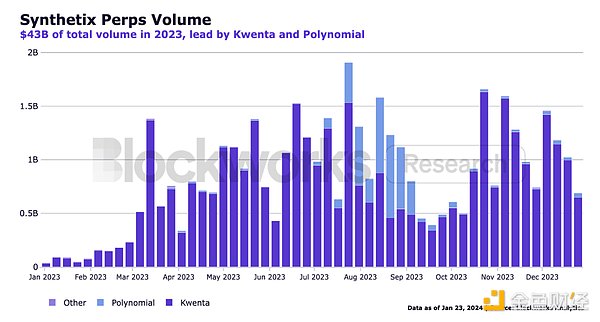

2023 is an erfolgre for Synthetix One year. Perps V2 quickly achieved product-market fit, with transaction volume of approximately US$43 billion and fees incurred of approximately US$36.5 million. In 2024, Synthetix V3, Perps V3 and USDC combination will be launched for Base deployment, as well as focusing on other cross-chain deployments. The Spartan Council allocates 40% of the fees generated through SNX inflation elimination and Andromeda deployment for repurchase and destruction.

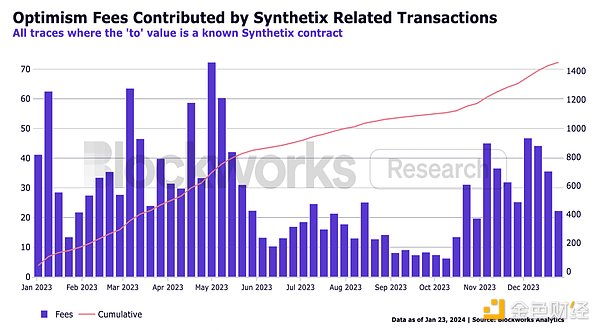

Synthetix is also one of the main drivers of Optimism's success, as it accounts for the majority of the chain's TVL (Total Value Locked), activity and revenue. Synthetix ended the year with $316 million in TVL, accounting for approximately 34% of all TVL on the Optimism Mainnet. Additionally, Optimism Mainnet transactions related to Synthetix, including any spot and perpetual transactions as well as SNX staking, drove approximately 1,460 ETH (approximately $3.5 million) in transaction fees in 2023, which accounted for approximately 7.3% of overall chain revenue. %.

Though some attribute this increase in activity to 5.9 millionOPs in incentives, which at the time were worth approx. 9 million, which Synthetix and its front-end used as fee rebates for traders on the platform, but after the incentive period ended, trading volumes remained relatively high. Compared to the $15.5 million raised during the incentive period, Synthetix still achieved an average daily trading volume of $151 million, and even reached a peak weekly trading volume of $1.6 billion in the week of October 23. This means that these incentives create a certain level of stickiness for users and transaction volume.

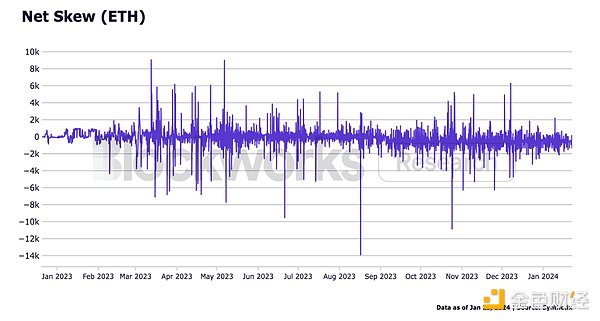

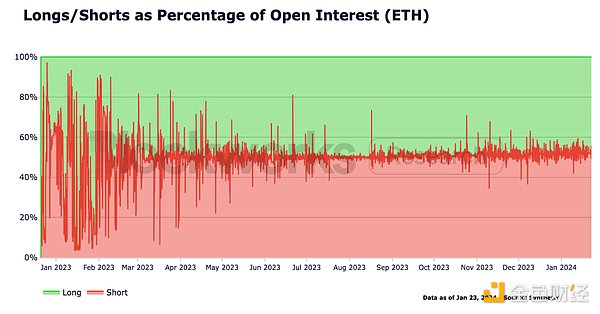

While trading volume and fees are obviously very important, an important aspect for SNX holders is reducing exposure to market volatility. This is achieved through Perps V2’s dynamic funding rate. Rather than only considering bias (i.e. the difference between longs and shorts), dynamic funding rates also take velocity into account. This means that if there is a persistent long bias over the long term, funding rates will continue to increase over time. This system greatly incentivizes traders to carry out arbitrage trades and maintain balanced positions. Although there were large fluctuations in early 2023 due to the extremely small position limit, it has remained very stable for the most part, with only occasional small fluctuations.

Others Competitors such asGMXare now incorporating dynamic funding rates into their products as they have proven successful in reducingliquidity Provider’s market exposure.

With a sustainable product that has clearly found product-market fit, Synthetix sets its sights on ambitious deployments in 2024 to upgrade its product line , expand perpetual trading across chains, add new collateral types to maximize liquidity and capital efficiency, and incentivize front-ends to create an enhanced user experience comparable to centralized trading platforms.

1. Synthetix V3 and Perps V3

Synthetix is currently converting its current V2x system Migrate to new products: Synthetix V3 and Perps V3.

Synthetix is the core layer of liquidity in financial markets. In V2, SNX holders can stake their SNX and take on debt positions. This debt is then represented by their corresponding share of the total system debt among all holders. Leveraging the value created from this global pool of debt, synthetic asset markets formed. As positions are entered and exited, the debt system updates to reflect changes in balances. As mentioned earlier, this makes SNX holders a temporary counterparty to traders in the perpetual contract, as the dynamic funding rate has proven to be able to maintain open positions< strong>Balance.

In V3, Synthetix takes this liquidity layer concept to the next level by creating a more modular system. This enables developers and users to experiment across different layers of the liquidity stack.

The core of V3 starts at the pool level. Each pool represents an independent source of debt and liquidity, which is then used to provide liquidity to the market. Debt and liquidity come from Vaults, whereliquidity providersdeposit their assets and delegate their collateral to the pool. Each pool has a Vault for each collateral type it accepts, and pools can choose any collateral asset they want. Pools can then stake the market into the market of their choice. While these can be spot or perpetual markets that Synthetix already has, there are also opportunities for developers to build entirely new markets.

This design allows for experimentation in different markets while allowingliquidity providersChoose the aamount of riskto take. The main pool will be the Spartan Pool, and its allocation, collateral assets, and market will be determined by the Spartan Council. Most liquidity providers will choose to offer this more secure system, but if someone wants to build a permissionless perpetual futures market, the higher risk but potentially higher reward capability is now available.

So far, several teams have expressed a desire to build products using V3 infrastructure. One of them is Overtime Markets, a sports betting platform built on Thales that is currently migrating its current infrastructure to V3. It is likely that the market will be absorbed by Spartan Pool soon after launch, as the liquidity provider has achieved annualized returns of over 70% in less than a year. Other protocols that have expressed interest in building on V3 include Betswirl, a CasinoFi project, and TLX, which is creating a tokenized version of Synthetix perpetual positions. Other market types, such as options markets, insurance markets, and prediction markets, have also been proposed.

While much of the focus this year will be on promoting sustainable products through enhanced user experience and portability across many chains, V3 will be available for experimentation , so that new markets can emerge.

Synthetix also plans to release the next version of its sustainability product, which will exist as a marketplace under the V3 infrastructure: Perps V3. This upgrade will improve the perpetual contract infrastructure to provide an overall enhanced user experience. This means latency improvements for traders, a native cross-margin system, expanded collateral options including open trading with synthetic assets like sETH and sBTC, progressive liquidations to reduce mezzanine liquidation risk posed by MEV seekers, and NFT-based account. This improved user experience fits well with Synthetix’s plans to expand perpetual contract activity in 2024.

2. 2024 Roadmap

Synthetix is entering a critical stage of its development. While the Perps V2 product demonstrates clear product-market fit, there are limitations in user experience that limit potential growth and activity. Perps V3 is improving the perpetual trading experience, but there is still a long way to go to create an on-chain trading experience comparable to that provided by centralized trading platforms. In 2024, Synthetix and its ecosystem hope to close this gap as much as possible.

One limitation of the current perpetual contract system is that users can only trade on Optimism Mainnet. While the chain itself provides a good enough user experience, porting the product to other chains with different user sets will allow Synthetix to generate more activity and revenue and build its brand in different communities.

The experimentation and migration process to other chains will begin with Synthetix’s suite of products called Andromeda, which will include Synthetix V3, Perps V3, and USDC as The only type of collateral. This environment is helpful for testing the new product itself and understanding the extent of the need to use USDC to provide liquidity instead of using the SNX native token.

Synthetix is specifically testing USDC because of its potential for better liquidity. Since USDC is a stablecoin, it allows liquidity providers to have lower required loan-to-value ratios (LTV), thereby improving capital efficiency and not requiring LPs to have significant market exposure Therefore, this increases the expected annualized return for liquidity providers. For example, if we assume that SNX holders earn an annualized return of 3% at a CR of 500%, other things being equal, USDC will earn an annualized return of 13.6% at a CR of 110% Rate. In addition to this, there are plans to introduce (without governancevotings) sDAI-like yield-stabilizing collateral to additionally support this potential yield. In addition to the ability to take on sUSD debt and earn additional yield elsewhere, this attracts yield farmers and yield-maximizing vaults, thereby attracting large amounts of liquidity to Synthetix.

The first deployments of Andromeda are currently being rolled out onBase. This will be the first testing ground for Perps V3 and USDC as primary collateral. The total USDC allowed will be gradually increased, and trading of liquidity and open interest will be allowed on the perpetual market. Additionally, Kwenta, the largest Synthetix front-end, stated that they will “actively promote” users to adopt V3 and provide incentives once the rollout is complete and there is sufficient liquidity to meet the needs of traders.

< /p>

< /p>

With deployment on Base, there will be the introduction of Infinex, a platform focused on providing traders with an enhanced user experience and creating a liquidity flywheel for sustainable trading. new front-end. Infinex was launched by Kain%20 Warwick, the founder of Synthetix, and uses SNX as its governance token. They will also receive 20% of the front-end fees for buying back SNXToken and staking them to facilitate the cycle of further liquidity. Feature highlights included within Infinex include login with username and password,multi-factor authentication andcross-chainDeposit. To the user, it feels like using a trading platform, but the backend is powered by decentralized and permissionlessliquidity .

After successful deployment on Base, Synthetix will look to deploy Andromeda to Optimism%20Mainnet, possibly adding ETH as an additional collateral asset. This will run in parallel with the current Perps%20V2 system and will understand whether SNX or USDC and ETH are preferred when providing liquidity. Synthetix will then look to scale on otherEVMchains and Rollups to identify where they can generate more users and liquidity. While the next destination has yet to be determined, the community seems to be leaning toward Arbitrum.

In addition to the promotion of Andromeda, Synthetix is also specifically deploying a sustainable product on the Ethereum mainnet, which they call Carina. While using Ethereum is significantly more expensive and slower than deploying on Rollup, this is specifically designed for traders leveraging Synthetix perpetual contracts or a group of traders deploying their infrastructure on mainnet. For these entities, functionality connected to Rollup increases their risk. The first protocol explicitly built on Carina will be Ethena, a stablecoin project that uses delta-neutral positions to back its stablecoin USDe, which holds stETH and shorts perpetual contracts. Ethena has earned more than $130 million in TVL during the closed alpha test, part of which will be hedged through the perpetual contract when Carina is officially launched. Since stETH is native to Ethereum, this product is ideal for reducing risk and maximizing composability.

Synthetix is also exploring the possibility of creating an OP%20Stack%20Rollup called the Synthetix chain. The purpose is to create a centralized place for governance for SNX holders to collateralize borrowing and bring their sUSD to the chain of their choice, and to distribute the resulting fees between different deployments. Debt from the current V2x system will be completely migrated to this Synthetix chain, along with SNX holders.

3. SNXToken Economics Improvement

On December 17, Spartan Director Will vote to reduce SNX inflation to zero. Inflation used to be a huge obstacle for users and investors to hold SNX, because the previous inflation rate was extremely high, causing holders to devalue and causing huge selling pressure on the Token. Although inflation has fallen roughly to around 5% over the past year, many people who were previously affected by SNX inflation can now revisit that decision.

Another improvement to token economics comes from the deployment of Andromeda on Base. The Spartan Council approved SIP-345, which stipulates that 50% of the fees generated by the protocol, after the aggregator fee share, will be used to buy back and destroy SNX. The other 50% of the net protocol fees will be burned in sUSD as currently implemented. Although the aggregator fee share has not yet been formally determined through governance, it is expected that the aggregator fee share will be 20% and will be paid directly from the V3 Reward Manager contract in sUSD.

This aggregator fee share will help create competition for users at the front-end level, thereby contributing to more transaction volume and theoretical revenue, Eventually making it flow back into the protocol. As mentioned previously, in addition to the SNX buying pressure caused by buybacks and burns, Infinex will use their aggregator shares to buy back SNX and stake it, adding to this buying pressure and additional liquidity.

4. Risk

Although Synthetix has a lot to be excited about in 2024 thing, but it is important to understand some of the potential risks associated with its design and implementation. One of the main risks comes from using the native token as the main mortgage token. If the price falls rapidly, this could have a reflexive impact of lower prices, as a lower SNX price could cause cascading liquidations, resulting in less liquidity in the market. However, the current minimum collateralization ratio of 500% is very conservative and should help alleviate these concerns, and the use of alternative assets like USDC to provide liquidity is also underway.

The second major risk comes from assets listed through Synthetix perpetual contract products. First, if an asset is too illiquid or presents a risk of price manipulation, this could lead to malicious actors taking advantage of SNX liquidity. Especially on December 31, 2023, a huge market manipulation incident occurred in TRB. In less than 36 hours, the price of the Token increased by 200%, and then fell by 80%. This incident cost SNX holders a total of $3 million, which is approximately 10% of the fees generated in 2024. This type of risk is typically managed by the Spartan Council deciding not to list assets that are too risky, or by CCs setting tight OI parameters if riskier assets are listed. SIP-2048 is also a temporary measure, giving some CCs the ability to close markets in an emergency, but there is also discussion on whether a risk committee should be established to provide guidance on listing assets.

Other non-technical risks include reliance on EVMequivalence in order to deploy V3 , but in a world where othervirtual machinesbegin to become the norm, these virtual machines may haveparallelprocessing or more Safe programming language. However, Solidity and EVM have a big lead in terms of development tools, talent pool, and field testing on more projects over the years. Additionally, perpetual contract decentralized exchanges (DEXs) using central limit order books (CLOBs) have become popular, with platforms like Aevo and Hyperliquid gaining market share. While they are certainly becoming more popular, most of the newer platforms benefit from airdrop hunters and money laundering trades, so we have yet to see whether traders actually prefer CLOBs to oracle-based perpetual contract trading, or This is just a hot spot for speculators trying to get in on the next big airdrop.

5. Final Thoughts

Synthetix hopes to capitalize on the success of 2023 and capitalize on the new chain to test Synthetix V3 and Perps V3 products, new collateral types, and user behavior. More deployments on different chains will help field-test new products, highlight the types of collateral that bring the most liquidity, and showcase which communities and deployments attract the most users and capital. Theperpetual contract product itself will also see huge improvements in user experience, both for the Perps V3 product and for front-ends focused on recreating the CEX experience on-chain, such as Infinex. With the rise of order book DEXs in recent years, Synthetix has certainly proven that oracle-based perpetual contract DEXs still have an important place, and we will see whether these deployments redirect attention and liquidity to their direction.

Wilfred

Wilfred